Being a homeowner is a big responsibility. You must make regular mortgage payments, cover your property taxes, and continue paying for all your other day-to-day expenses. But you also have to do the work to maintain your asset.

As November is Financial Literacy Month, we were curious how secure Canadian homeowners feel when facing an unstable economy. We also want to know whether homeowners are ready for potential increases to their mortgage payments if they’re close to renewal time. To determine the reality, we launched the Canadian Homeowner Economic Stability Survey.

87% of Canadian Homeowners Have an Emergency Fund

For the past two years, we’ve asked Canadians how soon they would run out of money and be unable to pay the bills if they lost their job. In 2020, 78% of people would run out of money in 90 days or less. In 2021, 76% said the same. This year, 83% of respondents would be able to go at least 30 days before running out of money to pay their bills.

Of the 83% with savings, 24% have more than 180 days worth of money to put towards their essentials if they were to lose their job. During the pandemic, the Bank of Canada found that Canadians were spending less than in years past. This is due to travel and entertainment services closing — or because they were being cautious about money and staying healthy. In turn, they found Canadians had saved around $5,800 per person in 2020. We couldn’t spend, so we saved! And we put those savings into our emergency funds.

Pre-pandemic, a 2019 Refresh Financial survey found that 49% of Canadians had no savings for an emergency. In 2020, a similar Ipsos survey by Global News found that three in 10 Canadians wouldn’t be able to pay their bills if they lost their job due to COVID-19. But, now that we’ve been through many unexpected emergencies and a few years of reduced ability to travel and spend on non-essentials, Canadians have changed their savings habits.

How Much Do Homeowners Have Saved?

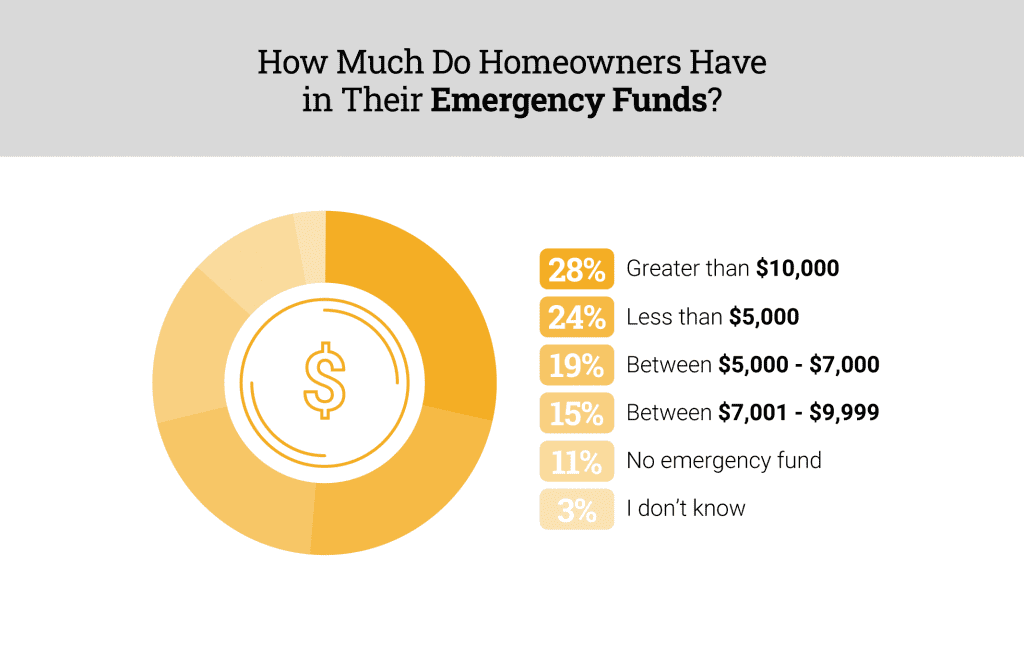

Our survey results found that most Canadian homeowners have an emergency fund, and they’ve saved a surprising amount. Only 11% of homeowners don’t have an emergency fund, and 28% of respondents have more than $10,000 saved.

“Homeownership is costly,” says Jordann Kaye, spokesperson for Zolo. “Unexpected expenses can range anywhere from a few hundred dollars to replace a broken appliance to tens of thousands of dollars to repair a rotting roof or remedy a leaking basement.”

She says it’s often more than the average Canadian can easily absorb within their budget. For that reason, Kaye suggests that a plan to deal with unexpected expenses, like an emergency fund, can be useful. Luckily, Canadians are on track.

Did Homeowners Save for Rising Mortgage Rates?

Emergency savings may come in handy for many homeowners soon because many are about to have bigger concerns than whether they can afford emergency repairs. Some Canadians could struggle to afford their new mortgage payment after they renew their mortgage because interest rates have been steadily rising.

The Bank of Canada’s (BOC) interest rate strongly influences mortgage renewal rates. At the start of 2022, the BOC interest rate was 0.25%. It’s now at 3.75%, with the most recent BOC increase on October 26, 2022. These increased rates have affected mortgage rates. For example, according to Ratehub.ca, the average 5-year fixed discounted mortgage rate was 1.39% in February 2021. Today, that rate is 4.69%.

An increase of a few percentage points may not seem like a big deal. But that increase changes a mortgage payment for a $5,000 loan amortized over 25 years from $1,973 to $2,833. That’s a difference of $860!

In short, higher rates equate to higher monthly mortgage payments at renewal.

Canadian Homeowners Worry About Mortgage Renewal

if you’re up for mortgage renewal in the next few years, you could find yourself in a tight spot financially. Canadians who are unprepared for an increase in their mortgage payment could find themselves scrambling to make ends meet. Most Canadians are well aware of the risk of rising rates. But still, they worry about being able to afford their mortgage payments at renewal.

Lana Brown is one such Canadian. She owes $411,000 on her Calgary, Alberta condo. Her mortgage is up for renewal at the end of March 2023. “We were going to wing it and wait,” says Brown. “But now we made an appointment for early renewal.”

Brown says she’s planning to shorten this renewal period from their typical five-year fixed rate to a two- or three-year fixed-rate mortgage. This is in hopes that their balance will be much lower or the interest rates settle by the next renewal.

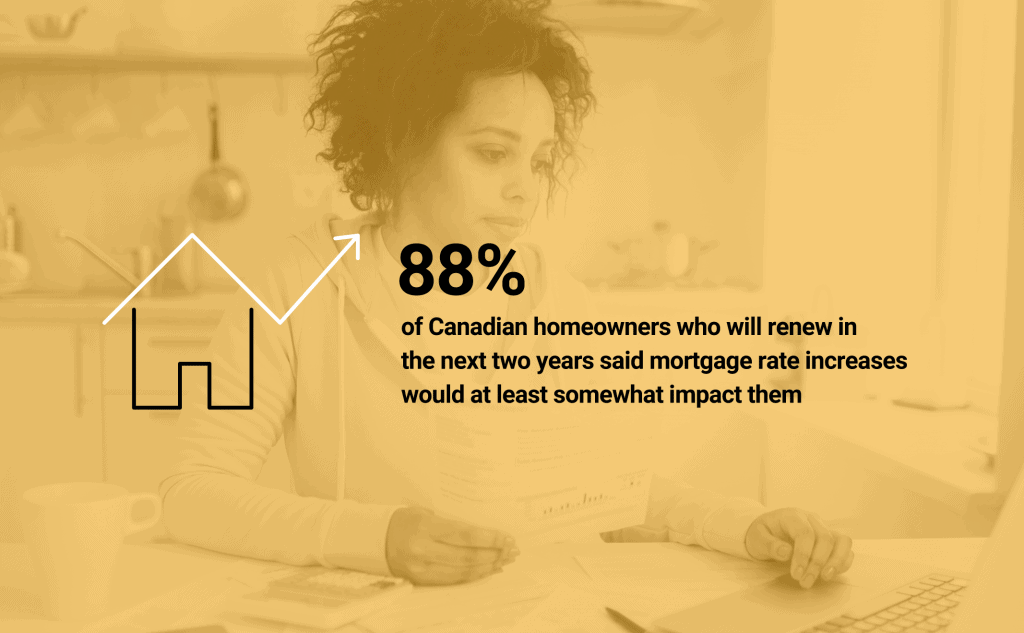

Brown isn’t alone. When we asked homeowners who will renew in the next two years whether higher rates impact their ability to afford their mortgage, 88% said these increases would at least somewhat impact them.

“We are nervous about the rate hikes,” says Tori Nowoczin, a detached homeowner in Okotoks, Alberta. She and her partner are up for mortgage renewal this January. “It seems that our wages don’t go as far anymore, so there’s certainly concern about how to manage a higher mortgage.”

How to Prepare For Higher Mortgage Interest Rates

If you’re one of the Canadian homeowners whose mortgage is up for renewal, let’s go over the top things you can do to prepare financially.

First off, working with an experienced mortgage broker is key. “They’ll holistically review your financial position, cash flow, budget and financial goals,” says Eden Simari, senior mortgage broker. She says they do this to understand how rising interest rates may impact your current mortgage, a new transaction or upcoming renewal.

Kelsey Burgess and her husband will be renewing their mortgage in 2024. “We’ve had some job changes, which resulted in salary changes, and have made some lifestyle changes to accommodate that,” says Burgess. “But if interest rates continue to climb, I’m concerned we won’t be able to afford payments when it comes time for renewal.”

If you’re worried about having to renew your mortgage in the next two years, Kaye shares her top advice for homeowners:

#1. Have an Accurate Perception of Your Financial Risk

That means understanding how your mortgage payment will be affected based on interest rates at renewal. Unfortunately, we don’t have a crystal ball that you can look into and know what interest rates will be at renewal. As a result, consider calculating your mortgage payments at today’s interest rates. You should also do separate calculations with interest rates that are several percentage points higher and lower than today’s rates.

#2. Plan How You’ll Pay Your Mortgage if Rates Rise Further

Make a mock budget with the higher mortgage payment, and observe how your budget changes. Is there room to save and pay down debt? Where will you cut to make ends meet? Creating a mock budget will help determine whether you can afford the worst-case scenario.

#3. Take Evasive Action

You can take many steps to reduce your risk and make more room in your budget for possibly higher mortgage payments. For example, you could make a lump sum payment on your mortgage. Or prioritize paying down other debts or work to increase your income.

Ultimately, Simari says that interest rates are always subject to change. “But, some Canadian economic forecasts suggest that price stabilization in the coming year may be on the way.”

She says it may not be the 2% pricing we saw throughout the pandemic, but it would be a potential reprieve from our current 5% and beyond.

44% of Canadian Homeowners are Worse off Financially Thanks to the Pandemic

A Statistics Canada study looking at the impact of the pandemic on Canadians found that most people have had difficulty meeting their financial needs. But that doesn’t mean everyone has been experiencing this type of crisis.

Instead, we found that Generation Z homeowners feel that they are doing better financially now than they were at the start of the pandemic. Unfortunately, millennials, Generation X and Boomers don’t feel the same. They report they are worse off financially today than two years ago.

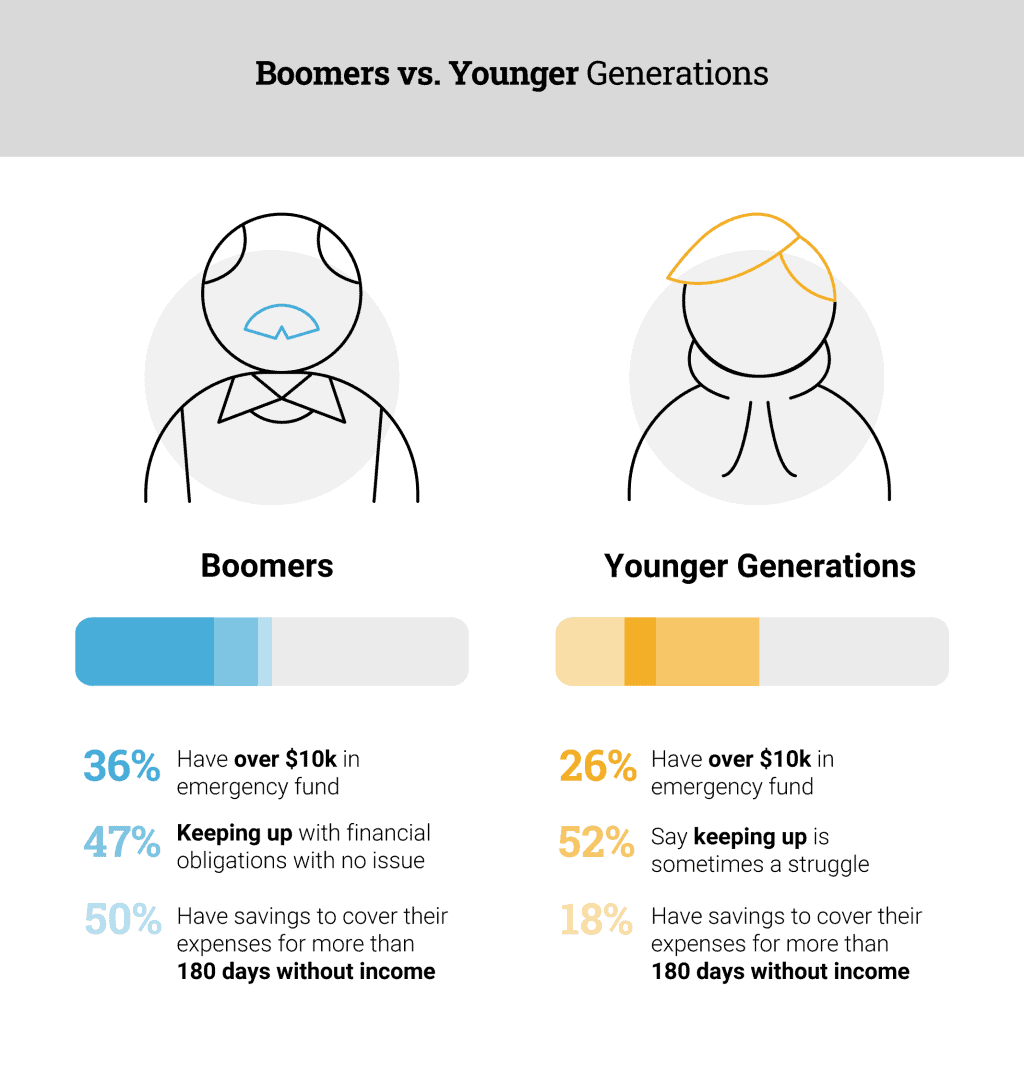

Although Generation Z is feeling the most optimistic about their finances, the generation seeing the least amount of financial struggle is Boomers. We asked homeowners to think back over the past 12 months and describe how well they have been keeping up with their bills and other financial commitments. Generation Z, Millennials and Generation X say that keeping up is sometimes a struggle. But, Boomers say they’re keeping up without any problems.

Boomers also have the heftiest emergency funds, with 36% saying they have more than $10,000 in their accounts. 50% of Boomers would also be able to go more than 180 days without an income if they lost their job today. All other generations would run out of money within zero to 60 days.

Emergency Savings Isn’t Enough to Avoid Anxiety

Homeowners are doing well financially, keeping up with their bills, and have emergency savings. But, an impending recession is enough to cause anxiety and a lack of confidence in their ability to continue to thrive.

“It’s normal to worry about the unknown, but planning is the best way to minimize that worry,” says Kaye. “By calculating possible outcomes, you’ll have a clearer picture of the actual impacts of rising interest rates and the ability to make a plan to protect yourself.”

Survey Details

The Zolo Canadian Homeowner Economic Stability Survey data was collected through an online survey between October 7 and 10, 2022.

The online survey asked 500 respondents a variety of opinion, self-report and knowledge-based questions to measure financial knowledge, confidence and skills — all of which are integral to financial literacy.

The estimated margin of error is +/- 4 percentage points.