Saving for a down payment can take years, and for many, saving 20% can feel like an unachievable goal. Thankfully, mortgage loan insurance can help you purchase a home with as little as 5% down. While utilizing mortgage loan insurance can increase your overall homeownership costs, it also has many benefits. In particular, owning a home years sooner.

Mortgage loan insurance has many names, including CMHC insurance and mortgage default insurance. It may also be referred to as mortgage insurance. This product was designed to encourage home buying and protect lenders from buyers at high risk of defaulting.

Here’s everything you need to know about CMHC insurance before you purchase a home.

Key Takeaways

- CMHC insurance, also known as mortgage default insurance, is mandatory for home buyers with a down payment of less than 20%

- Mortgage default insurance protects the lender if you stop making mortgage payments

- Mortgage loan insurance is not available on homes priced over $1.5 million

What Is CMHC Mortgage Insurance?

Mortgage loan insurance, sometimes called CMHC insurance, is required if you purchase a home with a down payment of less than 20% of the home’s purchase price. A mortgage with CMHC insurance is known as an insured mortgage.

This insurance is designed to protect lenders if homeowners stop paying their mortgages.

Do You Have to Get Mortgage Default Insurance?

Mortgage loan insurance is mandatory in Canada if you purchase a home with a down payment of less than 20% of the home’s purchase price.

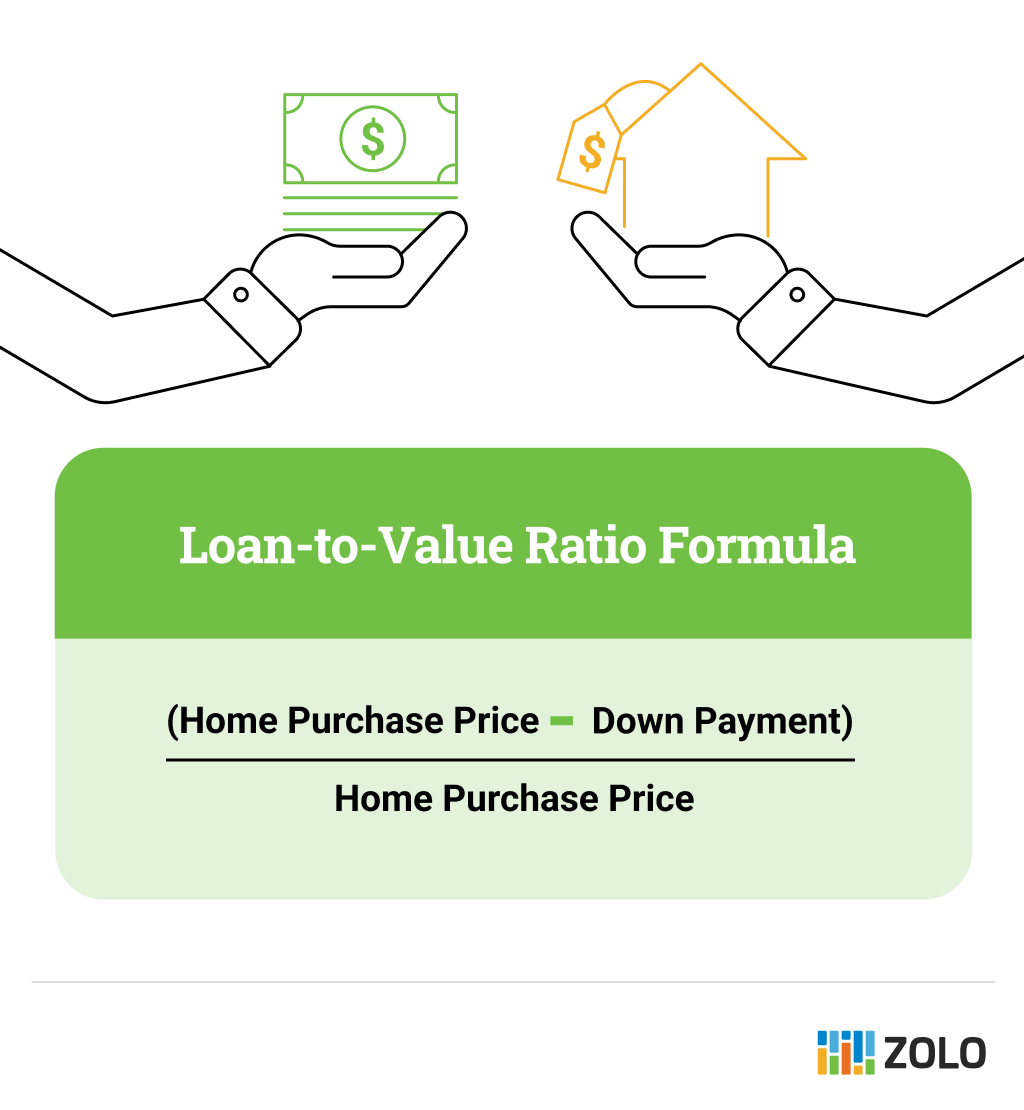

The need for mortgage default insurance depends on your loan-to-value ratio (LTV). The LTV is calculated by comparing the amount you are borrowing to the total purchase price. For example, if you make a 5% down payment on a home, your LTV ratio is 95%.

Any mortgage with an LTV of more than 80% is considered a high-ratio mortgage, and mortgage insurance is required.

Mortgage insurance is not available on homes priced over $1.5 million since these homes require a minimum down payment of 20%.

Cost of Mortgage Insurance

If you plan to purchase a home with a down payment of less than 20%, you’ll need to factor mortgage default insurance into your budget.

There are three costs to take into consideration:

- Premium – The mortgage insurance premium is calculated depending on your loan-to-value ratio (LTV). The higher the LTV, the higher the premium

- Interest – If you aren’t able to pay your default insurance premium upfront, it will be added to your mortgage, which will result in extra interest charges

- Provincial Sales tax – In Manitoba, Quebec, Ontario, and Saskatchewan, provincial sales tax is added to the mortgage insurance premium, which is paid as a lump sum along with other closing costs

As of October 2024, the standard purchase premiums are as follows:

For mortgages with a down payment between 20% and 35%, mortgage loan insurance is added. However, the lender typically pays for the insurance without passing the cost on to you.

Mortgage loan insurance can add thousands of dollars over the life of your mortgage. For example, if you buy a home for $500,000, the total mortgage amount varies depending on the size of your down payment and the mortgage default insurance premium.

Benefits of Mortgage Loan Insurance

While the downside of mortgage default insurance is that you will pay more for your mortgage, there are also several advantages.

Smaller Down Payment

For many, saving 20% for a down payment takes considerable time. By saving 5%, you may be able to own a home years sooner.

Lower Interest Rates

One of the most significant benefits of CMHC insurance is that mortgage lenders offer their best mortgage interest rates to those with insured mortgages.

Helps Stabilize the Housing Market

Insured mortgages support the housing market in Canada by protecting lenders against defaults and foreclosures.

Who Offers Mortgage Insurance in Canada?

There are three providers of mortgage default insurance in Canada:

- Canada Mortgage and Housing Corporation (CMHC)

- Sagen (formerly Genworth Canada)

- Canada Guaranty

The Canadian Mortgage and Housing Corporation is the most widely known, which is why many people refer to mortgage default insurance as “CMHC insurance.” The CMHC is a crown corporation that serves as Canada’s national housing agency.

Sagen and Canada Guaranty are private companies that also offer mortgage default insurance.

As a borrower, you may not notice a difference between providers, as their requirements and premium rates are essentially the same.

How to Qualify For Mortgage Insurance

While mortgage loan insurance may be mandatory, you will have to qualify for a high-ratio mortgage through the following:

- Good credit – For CMHC, the minimum credit score is 600, and for Sagen, the minimum score is 680. Canada Guaranty does not publish its minimum credit score but states that a strong credit profile is required

- Debt – Your Gross Debt Service ratio must be less than 39%, and your Total Debt Service ratio must be less than 44%

- Purchase price – The purchase price must be less than $1.5 million

- Amortization – The maximum amortization period is currently 25 years. However, it has increased to 30 years for first-time homebuyers and buyers of new builds.

In addition, the home must be in Canada and a primary residence. For multi-unit homes of up to four units, one unit must be owner-occupied. On the other hand, Sagen and Canada Guaranty offer mortgage loan insurance for certain types of second homes.

Mortgage Default Insurance vs Mortgage Protection Insurance

People often confuse mortgage default insurance with mortgage protection insurance. However, they are two different products with different purposes. In short, mortgage default insurance protects your lender if you default on your mortgage. Compared to mortgage protection insurance, which protects you if you are unable to make your mortgage payments.

Learn about the differences between mortgage default insurance and mortgage protection insurance below:

Final Thoughts

Many people see CMHC insurance as a punishment for not having a 20% down payment, but this is not the case. Mortgage loan insurance is a tool that many Canadians can use to own a home sooner and access the best mortgage interest rates.

CMHC Insurance FAQs

Do I have to get mortgage insurance?

Canadian mortgage lenders require default insurance for home purchases with less than a 20% down payment. There are a few ways to avoid mortgage default insurance:

- Make at least a 20% down payment

- Work with a private lender or credit union for your mortgage. These lenders are not federally regulated and may choose not to impose mortgage default insurance.

Can I cancel CMHC mortgage insurance?

In short, you can’t cancel CMHC insurance. However, if you sell your current home and buy another house, you can take advantage of the portability option. The portability option reduces or eliminates the premium amount owed on the newly insured mortgage.

When you’re renewing your mortgage, it may be possible to switch from an insured loan to an uninsured loan, provided you have at least 20% equity in your home. However, you may lose access to the best interest rates.

In addition, you may be eligible for a 25% refund if you make energy-efficient upgrades to your home through the CMHC Eco Plus program.