The home hunting process is long, and it’s not over once you land an accepted offer. While getting to that point might have been gruelling, there are many more steps to take before getting the keys to your new home.

You’ll need to complete a slew of tasks, including performing property inspections, securing home insurance, working with a real estate lawyer to finalize the transaction and securing final mortgage approval.

While you may already have a mortgage pre-approval in place (and we recommend that you do), that doesn’t guarantee you’ll get final approval. You’ll need to take several steps to move your mortgage pre-approval to the final approval stage.

Key Takeaways

- Getting pre-approved gives you valuable information and can help with the mortgage approval process.

- There are several documents you will need for your mortgage application. Make sure you have everything gathered in advance to speed up the process.

- Changes to your financial or employment status during your mortgage application can derail your chances of getting a mortgage.

Mortgage Approval vs. Mortgage Pre-Approval

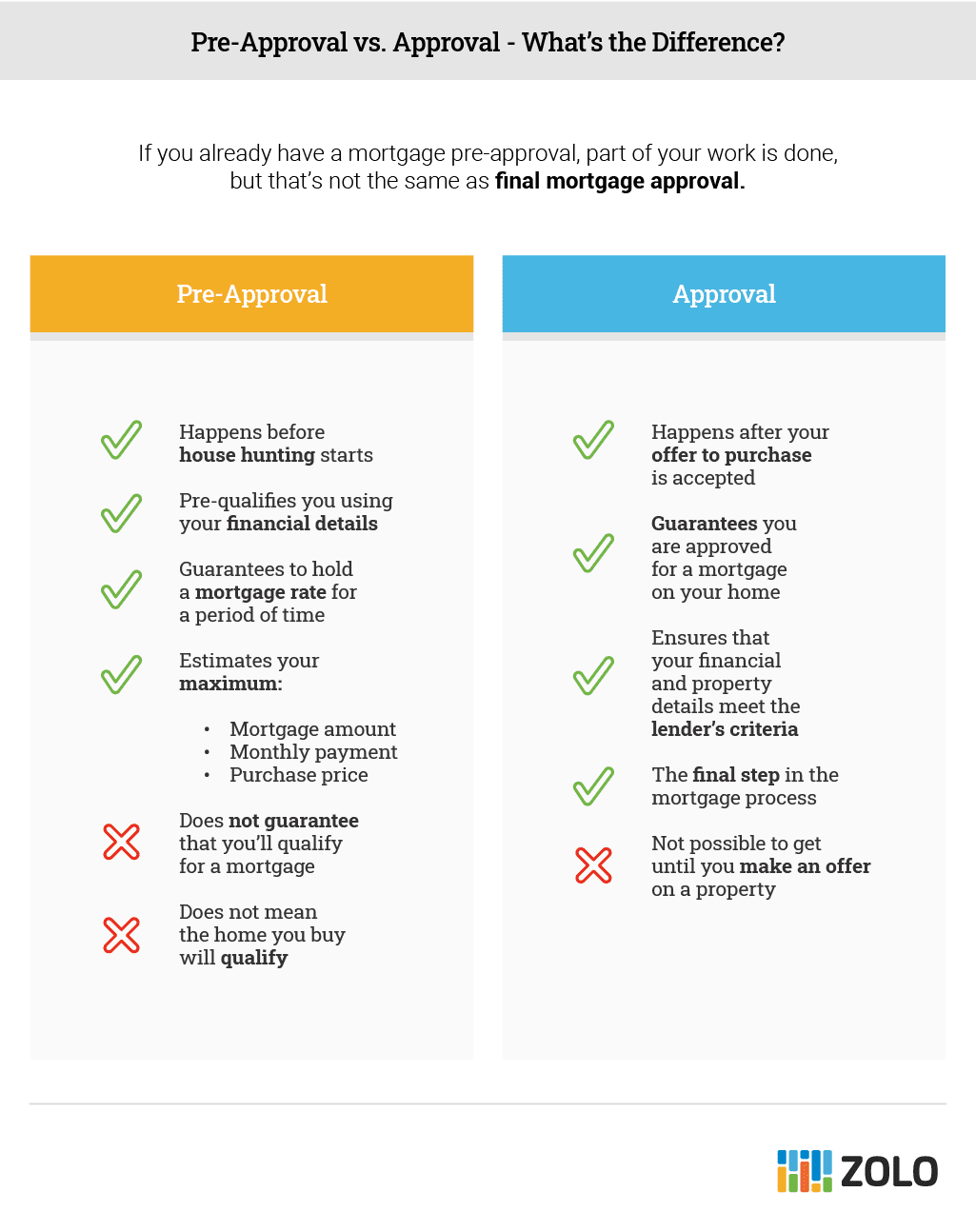

If you’ve already received mortgage pre-approval, you might be wondering: what’s the difference between mortgage approval and the pre-approval you already have? While the two are essential parts of the mortgage process, they are very different. Here’s how they differ:

Mortgage Pre-Approval Is:

- A pre-qualification using your essential financial information like your income, down payment amount, credit score, and debts

- A guarantee to hold a specific mortgage interest rate for a period of time

- An estimate of how much mortgage you can afford, your maximum purchase price and monthly payment based on your financial profile

A mortgage pre-approval estimates your mortgage details based on your financial profile. However, it does not guarantee that you’ll qualify for a mortgage or that the property you eventually purchase will be eligible for a mortgage. For those types of guarantees, you’ll need final mortgage approval.

Mortgage Approval Is:

- A guarantee to fund a mortgage based on your financial profile, your property’s details, and certain conditions that must be satisfied

- A verification that the property you want to buy meets the lender’s criteria

Getting Pre-Approval Makes Your Life Easier

While pre-approval doesn’t (and can’t) guarantee that you’ll get a mortgage, it’s still an essential step in the home buying process. Getting pre-qualified for a mortgage gives you valuable information about how much you can afford to spend on a home, your maximum monthly mortgage payment, and your mortgage interest rate. Obtaining pre-approval before you start your home hunt can also show you if there are any red flags in your financial profile that may prevent you from affording your dream home.

What Is Mortgage Approval and When Does it Happen

Mortgage approval happens after you have an accepted offer on a home. It is formalizing your pre-approval using the details of the specific property you plan to purchase.

Finalizing your mortgage approval involves completing paperwork regarding your income, down payment, assets and debts. Suppose you already have a mortgage pre-approval with this lender. In that case, you won’t have to submit the same information again unless your financial situation changes. If you haven’t submitted any information to your lender, this checklist outlines everything you’ll need.

To qualify for a mortgage, you’ll have to submit details about the property because the lender uses it to secure the loan. They will need to ensure you aren’t overpaying (and may sometimes require an appraisal) and that there are no substantial defects.

Documents Required for Mortgage Approval

The documents required may vary depending on your lender or mortgage broker. However, you should have the following documents ready to submit:

- Proof of employment and income: This could include recent pay stubs, direct deposit records, T1 General tax return with your Notice of Assessment, proof of employment, and proof of any additional income you make, like self-employment income

- Proof of down payment: You will need a record of withdrawal from your RRSP or FHSA, a statement of savings from the last three months, a sale agreement or a letter to confirm a gifted payment if applicable

- Financial details: This could include your assets and liabilities, void cheque and a pre-approval certificate

- Property documentation: They will also need the real estate listing, sale agreement, full address, added housing cost estimates (like property tax) and your lawyer’s contact information.

How to Get Approved for a Mortgage in 5 Steps

When you get an accepted offer on your new home, you’ll probably be ready to pop a bottle of champagne and celebrate! While it is a milestone, there are many steps to take before you hold the keys to your new home in your hand.

Angela Calla, accredited mortgage professional and host of The Mortgage Show, says you should expect to have five to seven days to finalize all of the details and documents related to your mortgage approval. Here are the five steps you’ll take.

1. Processing Your Mortgage Approval

After your offer to purchase is accepted by the seller, let your lender know, and they’ll start processing your mortgage approval. Send your lender details about the property, including the price. Your lender will verify your application details. They may call your employer to confirm your position or request a property appraisal

2. Conditional Approval

When your lender or mortgage broker finishes their due diligence, they’ll issue a conditional approval document. A conditional approval outlines all of the details of your mortgage, including the amount, the amortization schedule, your prepayment privileges, whether your mortgage is portable and more. Your conditional approval document also has areas for you to fill in and sign. These sections tell your lender how mortgage payments will be withdrawn from your account, at what frequency, and which real estate lawyer you’ll use.

The approval of your mortgage is “conditional,” which means that your application meets the lender’s requirements. As long as certain conditions are met, you will be approved. These conditions could include:

- Paying off an outstanding loan

- Getting an appraisal

- Verifying your employment income

- Acquiring adequate insurance

- Selling your current home

You’ll sign your conditional approval before meeting the terms above and then work on satisfying the conditions.

3. Mortgage Instructions

Once you’ve submitted all of the required paperwork to your lender and all conditions have been met, the lender will send “mortgage instructions” to your lawyer, and you can consider your funding formally approved. Once your lawyer receives their mortgage instructions, they will act to register your mortgage with your local land titles office and transfer the title of the property to you. To finalize these last steps, you might need to provide your lawyer with a fully executed offer to purchase.

4. Paperwork and Down Payments

Once your real estate lawyer receives the mortgage instructions, you’ll meet with them to finalize your paperwork and provide your down payment, and closing costs money.

5. Closing Day

On the closing date, your lender will transfer your mortgage funds to your lawyer’s trust account, and the lawyer will distribute the money to the sellers. The lawyer will register your name on the title if they haven’t already. Finally, your real estate agent will provide you with the keys to your new home.

Factors that Could Derail Your Mortgage Approval

The closing period of the homebuying process is a complex time with many steps that need to be completed. But it’s important to remember that your mortgage approval isn’t guaranteed at that time, and changes to your financial situation could derail the process. Here are some factors that could affect your mortgage approval.

- Exaggerating your finances

- Changing employers

- Applying for new loans (including credit cards, personal loans, and car loans)

- Closing old or unused credit cards (causing a drop in your credit score)

These changes could negatively impact your mortgage approval and might even cause your lender to withdraw their offer. Which would mean you’ll have to start back at square one to approve financing. For this reason, it’s essential to make no changes to your financial situation before you close on your new home.

Mortgage approval might seem like a stressful process. After all, you’re dealing with lawyers and one of the most significant purchases you’ll make in your lifetime. But if you’ve already been pre-approved and you’re purchasing an average home, just follow the steps above, and you’ll be well on your way to homeownership.