Mortgage terms only last a few years, and when the term is up, it’s time to renew. At this point, you need to decide if you want to stick with your current lender or look elsewhere. Like shopping for a mortgage, you want to compare pricing and negotiate to get the best rate when renewing your mortgage.

Key Takeaways

- Mortgage renewals should be negotiated to ensure you get the best rate. Don’t be afraid to shop around and compare other lenders’ offers.

- If you find a better deal elsewhere, you do not need to stick with your original lender. However, remember that switching lenders will likely incur extra costs, and you must pass the mortgage stress test.

- If you have a lot of equity in your home and want to access it, consider refinancing your home instead of renewing your mortgage.

What is Mortgage Renewal?

A mortgage renewal happens when your mortgage term is up. The end of your term isn’t the end of your mortgage, but it’s the end of the time period that you and your lender agreed on your mortgage conditions.

In Canada, the standard length of a mortgage loan is 25 years. Rather than sign a single contract and be locked into an interest rate for the entire period, you break the payment period down into smaller sections called terms. These terms can last just a few months or several years. At the end of each term, you need to renew your contract, often with a new interest rate, which will depend on the current economy and your financial standing at the time of renewal.

Since mortgages tend to be hundreds of thousands of dollars, the expectation is that it will take many years to pay off, so chances are you will have to renew your mortgage several times before it is paid in full.

How to Renew Your Mortgage?

When it comes time to renew your mortgage, you have two options: you can either renew with your current lender or find a new lender. Here are the basic steps to follow to renew your mortgage.

Step 1: Review Your Mortgage

If you are considering renewing with your current lender, are all your mortgage needs being met? If not, can you make the changes and adjustments you want? For example, you may wish to add additional payments or change your payment frequency.

Step 2: Compare Other Lenders

If you think you will stick with your current lender, look around and see what is available. Shop around a couple of months before the end of your term.

Step 3: Negotiate

If you received better offers when shopping around but prefer not to change lenders, take these offers to your current lender and see if they will match or beat it. Provided that you are happy with your current lender, then renew with them. If not, go elsewhere.

Note that if you do choose to go elsewhere, there will be additional costs when switching to a new lender. These costs include:

- Transfer and setup fees

- Appraisal fees

- Other admin fees

Ask your new lender if they will cover these costs if you switch. They might cover some or all of the fees if they want your business. In addition to the extra expenses, signing with a new lender means you will also need to requalify and undergo another stress test, which is important to keep in mind.

When Do You Renew Your Mortgage?

Mortgage renewals will take place at the end of each term. As discussed above, terms differ in length from a few months to several years, which means you will likely have to renew your mortgage several times before you can pay off the mortgage in full. You should expect to receive your mortgage renewal notice in the mail several months before your mortgage is set to renew. Your lender may call you up to six months before your renewal date to start the process.

What is a Mortgage Renewal Statement?

A mortgage statement is an official document provided to you by your lender at least 21 days before your term is up. The statement will include essential information like:

- Remaining principal at the renewal date

- Your new term’s interest rate

- Payment frequency

- Length of the proposed term

- Any charges or fees that apply

The statement will be sent by either email or traditional mail (depending on your method of choice).

Does your Mortgage Automatically Renew?

Whether your mortgage will renew automatically is dependent on your lender. Some mortgages may automatically renew, while others won’t. Be sure you understand your contract with your lender and what happens when it comes time to renew so you can be prepared either way. If you have a renewal statement, check it – usually, automatic renewal will be indicated on the statement.

Mortgage Renewal Interest Rates

Can you get the best interest rate when you renew? Possibly, but it’s essential to shop around and ensure the mortgage rate your lender offers at renewal is competitive with what is available from other lenders. If the rate they offer on your renewal statement is not competitive, it’s important to negotiate.

Even a few tenths of a percentage point can make a big difference in how much interest you’ll pay on your mortgage over time, so it’s essential to do your due diligence and ensure your mortgage has a competitive interest rate.

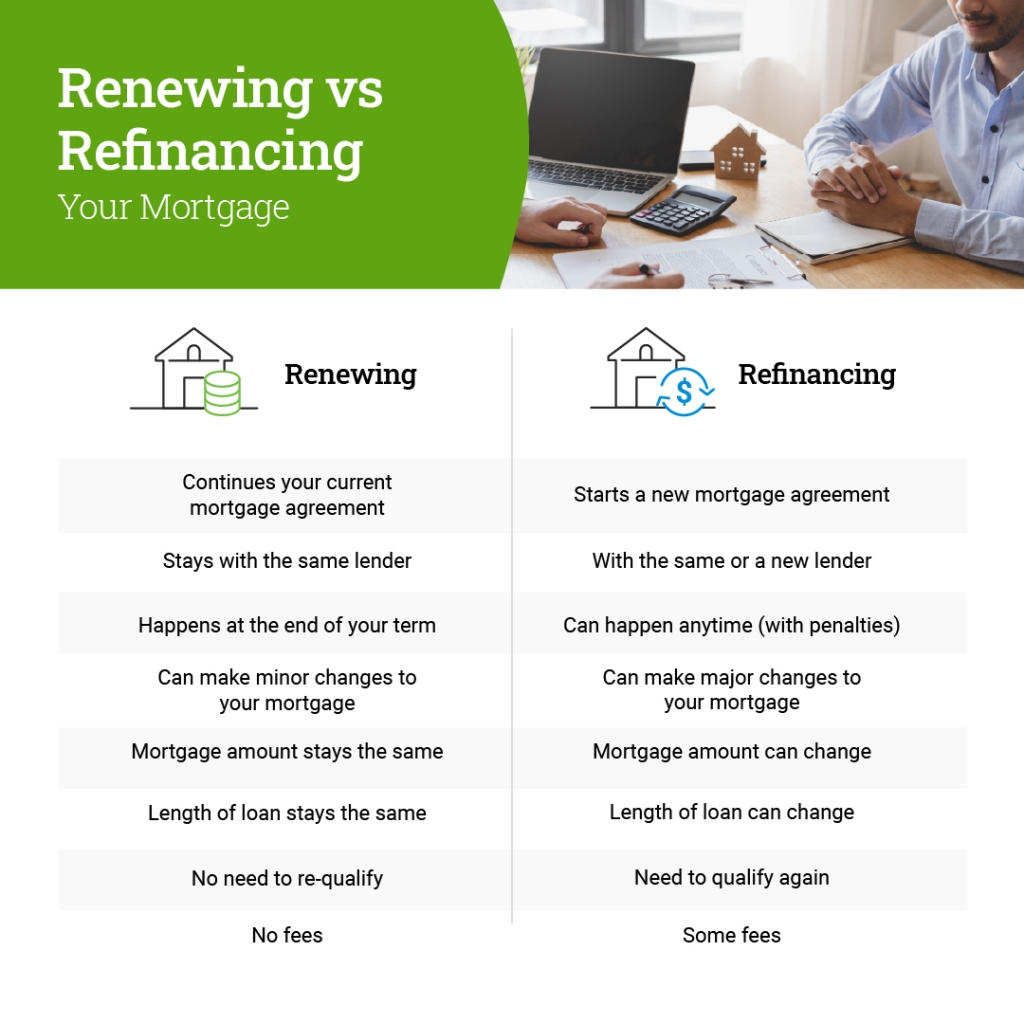

How is Mortgage Renewal Different from Refinancing?

Your mortgage is a loan that you take out to pay off your house. The more you pay into your mortgage, the more equity you have in your home. When you renew your mortgage, you are just updating the contract. You may be able to make a few minor changes to your payment frequency or term, and the interest rate will change, but the specifics of your mortgage, like the principal amount and the total length of the loan (known as the amortization), will stay the same.

You’ll need to refinance if you want to make more significant changes to your mortgage. When you refinance your home, you break the mortgage contract and sign onto a new one, so all of the terms, including the mortgage amount and length, can be renegotiated.

Refinancing allows you access to the equity you have in your home, which may come in handy if you want to do major renovations or purchase a new home. Another benefit of refinancing is that it allows you the opportunity to consolidate your debt, which can be helpful if you have any high-interest debt.

You can refinance your mortgage at any time. You don’t need to wait until the end of the term, but remember, if you refinance your mortgage at any time besides at renewal, you are breaking your current mortgage contract, and you’ll need to pay a penalty to do so.

It’s also important to note refinancing your mortgage requires an entirely new mortgage application, and you’ll need to re-do the entire approval process, which includes income assessment, debt analysis, and passing the mortgage stress test.

What Happens if Your Mortgage Renewal is Denied?

Sometimes, your financial situation will change after buying a home, and at renewal, your lender may decide your financial profile is too risky to continue your mortgage. If your current lender denies you renewal, you can try to discuss it with them. They may be willing to offer you a new mortgage under different terms.

If your lender is unwilling to reconsider, you must shop for a new mortgage with a different lender. A mortgage broker is an excellent place to start if you need to find a new lender. If “A” lenders such as big banks won’t take you on, you will have to consider a “B” or private lender to take you on. In the worst-case scenario, you will have to sell your home.

Renewing your mortgage will happen several times while paying off your loan, so it’s essential to understand the process and the opportunity it presents. You don’t have to stick with your mortgage provider, and shopping around to find the lowest rate is wise.

Mortgage Renewal FAQs

What is a mortgage renewal?

When you purchase a home and take out a mortgage with a mortgage lender, you sign a contract for what is referred to as a term. A term is usually between a few months to five years, although it can also be longer. If you haven’t paid back the total amount of the mortgage loan within the term, you will have to sign a contract for a new term. This contract is called a mortgage renewal, and you will likely have to renew your mortgage multiple times before you pay it in full.

Can a bank automatically renew your mortgage?

Some lenders may automatically renew your mortgage if you haven’t told them you want to change or negotiate. Others will not, and you will need to re-sign a contract. It depends on the lender, so make sure you know what to expect to be prepared when the time comes for mortgage renewal.

Is renewing your mortgage the same as refinancing?

No, the two are different. A mortgage renewal is essentially re-signing a contract with a new interest rate. There is some wiggle room to negotiate, but you continue with your existing agreement. If you refinance, you must break your mortgage contract and start fresh. Refinancing has many advantages, and it gives you more room to negotiate. However, you are starting over and must qualify for your mortgage and pass the stress test again. There will also likely be extra fees involved.

Can you be denied a mortgage renewal?

Yes, it is possible to be denied a mortgage renewal. In this case, your lender must tell you at least 21 days before renewing your mortgage that they are unwilling to continue with you for another term. If you are denied, you can try to negotiate with your new lender, or you will have to find a new lender.