Many potential homebuyers in Canada have likely been waiting to see if real estate prices will drop any time soon. As crucial as home prices are, we must emphasize another aspect of the home-buying process. When trying to purchase your first place, you must ensure that your credit score is at least good because you don’t want to be disappointed when you realize that you don’t qualify for a loan or the loan amount you had hoped for after finding the perfect home.

Your credit score will determine if you qualify for a mortgage on that dream home, so you must know where you stand before you start putting in offers. A question you’ve likely pondered if you’re still reading this is, “Can I get a mortgage with a bad credit score?” We will look at credit scores and how you can get a mortgage if it isn’t an ideal number.

What is a “Bad” Credit Score?

Before examining how to apply for a mortgage loan with poor credit, we should look at what lenders consider a “bad” credit score. According to Equifax, one of the two credit bureaus in Canada, lenders will view a credit score below 660 as risky, and these people will need help to qualify for decent loan terms. Your score is usually between 300 and 900. Scores from 660 to 724 are good, 725 to 759 are very good, and anything over 760 is considered excellent.

The reality is that a credit score below 680 will make it challenging to obtain a mortgage. Generally speaking, most banks in Canada will require you to have a score of at least 600 to qualify for a mortgage in the first place. If your credit score is below 560, it’s considered “poor,” and you’ll have challenges qualifying for any credit.

How Does This Impact Your Mortgage Application?

You may wonder about the significance of a bad credit score on your mortgage application. When the lender analyzes your financial information, they will pull your credit report and review your credit score to see your history of handling money. A bad credit score will indicate that you need a more robust record of making timely payments. A bad score will show the lender that you’re risky to loan money compared to someone with a good credit score. If your credit score needs to improve, you may get a higher mortgage rate or not qualify for a mortgage loan.

A credit score below 600 would disqualify you from CMHC insurance. When you have an insured mortgage, you can make a lower down payment on the home of as low as 5%. With an uninsured mortgage, you must make a down payment of at least 20%.

A mortgage loan is for a significant amount of money, so the lender wants to ensure that you have built up a history of making payments on time and that you can be deemed trustworthy with money. That lousy credit score caused by late payments and opening up too much credit could hold you back from getting approved by a traditional bank for a home mortgage.

What Are Your Options if You Have a Bad Credit Score?

What if you have a bad score and still want to apply for a mortgage? Here are your best options if you’re looking for how to get a mortgage with a bad credit score.

B Lenders

Lenders that aren’t traditional banks (like credit unions) are considered “B lenders” and are more flexible with mortgage requirements. Unlike private lenders, these B lenders will typically follow the federal regulations for federally regulated banks. These B lenders all have different requirements, so you must shop around. For example, some offer CMHC-insured mortgages requiring a minimum credit score of 600.

Private Lenders

Numerous private lenders in Canada will offer mortgages to those with bad credit or even no credit. However, you may have to work with a mortgage broker to access these lenders. The positive news is that some private lenders won’t have a minimum credit score requirement to qualify if you desperately want to enter the real estate market. It’s worth mentioning that if you get a bad credit mortgage through a private lender, you’ll have to spend money on lender fees and get a much higher interest rate.

Hopefully, we answered the question from the beginning of this article, “Can I get a mortgage with a bad credit score?” The good news is that you still have options for landing a mortgage if you need a better credit score. The bad news is that you’ll have to spend more money on interest, and you’ll need to save up more for your down payment. You can always take the time to improve your credit as you’re not stuck with one score.

What If I Have No Credit Score?

If you have no credit score, it’s likely because you need to have a credit history. You’ll want to focus on building up some credit history to build your credit score up to a respectable number. You may have to start with a credit card that has a low limit, where you pay your bills on time to prove that lenders can trust you as a borrower.

On the bright side, having no credit score means that you at least have a clean sheet, and you can prioritize building up credit for the next few years as you also work on saving up enough for a down payment.

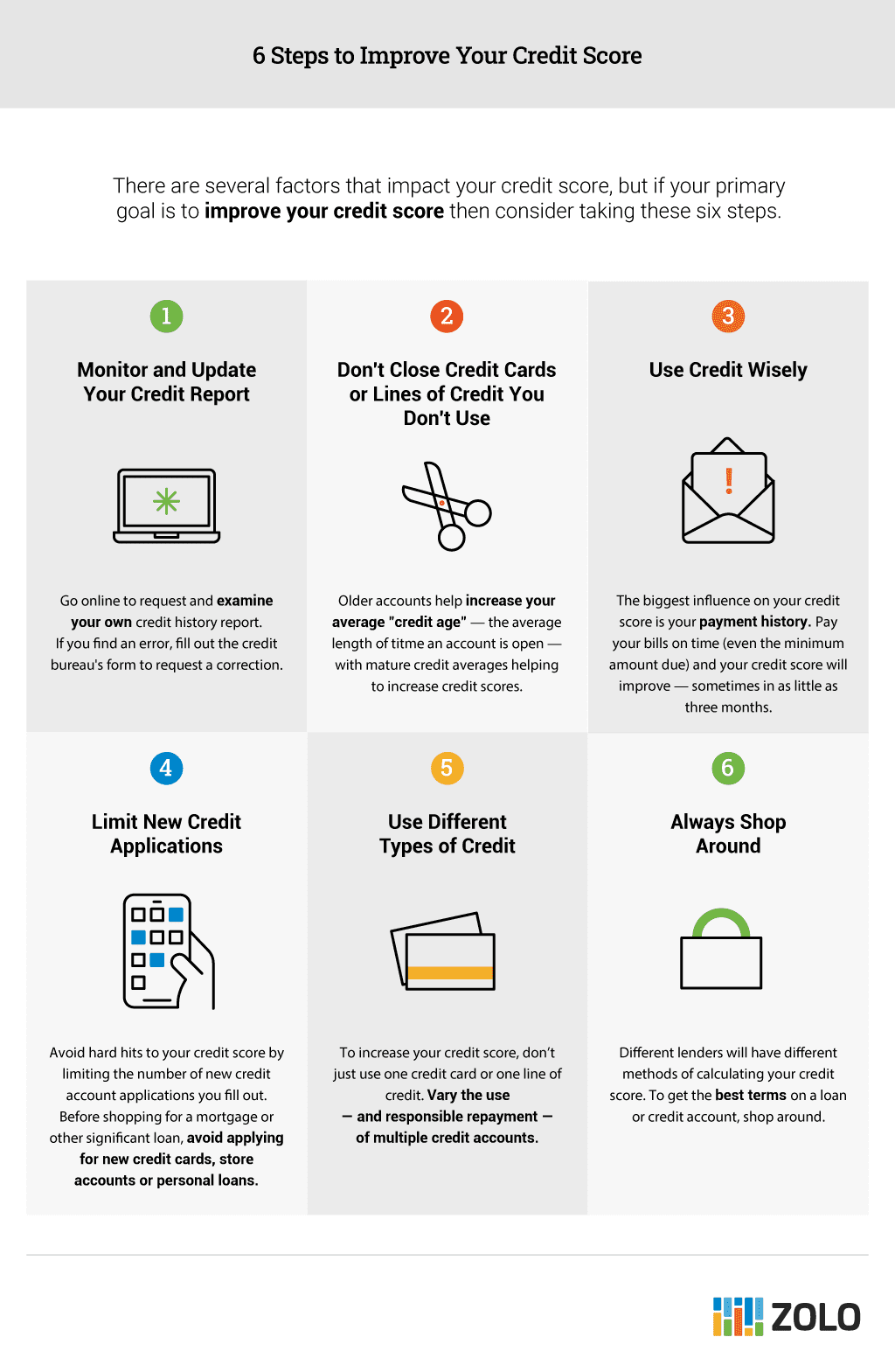

How Can I Improve My Score?

If you currently don’t have an ideal credit score, then you can always work on improving it. Here are the best ways to improve your credit score:

- Always make your payments on time. If you have any late or missed payments on a credit card, cell phone bill, or any other account, lenders will report this to credit bureaus.

- Monitor your payment history. You must make your minimum payment on the credit card, contact lenders if you’ll be late, and even pay the bill when you dispute a discrepancy.

- Keep your credit card balance below the limit. It will help if you only use a little of your available credit. Generally, it would help if you aimed to use less than 30% of your available credit.

- Don’t apply for credit often. Applying for new credit accounts frequently can hurt your credit.

- Review your credit report. You want to ensure that all of the information is accurate. If you notice any discrepancies, then you can file a dispute online.

According to Transunion, the other leading credit bureau in Canada, it’s important to remember that the bureaus are messengers and that it’s up to us to let them know when a creditor has submitted inaccurate information.

If your credit score isn’t where you want it to be, the good news is that you can still get a mortgage if you have your heart set on getting into the real estate market since you get a bad credit loan. Remember the high-interest rates and lender fees associated with bad credit mortgages from B lenders and private mortgage companies.