You’ve gotten pre-approved for a mortgage, hired a top-notch real estate agent, and are ready to buy your first home. But how do you know what to look for when buying a house? There are many factors to consider before you make an offer.

However, buying a home has an inherent emotional side that is hard to ignore. When viewing homes, it’s easy to overlook red flags when imagining family dinners in the large dining room and how you’ll spend summer days in the backyard.

Therefore, deciding to buy a home involves considering the pros and cons and seeking advice from real estate professionals before you commit to homeownership.

From price and location to red flags, here are things to consider before buying a house.

Key Takeaways

- Home price and location are two significant factors to consider when looking for a property

- You should consider what amenities are important to you, and which ones you are willing to compromise on before viewing homes

- Red flags don’t have to be deal-breakers, but be sure to consider them before you jump into homeownership

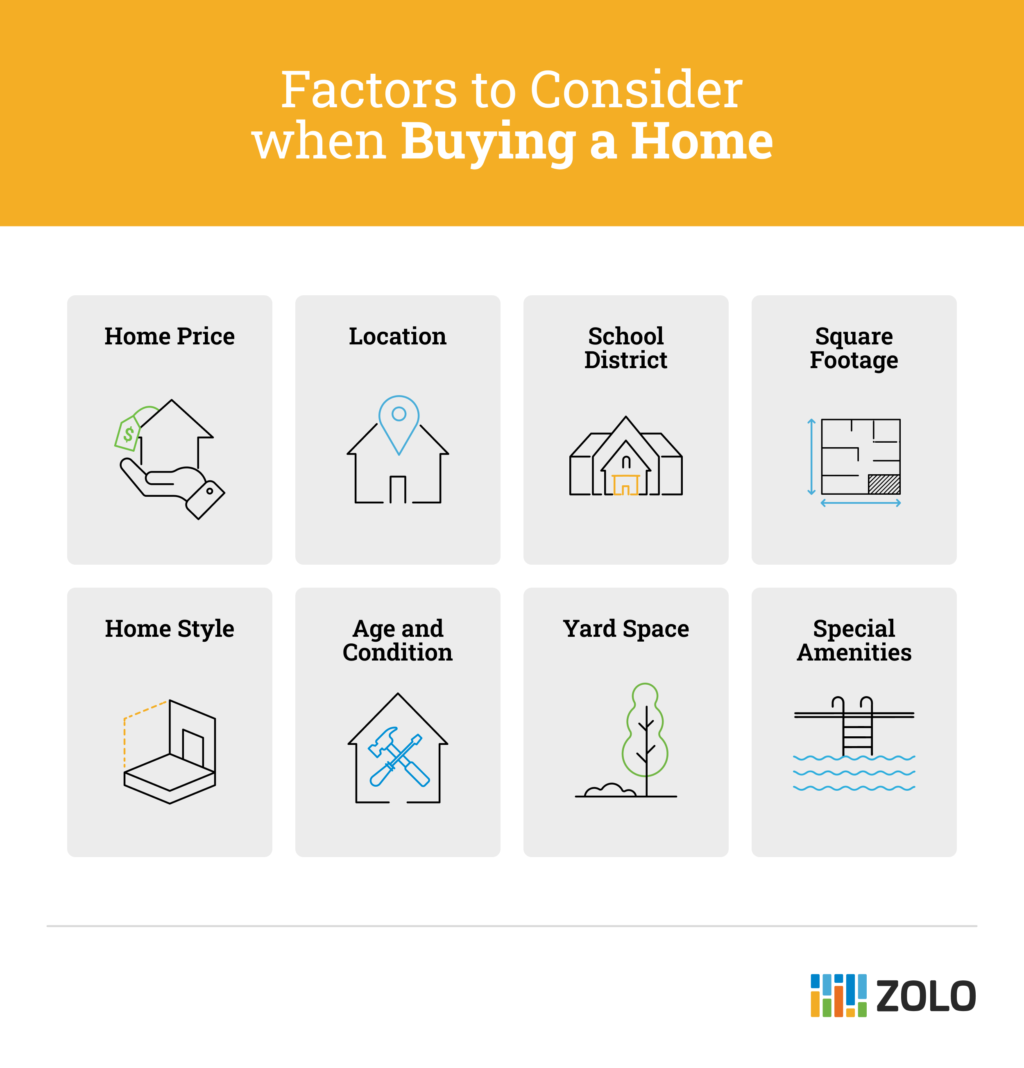

Factors to Consider when Buying a Home

As a first-time homebuyer, it can be easy to get swept up in the excitement of buying a home. But before you head to an open house, consider your must-haves list. Remember that you may not find a home that checks all the boxes, so you may have to compromise.

Home Price

Unsurprisingly, price is a crucial factor to consider when buying a home. Deciding how much you can afford can be challenging because you must consider several factors, including your income, any debt repayments, and how much you have saved for a down payment and closing costs.

Lenders use two formulas: your gross debt service ratio (GDS) and your total debt service ratio (TDS), to calculate how much mortgage you qualify for. The GDS takes your monthly housing costs as a percentage of your gross monthly income, which cannot exceed 39%. The TDS takes your monthly housing costs and minimum debt payments as a percentage of your gross income, which cannot exceed 44% of your gross monthly income.

Buying a home at the top of your budget may be tempting. However, consider how your monthly mortgage payment fits your budget alongside other expenses like home insurance, car payments, groceries, and other variable costs.

Location

There’s a reason why the saying “location, location, location” is popular. The neighbourhood you buy a home in can make a big difference in home price and expenses like property tax and land transfer tax. Additionally, you may want to consider the proximity to grocery stores and other shopping, crime rates, whether public transportation is available, and even the amount of street noise you will hear.

School District

If you have children, or plan to in the future, consider the local school district before you choose a home. Additionally, if you plan to resell the property in the future, the school district may affect the home’s resale value. A knowledgeable real estate agent can guide you through the homebuying process and help you find a home in a neighbourhood that meets your needs.

Square Footage

Another consideration when buying a home is the size of the house and property. Consider how many bedrooms and bathrooms are essential for you. On the other hand, it’s important to remember that more space often means more maintenance and cleaning.

Additionally, you’ll want to think about your future needs. For instance, are you planning to have children? Or are you close to retirement and looking for a smaller home on one level?

Home Style

It can be easy to get caught up in the colour of the kitchen cabinets or the type of flooring. But it’s important to look beyond the cosmetic when buying a house. Do you like the layout of the house? Does it have enough storage?

Look beyond the home’s staging and consider whether the structure and layout meet your specific needs.

Age and Condition

The age and condition of a home and its systems can affect its price and the amount of work needed to maintain it. For instance, a new condo will need much less maintenance than an older detached house.

Be sure to ask about the age of the roof, water heater, and HVAC systems. Moreover, you should assess the home’s condition, kitchen appliances, decks, and window frames, among other things, before deciding how much to offer on a house.

Yard Space

Another question is how much (or little) yard space is important to you. For some, a fenced yard is essential, but outdoor space is not as important for others. A large yard can be a lot to look after. Therefore, you should consider your lifestyle before you buy a house.

Special Amenities

Lastly, you should consider what special amenities are important to you. Are you looking for a house with a pool? Or, maybe a garage is essential to you. Some amenities, like pools or a home gym, can be added later through renovations or additions, while others, like an elevator, may be expensive or difficult to add.

Red Flags to Look for When Buying a House

While viewing homes, it’s essential to look for red flags. However, even homes that look good on the surface could have invisible issues, so hiring a professional home inspector to assess the home’s condition is important. Red flags do not have to be a deal breaker, but once found, you can make a plan to move forward with the purchase or decide to walk away if the issues are significant or out of your budget to fix.

Here are some common issues that a home inspection can find:

Foundation Issues

Foundation issues can be caused by soil movement, drainage problems, or improper construction. They can lead to structural issues, cracked walls, warped floors, misaligned doors, and other problems. Repairing foundation issues can be costly, so the sooner they are found, the better.

Water Damage

You should always look for water damage when buying a house. Water damage can be relatively minor or cause major problems. Your home inspector will look for signs of leaks, flooding, and poor drainage.

Mould

Mould can result from poor ventilation, water leaks, humidity issues, or flooding. Large areas of mould require professional attention, and the cost to remediate them will depend on the amount of mould and the cause.

Remodeling Efforts

One of the questions to ask when buying a home is whether or not any renovations have been completed. You’ll want to know what was renovated, by whom, and when. If a qualified professional did not do the work, mistakes may be expensive to fix.

Overall Neglect

Often, it is easy to see whether a property has been neglected. Buying a foreclosed property has many pros and cons, including the potential for return on investment, but you may incur unexpected expenses as well. Your home inspector and real estate agent can help you determine whether or not a home is worth the investment.

Signs of Pests

Lastly, signs of a pest infestation are another red flag to look out for when viewing homes. Pests like mice and termites can damage wiring and home structures.

Final Thoughts

Now that you know what to look for when buying a house, you can confidently begin the process. Remember to consider your budget, the local amenities, and potential red flags before you make an offer.

Homebuying FAQs

How do you determine how much you can afford?

One of the best ways to determine how much you can afford is to get pre-approved for a mortgage. A pre-approval will take into account the amount you have saved for a down payment, your income, property taxes, heating costs, and debt repayments.

What interest rate is a good rate?

Various factors determine mortgage interest rates, including your financial situation and broad economic factors. Therefore, a good interest rate depends on your personal circumstances. Review the current interest rates and consult with a mortgage broker or other mortgage professional to determine what you qualify for.

How do you know when it is a good time to buy a house?

The best time to buy a home is when you are financially stable, ready to stay in one location, and prepared to take on the maintenance requirements. Zolo real estate broker Lisa Nash advises, “Remember, timing the market perfectly is nearly impossible. The best time to buy is when you find a home you love and that fits your long-term needs.”

What are settlement costs?

Settlement costs are more commonly known as closing costs. These closing costs are paid upfront on the closing date and cover legal fees, registration fees, land transfer taxes, appraisal fees, surveys, home inspection, title insurance, and more. The full cost depends on the purchase price, where you live, and the type of property you buy, but a good rule of thumb is to budget 2% to 4% of the purchase price.