Homebuying in movies is usually portrayed in the following scenario: young homebuyers find a home they love, contact a real estate agent, and make an offer. The offer is miraculously accepted without negotiation, and they begin their life as new homeowners.

The reality of home buying in Canada is far from this picture-perfect story. One of the most significant deviations is the order in which the average Canadian will approach the homebuying process.

Instead of finding a home you love, contacting a real estate agent, and making an offer, the first step you should take in your home search is to get a mortgage pre-approval. At first glance, getting pre-approved for a mortgage might seem like a step you would take further in the process, but in reality, mortgage pre-approval can give you valuable information and help you make informed decisions in your home hunt.

What is Mortgage Pre-approval?

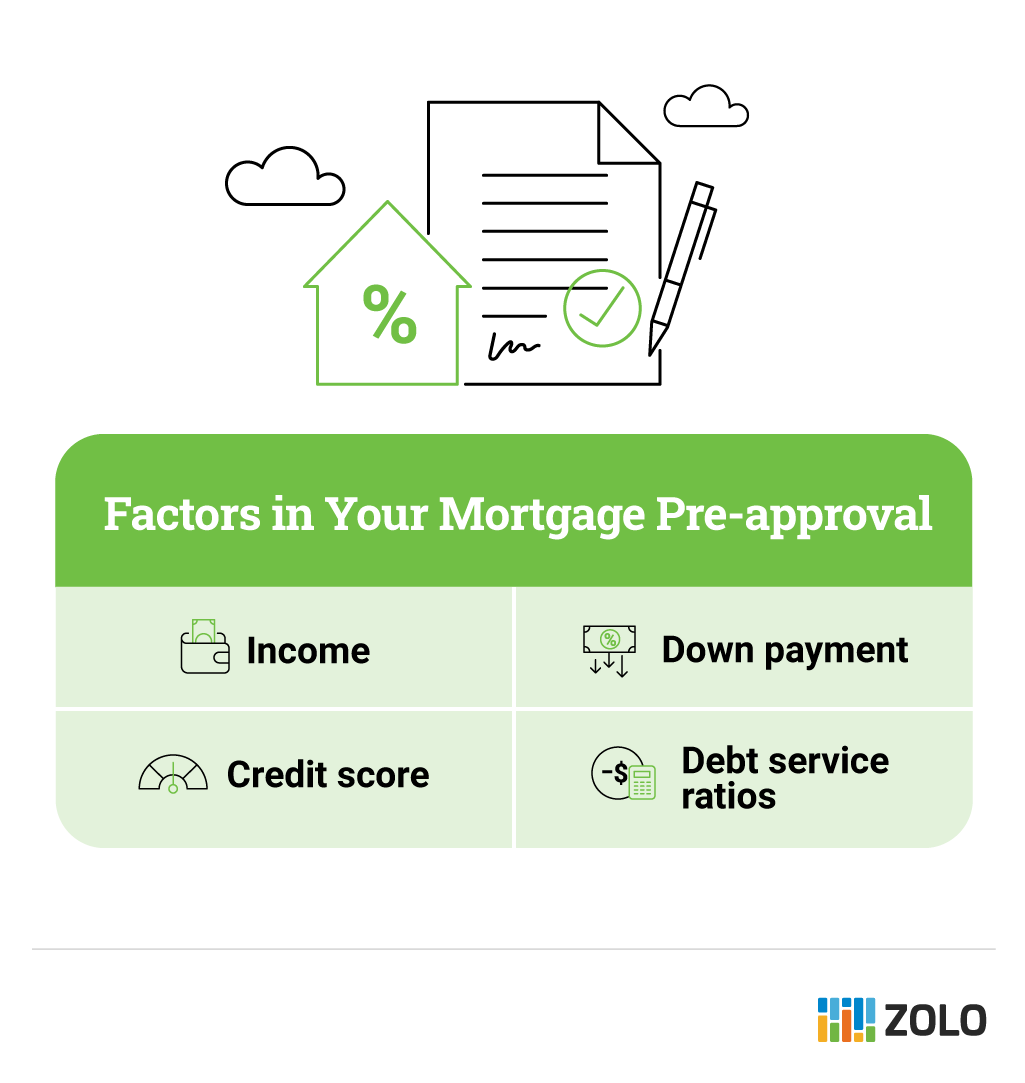

Mortgage pre-approval is the process of sitting down with a lender or mortgage broker to determine how much mortgage you can afford. With some basic information, they can determine how large a mortgage you can afford to borrow, the interest rate they can offer you, and your monthly mortgage payment.

However, pre-approval does not guarantee you’ll qualify for a mortgage with that lender. You’ll be guaranteed full mortgage approval once you submit your mortgage application, which happens after you have an accepted offer to purchase. Until you have final approval, consider your mortgage pre-approval only helpful information.

Mortgage Pre-Approval vs Pre-Qualification

While pre-approval and pre-qualification sound similar, they serve different purposes. Pre-qualification estimates how much you can afford based on general financial information. Mortgage pre-qualification does not require a credit check or documentation.

How to Get Pre-approved For a Mortgage

Mortgage pre-approval provides the key benefit of understanding how much you can afford (also called your maximum affordability) and your monthly payments. You can use this information to make a strategy for your house hunt. But, before you head to any open houses, follow these steps to obtain mortgage pre-approval.

Step 1: Contact a Lender or Mortgage Broker

Generally, you can obtain a mortgage directly from a lender like a bank or credit union or through a mortgage broker. Each choice has pros and cons.

If you work with a bank and prefer to keep all your business in-house, applying directly with your lender is quick and easy. The downside of applying for mortgage pre-approval through a bank or credit union is that you will only receive that lender’s best rate, not the best rate on the market.

Another source of mortgage pre-approval is a mortgage broker. Mortgage brokers are not affiliated with banks or credit unions; their role is to find you the lowest possible interest rate on the market. When you use a mortgage broker, you’ll complete a similar application, and your mortgage broker will shop your application around to several different lenders to find you the best possible interest rate. There is no fee to use a mortgage broker. Instead, they are paid by the lender.

Step 2: Provide Documentation

Whether you choose a bank or mortgage broker for your pre-approval, you’ll need to provide basic information to your lender or mortgage broker. This will help them understand your financial situation and accurately calculate how much you can afford.

Most of the information revolves around proving your income and documenting your down payment and debt. Here’s what each applicant will need to provide:

- Two recent paystubs

- A letter of employment

- Two years of T4s

- Proof of down payment, including 90 days of bank statements for the accounts where the down payment is held

- If the downpayment is a gift, proof certifying so

- For self-employed individuals, provide two years of complete tax returns and two years of Notices of Assessments

- A complete accounting of your debts and financial obligations, including child or spousal support

Your lender or mortgage broker may also ask your permission to pull your credit score.

Does Mortgage Pre-Approval Hurt Your Credit Score?

Some lenders will request to check your credit report to help them evaluate your pre-approval application. Whether or not this check will hurt your credit score depends on if the check is a “soft check” or a “hard check.” A soft check is also known as a soft pull and doesn’t hurt your credit score. These checks are typically used for background checks or when you check your credit score yourself.

On the other hand, a hard credit check is what mortgage lenders do when qualifying you for a loan. Because a hard check is related to new debt acquisition, it will lower your credit score by a few points. Whether or not your lender will do a hard check or a soft check depends on their internal policies. For example, TD Bank states on its website that its mortgage pre-approval process will not impact your credit score.

If you aren’t sure whether your lender or mortgage broker will perform a soft or hard credit check – ask!

Step 3: Lender Review

Once you’ve submitted your application, your lender or mortgage broker will secure your pre-approval. This process can take as little as a couple of hours or as long as a few days.

Step 4: Obtain Your Mortgage Pre-approval Letter

Once you’ve been pre-approved, you’ll receive a letter outlining the details of your pre-approval. Here is the information your pre-approval letter will include:

- The name of the lender

- Your mortgage amount

- Your down payment amount

- The mortgage interest rate

- Your monthly payment

- Your total purchase price

The letter will usually be on the lender’s official letterhead. It can sometimes be used when making an offer on a property to assure the seller that you are highly likely to receive full financing approval.

Questions to Ask About Your Mortgage Pre-Approval

It’s essential to be well-informed before accepting your pre-approval offer or choosing to keep shopping. To learn more, ask these questions:

- How long does mortgage pre-approval last? Hold periods vary from lender to lender but average between 30 and 160 days.

- What happens if rates drop? Most lenders will let you negotiate your pre-approval at the newer, lower rate.

- Can my pre-approval be extended? Your lender or mortgage broker may extend your rate hold if you haven’t found your dream home within the hold period.

What Not to Do Between Pre-approval and Full Qualification

Once you receive your mortgage pre-approval, you can begin your house hunt with a clear idea of how much you can afford. That said, mortgage pre-approval is not a full mortgage qualification. Having a mortgage pre-approval does not guarantee that you will be approved for financing on a home. If your financial profile changes, you may not qualify. Here are financial moves that could derail your mortgage pre-approval and full qualification.

- Change jobs

- Take on new debt

- Lower your credit score

How to Increase Your Mortgage Pre-Approval Amount

You may apply for mortgage pre-approval and find that you aren’t approved for the amount you’d hoped. In this case, you may wish to put your house-hunting plans on hold while you improve your financial situation. Here are four ways to improve your finances and increase your mortgage affordability.

Improve Your Credit Score

You need a credit score of at least 650 to 680 to qualify for a mortgage, but the higher your score, the better your mortgage rate. Three strategies will quickly improve your credit score. First, make your monthly payments diligently. Second, ensure that you carry less than 30% of your limit on revolving credit tools like lines of credit and credit cards. Finally, keep a mix of credit tools, like credit cards, lines of credit, utility bills, and a car loan.

Increase Your Income

To explain how increasing your income will improve your mortgage affordability, we’ll need to explain how lenders determine your affordability. Lenders use two ratios to determine how much mortgage you can afford. The first is your gross debt service ratio (GDS). This ratio measures the percentage of your income needed to pay your monthly housing costs, including principal, interest, taxes, and heat. The maximum ratio is 32%. Increasing your income will shift that ratio and improve your affordability.

Decrease Debt

A second ratio used to determine affordability is your total debt service ratio (TDS). This ratio uses the same numbers above but adds additional debt obligations like credit card interest, car payments, and other loan expenses. Your TDS ratio cannot exceed 40%. Paying off debt will reduce your ratio, and improve your affordability.

Increase Your Down Payment

You must have a down payment equaling at least 5% of the purchase price in Canada. In some cases, your mortgage affordability might be limited by the size of your down payment. In this case, taking time to save a larger down payment will help you qualify for a larger mortgage.

Do You Really Need Mortgage Pre-Approval?

Mortgage pre-approval provides valuable information about how much you can afford and whether you need to spend more time preparing for your home purchase. Mortgage pre-approval is a straightforward way to get a clear picture of your maximum home purchase price and lets you make informed decisions during house-hunting.

There are very few downsides to mortgage pre-approval, and we think it’s an essential part of the homebuying process.

Mortgage Pre-approval FAQ

How long does the mortgage pre-approval process take?

Getting pre-approved for a mortgage can take as little as a few hours or up to a few weeks, depending on your application and the lender. Straightforward applications typically take less time to process, while complicated applications can take longer to verify.

What happens after a pre-approval

After pre-approval, you will receive a letter stating the lender’s name, your mortgage pre-approval amount, the amount of your down payment, your mortgage interest rate, and your monthly payment.

After you make an offer on a home, your lender or mortgage broker will use the documentation provided to secure your final mortgage funding.

Is pre-approval the final approval?

No, pre-approval is an optional step to determine how much mortgage loan you can afford before you start home shopping. Pre-approval does not guarantee you will be approved for a mortgage. Instead, it provides information to make a strategy for your house hunt.

Once you make an offer on a home, your lender will submit your application to obtain mortgage funding.

How long does mortgage pre-approval last?

Most mortgage pre-approvals lock in your interest rate for between 60 and 130 days. During that time, you’ll have guaranteed access to the interest rate your lender or mortgage broker quoted. That means you still have access to the lower rate if interest rates rise during that time. Conversely, if interest rates drop, you can renegotiate.