After years of dealing with the high costs and inconveniences of renting, you’re craving more independence and looking to purchase your first home. But there’s a big hurdle to be crossed first—the dreaded upfront costs. Without down payment assistance, the minimum down payment amount is 5% for properties priced at $500,000 or less in Canada. Although 5% might not sound so bad, its dollar amount can be daunting, particularly for those who make only a modest income.

If you purchase a house that costs more than $500,000, you have to pay 5% for the first $500,000 plus 10% between $500,000 and $1.5 million

However, down payment assistance programs can help put homeownership within reach. Here are some of the programs currently available in Canada.

What Is Down Payment Assistance?

Down payment assistance programs can come in multiple forms, including grants, rebates, tax-free or interest-free loans. Additionally, other programs can help you save for a down payment through tax credits.

The majority of these programs are for first-time home buyers. However, if you are a person with a disability, you don’t have to be a first-time home buyer as long as you are buying the property to use as your primary residence.

Different Types of Down Payment Assistance

Fortunately, federal and provincial down payment assistance programs exist to support first-time homebuyers with limited income. You may not have heard about these programs or know how they work, but if you are serious about buying a house, it’s worth investigating and seeing what benefits they may hold.

If you are currently saving for a down payment, several options are available. For instance, specialized savings accounts and provincial down payment assistance programs that provide down payment loans. Moreover, after you’ve purchased a home, tax credits and rebates can help put money back into your pocket.

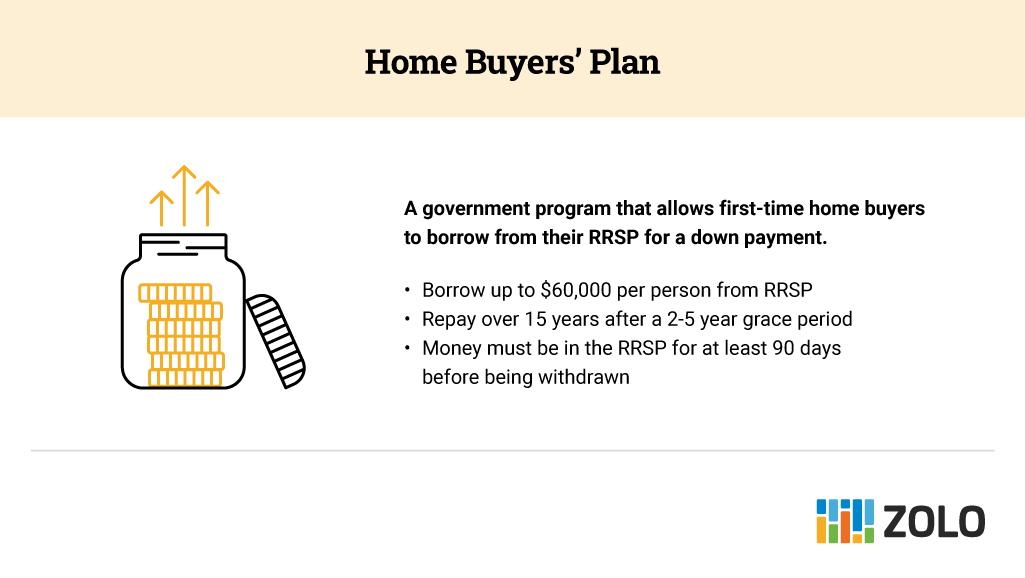

Home Buyers’ Plan

Under the Home Buyers’ Plan (HBP), you may borrow up to $60,000 tax-free from your RRSP (Registered Retirement Savings Plan) to fund your down payment. If you plan to purchase a home with a partner who is also a first-time purchaser, you can each borrow up to $60,000, or $120,000 combined, tax-free.

To qualify for this program, you must be a first-time homebuyer, defined as anyone who has not purchased a house or lived in a home their spouse owned in the last four years. (There are also different requirements for people with disabilities.)

The HBP funding is treated as a 15-year interest-free loan if you start making annual repayments to your RRSP account no more than two years after borrowing the money from your RRSP. Remember that the money in your RRSP must have been available for at least 90 days before the HBP application is submitted.

When repaying your HBP withdrawals, you do not have to repay the money into the same RRSP account — you can contribute to any RRSP account. Instead, the repayment happens when you designate a portion of your RRSP contribution as part of your HBP loan repayment on your taxes.

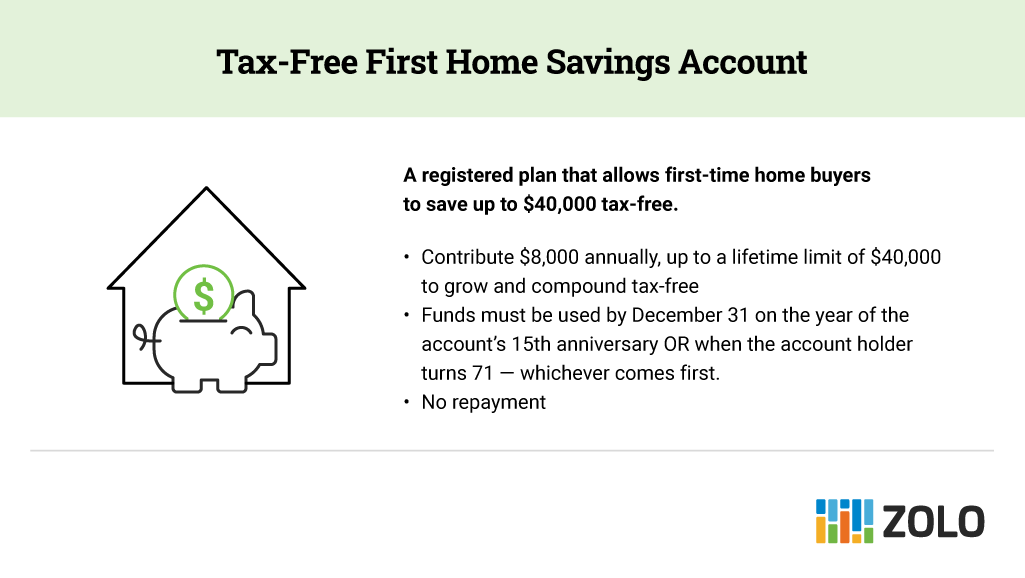

Tax-Free First Home Savings Account

The Tax-Free First Home Savings Account (FHSA), introduced in 2023, allows you to save up to $40,000 tax-free towards the cost of your first home. This account can hold the same investments currently allowed in your TFSA, including mutual funds, publicly traded securities, bonds, and Guaranteed Investment Certificates (GICs). In addition, similar to an RRSP, any contributions made to your FHSA are tax-deductible.

To be eligible to open a FHSA, you must be a resident of Canada, aged 71 or younger. You must also be a first-time home buyer, meaning you or your spouse or common-law partner don’t currently own a home and haven’t in the previous four calendar years.

You can contribute $8,000 annually, up to a lifetime limit of $40,000. However, if you cannot contribute the total $8,000 in one year, you can carry over the unused contribution room forward the following year.

Finally, you can make withdrawals in a lump sum or in a series within 30 days of moving into your new home.

Open your First Home Savings Account with Questrade online and start saving for your first home!

First-Time Home Buyers’ Tax Credit

The First-Time Home Buyers’ Tax Credit (HBTC), first introduced in the 2009 federal budget, allows first-time homebuyers to recover some of the costs related to their purchase. Specifically, this non-refundable tax credit covers inspections, legal fees, and other similar closing costs and is valued at up to $1,500.

Dwellings that qualify for the tax credit include new and existing single-family homes, condos, townhomes, semi-detached homes, and duplexes. However, the requirement to be a first-time buyer does not apply if you have a disability.

In addition, you must claim the credit in the tax year you purchased your home.

Land Transfer Tax Rebate

Homes purchased in Canada are subject to a land transfer tax ranging from 0.5% to 2.0% of the purchase price. Depending on where you are located, this can equal thousands of dollars. However, suppose you are a first-time homebuyer purchasing in British Columbia, Ontario, or Prince Edward Island. In that case, you may be eligible to receive a rebate on a portion of the land transfer tax.

In addition to the provincial rebate, first-time homebuyers in Toronto can receive a refund on the city’s land transfer tax. Other provinces and municipalities may also offer different rebate programs to help residents offset the cost of land transfer tax.

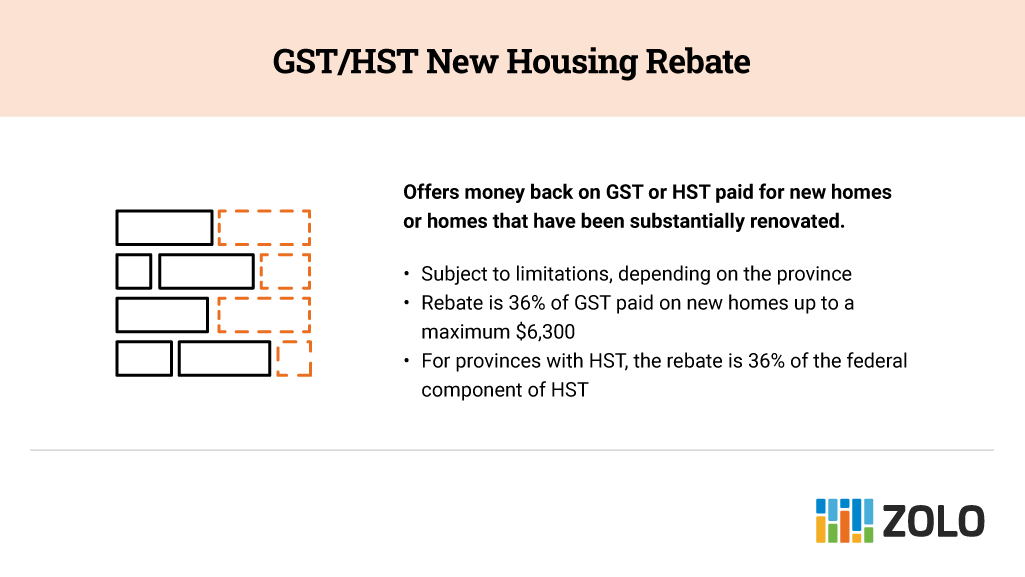

GST/HST New Housing Rebate

The GST/HST New Housing Rebate offers you money back on the portion of the GST (goods and services tax) or HST (harmonized sales tax) you must pay when you build a house or substantially renovate your existing house. You could also qualify for a refund on a portion of the GST or HST you pay when building an add-on to your current home or converting a commercial property into a residential home.

You can only claim this rebate if the house’s value is less than $450,000. This rebate is also available for non-traditional homes, such as mobile and floating homes.

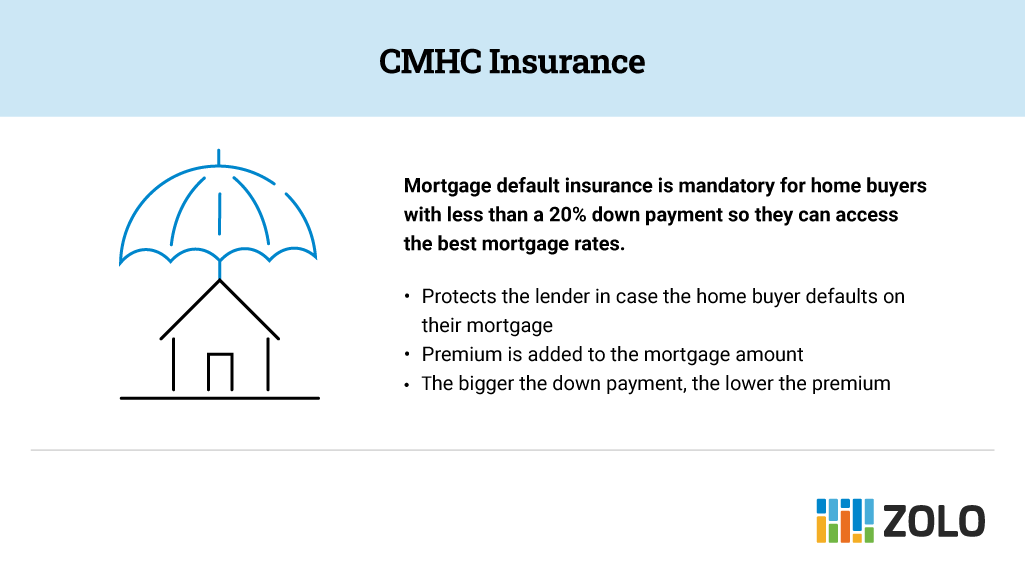

CMHC Insurance

Also known as mortgage default insurance, CMHC insurance is required for homebuyers purchasing a home with less than a 20% down payment. Despite the name, mortgage default insurance doesn’t protect you in the traditional sense. Instead, it protects the lender if you default on your mortgage payments. Specifically, this protection makes homebuyers with smaller down payments much less risky for lenders, making homeownership more achievable.

Lenders charge CMHC insurance as a premium added to your mortgage amount, which varies depending on the size of your down payment. CMHC insurance is unavailable on homes costing more than $1 million. A down payment of at least 20% is mandatory for homes in this price range.

This insurance is available through Canada Guaranty, Sagen, or the Canada Mortgage and Housing Corporation (CMHC).

These are just some down payment assistance programs available to Canadians. Furthermore, there are additional grants and programs available through provincial programs:

Jump to your region:

- British Columbia

- Alberta

- Manitoba

- Ontario

- Quebec

- New Brunswick

- Nova Scotia

- Prince Edward Island

- Newfoundland and Labrador

- Northwest Territories

- Nunavut

British Columbia Down Payment Assistance

Métis Financial Corporation First-Time Home Buyer Program (FTHBP): For Métis Citizens who have resided in British Columbia for at least one year, this program provides a forgivable loan of up to $20,000 for a down payment and an additional $3,000 towards closing costs.

Alberta Down Payment Assistance

Attainable Homes (AHC): This program is for Calgary residents only. Applicants contribute $2,000 towards the down payment of their home while the program covers the remainder.

First Place Program: This program allows Edmonton residents to defer land costs on select properties for up to five years.

Manitoba Down Payment Assistance

First-Time Home Purchase Program: For Metis citizens in Manitoba, this program provides a 5% down payment of up to $18,000 plus another 1.5% of the purchase price, up to $2,500 for closing costs.

Affordable Homes Program: Provides down payment assistance of up to 25% of the purchase price in select Manitoba communities.

Ontario Down Payment Assistance

Shared Equity Mortgage Through Ourboro: Provides 5% to 15% of the purchase price, up to a maximum of $250,000, in exchange for a percentage of equity in your property. In return, when you sell your home, you’ll pay back the percentage of equity that you share with Ourboro. Therefore, if your house increases in value, you will pay more than you first received.

Region of Waterloo Affordable Homeownership Program: Provides eligible home buyers who have lived in the Waterloo region for at least one year with a 5% loan for a down payment.

County of Simcoe Affordable Homeownership Program: Provides eligible home buyers who currently rent in Simcoe County with a 10% loan for a down payment.

B-Home Homeownership Program: Provides eligible first-time home buyers currently renting in Brantford or Brant County with a 5% loan at closing.

Lanark County Homeownership Program: Provides eligible first-time home buyers who are currently renting in Lanark County with down payment assistance up to 8% of the purchase price.

County of Renfrew Affordable Homeownership Program: Provides eligible first-time home buyers who are currently renting in Renfrew County with down payment assistance up to 10% of the purchase price.

Oxford County Home Ownership Program: Provides eligible home buyers who are currently renting in Oxford County with down payment assistance up to 5% of the purchase price.

Niagara Homeownership Program: Provides eligible first-time home buyers who have been renting in Niagara for at least six months with down payment assistance up to 5% of the purchase price.

District Municipality of Muskoka Gateway Homeownership Program: Provides eligible first-time home buyers in Muskoka with down payment assistance up to 10% of the purchase price.

Quebec Down Payment Assistance

AccèsCondos: A financial assistance tool to help residents buy an affordable condo in Montreal. In return for a deposit of $1,000, the SHDM (Montreal’s housing development authority) will advance a percentage of the sale price of one of the condo units accredited by their organization to be used towards the down payment.

Montréal Home Purchase Assistance Program: For first-time home buyers or experienced buyers with children under 13, you can receive a lump sum payment when purchasing a new property or a refund of your real estate transfer tax (welcome tax) when purchasing an existing property.

Accès Famille: Available in Quebec City, this program provides an interest-free, no-payment loan for 5.5% of the purchase price, more for Novoclimat-approved homes.

New Brunswick Down Payment Assistance

New Brunswick Home Ownership Program: Provides loans up to $75,000 for first-time home buyers or anyone living in a substandard housing unit who has resided in New Brunswick for at least one year.

Nova Scotia Down Payment Assistance

Nova Scotia Down Payment Assistance Program (DPAP): This program offers interest-free repayable loans of up to 5% of the home’s purchase price to eligible Nova Scotia residents.

Prince Edward Island Down Payment Assistance

PEI Down Payment Assistance Program (DPAP): This is a repayable loan of up to 5% of the home’s purchase price, up to a maximum of $17,500 for Prince Edward Island residents. Furthermore, the purchase price of the home cannot exceed $350,000.

Newfoundland and Labrador Down Payment Assistance

Newfoundland First-Time Homebuyers Program: Eligible first-time home buyers in Newfoundland receive a repayable loan of up to 5% of the purchase price for a down payment. The total loan amount is based on a sliding scale. In addition, home buyers can also receive a grant of 50% of legal closing costs, up to a maximum of $1,500.

Northwest Territories Down Payment Assistance

Home Purchase Program: First-time home buyers who have lived in the Northwest Territories for at least three years can receive a forgivable loan of up to 5% of the purchase price in specific communities. Moreover, home buyers must have resided one continuous year in the community of application.

Nunavut Down Payment Assistance

Nunavut Down Payment Assistance Program: Eligible home buyers who have lived in Nunavut for at least one year and who do not own any residential property in the community at the time of application or within the previous five years can receive a forgivable loan of up to $80,000 for a down payment and closing fees.

If your province isn’t included in this list, contact the local government to learn more about what programs are available. Program status and availability can change quickly, so do your research and contact local governments for the latest program information.

Frequently Asked Questions

What Is a Down Payment Assistance Program?

Down payment assistance refers to providing financial aid to qualified Canadians seeking to purchase their initial home but requiring assistance in obtaining a significant amount for a down payment.

How Do Down Payment Assistance Programs Work?

Down payment assistance programs generally provide a grant or loan to the homebuyer, which can be used towards the home’s down payment and closing costs. The assistance available will depend on the program and the applicant’s financial situation and may be subject to certain restrictions and eligibility criteria.

What Incentives Are There for First-Time Home Buyers?

Governments and financial institutions often offer incentives to encourage first-time home buyers to enter the housing market. For example, some common incentives include tax credits and rebates, reduced interest rates, and more.

What Is the Minimum Down Payment for a House?

The minimum down payment in Canada to purchase a home depends on the property’s purchase price, for instance: