Saving for a down payment can feel like climbing Mount Everest. For many Canadians, saving for a house takes years, often tapping multiple sources of funds. For instance, in Zolo’s 2024 housing market report, 48% of Canadians used money from their or their partner’s parents and relatives for at least part of their down payment.

While the average home price in Canada is trending down, the national benchmark home price was $712,200 in March 2025, which would require a down payment of at least $46,220–that’s no small sum. With that in mind, here’s how to save for a down payment on a house so you can enter the housing market as soon as possible.

Key Takeaways

- The minimum down payment in Canada is determined by the home’s purchase price and can range from 5% to 20%

- Homebuying incentive programs could help you become a homeowner sooner

What Is a Down Payment?

A down payment is a sum of money paid upfront to buy a home. It is subtracted from the purchase price; typically, a mortgage covers the rest.

In Canada, a down payment is required, and it directly influences mortgage interest rates, the total cost of the mortgage, and whether mortgage loan insurance is required.

How Much Do I Need for a Down Payment?

The Canadian government sets the minimum down payment amounts. If you are buying a primary residence, the minimum down payment changes depending on the home price:

For example, if you purchase a home for $500,000, the minimum down payment is $25,000, or if you buy a house for $800,000, it is $55,000.

It’s important to note that if you purchase a home with a down payment of less than 20%, you will be required to purchase mortgage default insurance. Mortgage default insurance, also called CMHC insurance, protects the lender if you stop making mortgage payments. The cost of the insurance premium is typically added to your mortgage and paid off over time with your mortgage payments.

How to Save for a Down Payment

For many Canadians, the best way to start saving for a down payment is to set a down payment goal and create a savings plan.

Identify Budget for Buying a Home

Before you start looking at houses for sale, it’s important to determine what you can afford. Your maximum purchase price is based on the size of your down payment and mortgage. That being said, it’s essential to consider your personal budget before you buy a home at the top of your price range.

In addition, you’ll need to budget for closing costs, which include legal fees, land transfer taxes, title insurance, and other administrative fees. Closing costs could range from 2% to 4% of the purchase price, depending on where you live and the type of property you buy.

If the type of home you want to buy typically costs around $500,000, then your down payment savings goal should be at least $25,000, and you should save an extra $10,000 to $20,000 for closing costs.

Identify a Timeline

While you may want to buy a home as soon as possible, building your down payment fund often takes time. If you plan to purchase your first home in two years, you can divide the amount you need to save by your timeline. For example, to save $35,000 in two years, you need to save $1,458 per month or $673 biweekly. The good news is that certain savings and investment accounts can help you save through interest and tax breaks.

You may need to adjust your timeline depending on how much room you have in your monthly budget. For instance, if you save $900 per month, you will reach $35,000 in three years and three months.

Create a Savings Plan

Once you’ve figured out how much you need to save, a savings plan can help you achieve your goal. There are many different savings strategies. One option is to create an automatic transfer to your savings or investment account on each payday.

In addition, tax refunds and bonuses could help boost savings and get you to your down payment goal sooner.

Establish a Separate Savings Account

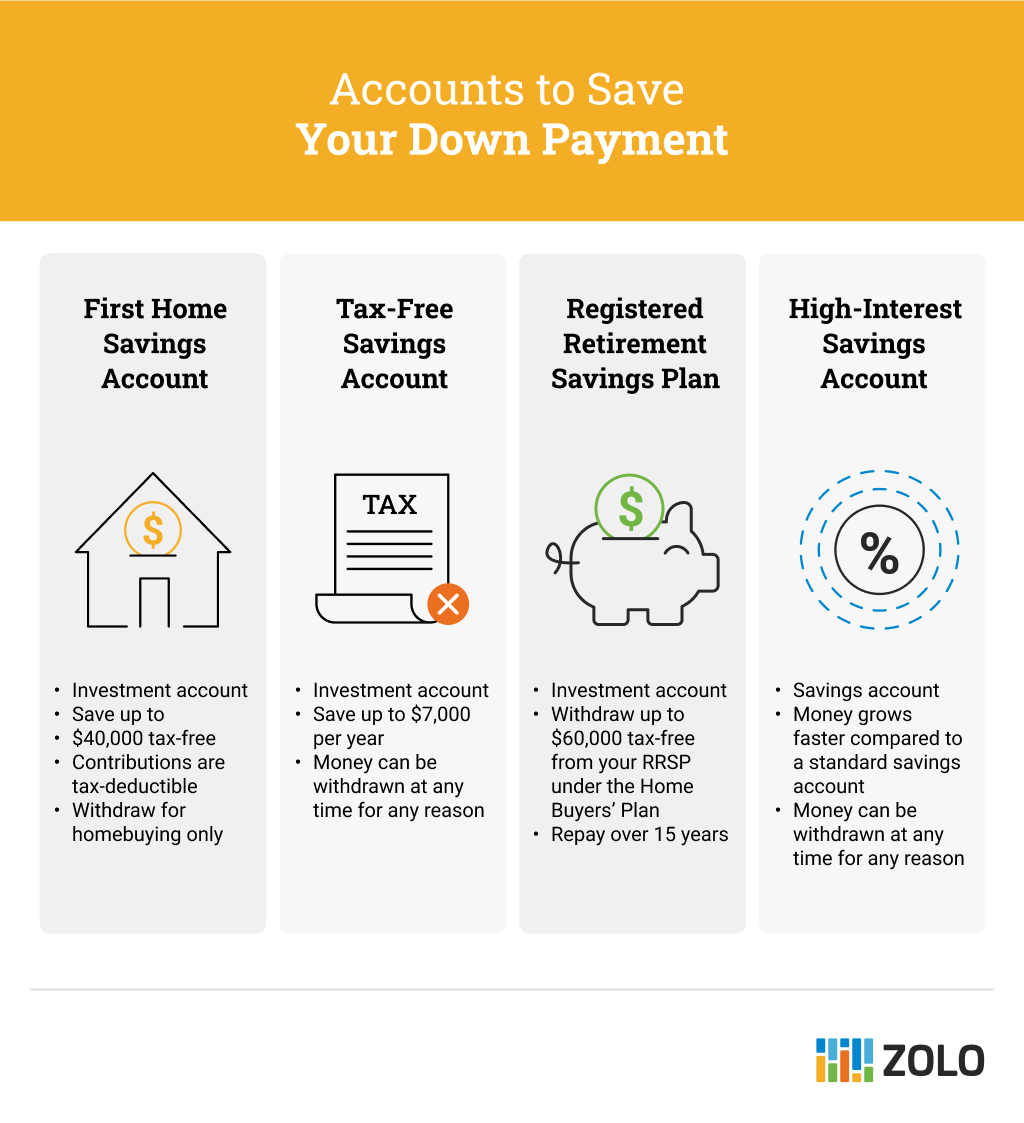

Before you start saving your down payment, you’ll need to decide which type of account you should use. There are multiple options available, each with its pros and cons. But you can opt for a combination of accounts that work best for you.

First Home Savings Account (FHSA)

The First Home Savings Account allows first-time homebuyers to save up to $40,000 tax-free. An FHSA can hold investments like mutual funds, bonds, publicly traded securities, and GICs so that your money can grow tax-free. In addition, any contribution made to an FHSA is tax-deductible, which lowers your taxable income on your tax return.

Open your First Home Savings Account with Questrade online and start saving for your first home!

Tax-Free Savings Account (TFSA)

A Tax-Free Savings Account is another type of investment account, but unlike an FHSA, you can withdraw money from a TFSA anytime for any reason. In addition, withdrawals are tax-free. However, contributions are not deductible on your personal income tax. Currently, the contribution limit is $7,000 per year, but your personal contribution limit may be higher, depending on how much you’ve contributed in the past.

Registered Retirement Savings Plan (RRSP)

While the Registered Retirement Savings Plan is an investment account designed to save for retirement, you can withdraw up to $60,000 tax-free from your RRSP under the Home Buyers’ Plan. Importantly, you must repay these funds to your RRSP within 15 years. If you’ve already been contributing to an RRSP, withdrawing funds may help you buy a home sooner. However, it may affect your retirement goals, and you’ll miss 15 years of growth on the funds withdrawn.

High-Interest Savings Account (HISA)

High-interest savings accounts are available at many financial institutions. Typically, these accounts offer a higher interest rate than a regular savings account, and you can access the funds anytime for any reason. They are typically considered risk-free, as your money is not subject to market fluctuations. However, the interest you earn is taxable.

Explore Loan Options

You may get discouraged by the amount of money you need to save for a down payment, but some options can help you buy a home with a lower down payment.

Borrowed Down Payment

Some mortgage lenders will allow alternative funding sources for your down payment, such as a line of credit, personal loan, or borrowed from family. Before you choose this option, it’s important to consider how the additional debt will affect your personal finances.

Provincial Down Payment Loan Programs

Numerous provinces, territories, and municipalities offer down payment assistance programs for first-time homebuyers. They may offer forgivable or interest-free loans. Additionally, some programs require you to live in the area for a minimum amount of time. Check with your local government to learn what programs are available to you.

Explore Home Buying Incentive Programs

- First-Time Home Buyers’ Tax Credit (HBTC) – A federally administered and non-refundable tax credit that allows first-time homebuyers to claim up to $10,000 of costs related to their home purchase, which could result in income tax savings of up to $1,500

- Land Transfer Tax Rebate – Available to first-time homebuyers in British Columbia, Ontario, or Prince Edward Island, this rebate offsets the cost of land transfer tax, which ranges from 0.5% to 3% of the purchase price

- GST/HST New Housing Rebate – Offers you money back on the GST or HST you must pay when you build a house or substantially renovate an existing house.

How to Save for a Down Payment FAQ

Is $10,000 enough for a down payment?

If you purchase a home for $200,000 or less, $10,000 is enough for a 5% down payment. However, you will still need to budget for closing costs.

What is the 50/30/20 rule?

The 50/30/20 rule is a budgeting method that splits income into three categories: 50% for needs like housing, groceries, utilities, and insurance, 30% for wants like hobbies, dining out, and entertainment, and 20% for savings and debt repayment.

How do people afford down payments?

Many Canadians save for years to afford the minimum down payment on a house. In addition, by taking advantage of down payment assistance programs, you may be able to buy a home sooner.