Even before you call your lender to inquire about mortgages, car loans or any other type of debt, be smart and check your credit report. Unless you need your report immediately, you can get a free credit report with very little effort.

Where to Get Your Free Credit Report

There are only two major credit agencies in Canada: TransUnion Canada and Equifax Canada.

You can request your free credit report by going online or by filling out the consumer request form, found online at Equifax or TransUnion. (You can also phone the customer service number for either credit bureau and request the form be sent to you in the mail.)

It’s a good idea to request a copy of this free credit report from both agencies, as there could be differences in the reporting history. Although credit reports don’t generally include your credit score, you’ll learn critical information about your credit history and get a chance to check for any errors that may be included in your report.

Should You Check Your Credit Score?

Daily, weekly or monthly monitoring of your three-digit credit score isn’t necessary; however, if you plan on making a major purchase, need approval for credit or a loan, or in the process of rebuilding (or building) your credit rating, then checking your credit score is a good idea.

The good news is that these days there are a few ways you can check your credit score.

How to Check Your Credit Score?

The first option is to pay one or both of the credit agencies a fee, typically between $10 and $50, for access to your credit score (and, potentially, your detailed credit report).

Another option is to go through an external agency, such as your credit card provider, your financial institution, or a financial tracking app. These providers usually offer access to check your credit score for free as an incentive for being a (paying) customer for their brand or service.

For example, RBC offers their banking clients free access to their credit scores, but most clients also end up paying a monthly banking fee, so the ‘free’ credit report is because you pay for RBC’s account services.

A final option is to sign up for a free credit report or pay a third-party company to access your credit score; however, it pays to be careful. While most third-party companies are legit, there are scams. Be sure to check the credentials of the company before providing personal information.

More Than One Credit Score?

In Canada, there are two major credit agencies responsible for collecting consumer data and creating the algorithms used to create credit reports that determine credit scores.

But both credit agencies, Equifax and TransUnion, use multiple algorithms to produce multiple credit scores — even for the same person!

This discrepancy boils down to privacy and proprietary need. Each bank or business who pays to use credit scores requires their own, specifically tailored algorithm — which is a calculation based on a set of criteria that’s defined by that bank or business. Since each lender will vary in how they measure and treat risks, the algorithms that produce credit scores can vary and this results in different scores for the same person.

In most cases, the difference between multiple credit score algorithms is so small it doesn’t make a difference; however, there are some circumstances where a few points can have a dramatic effect.

For instance:

- Lender A’s algorithm could calculate your credit score at 660, giving you access to a mortgage rate of 2.75%

- Lender B’s algorithm could calculate your credit score at 659, giving you access to a mortgage rate of 2.95% (or, worse, put you in the private lender market, with even higher rates).

“Credit scores are like salad dressing,” explains Julie Kuzmic, director of consumer advocacy for Equifax Canada. “There are a number of different brands offering their own variations of salad dressing. Each may have their own recipe, but all are offering Caesar-style dressing.”

Kuzmic explains that it’s not unusual to have variation among those scores; most are minor but some differences result in 100 points or more between various credit score results.

Bottom line: If you don’t like the terms one lender is offering, start shopping around.

How Are Credit Scores Calculated?

All credit scores factor in five main criteria and each is weighted based on its significance. Typically, the order of importance for the criteria used to calculate your credit score is:

- Your payment history (35%)

- The amount of debt you hold (30%)

- The length of your credit history (15%)

- The number and type of new credit applications (10%)

- Your credit mix (10%)

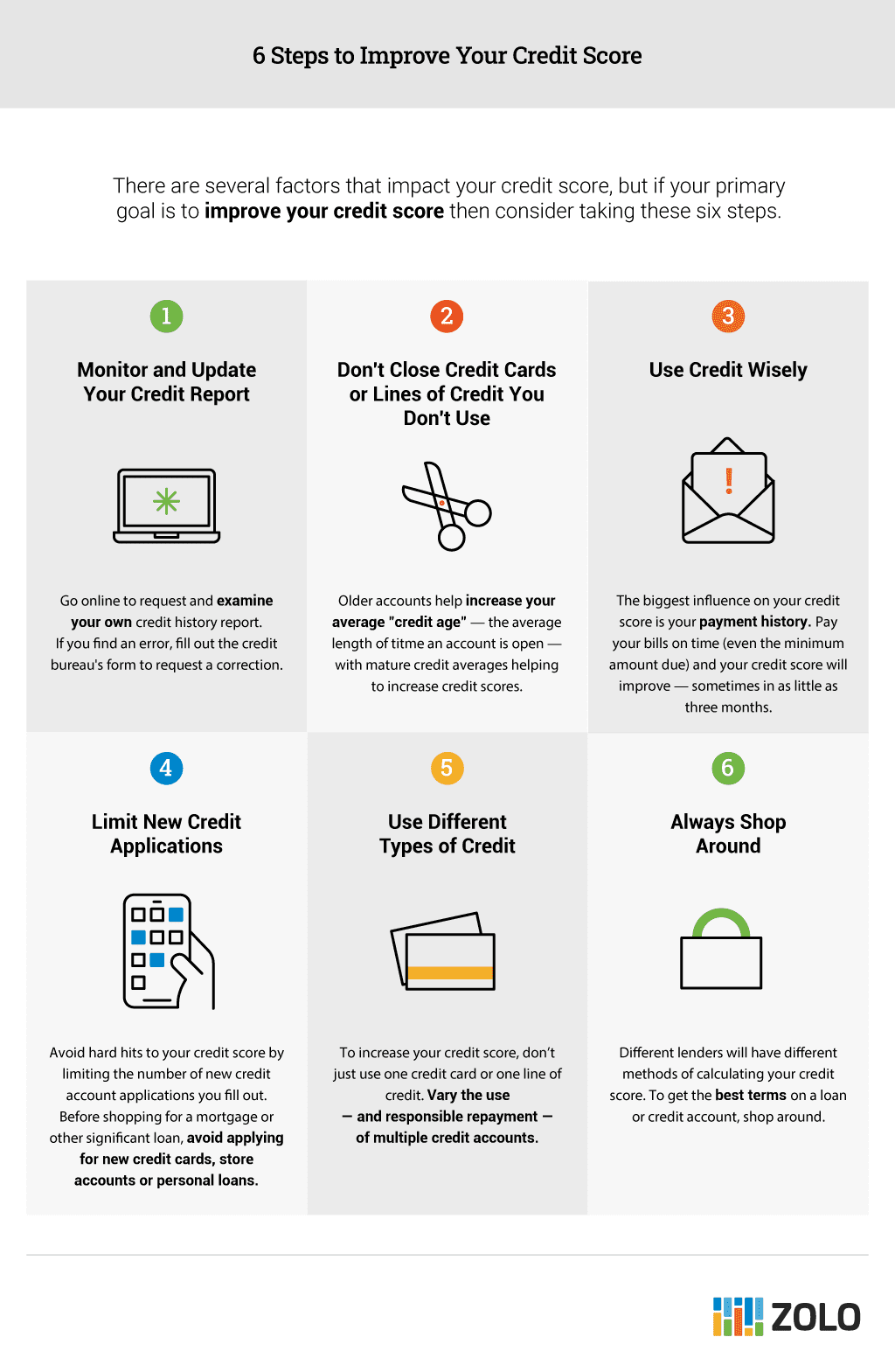

6 Tips for the Best Credit Score

If you want to improve your credit score — or build an excellent credit rating — follow these tips:

#1. Always Pay Your Bills By the Due Date

Your payment history is the single most important factor when it comes to calculating your credit score. Above all else, lenders want to know how likely you are to pay them back.

To assess this risk, lenders look at your payment history, which is considered a reflection of how you treat debt and debt repayments.

People who consistently pay back their debts get top marks in this category — making this the number one factor in improving your credit score.

Even if you can only pay the minimum amount due, it’s still better to pay this nominal sum, either on or before the due date, then to skip a payment or pay late.

#2. Be Consistent

While most credit agency algorithms only use 12 to 36 months of payment history to calculate your credit score, virtually all calculations will go back six or seven years to include any late payments, default or bankruptcies.

To avoid being penalized, be consistent about always paying your bills on time. Set up reminders in your calendar or get e-bills sent to your inbox.

For those undertaking credit repair, the good news is the older the late payment or default, the less of an impact it has on your credit score. “That’s because almost all algorithms weigh heavily on recency,” says Kuzmic.

#3. Avoid the Tilt Factor

In poker, a poor state of mind can lead a play to make costly mistakes. Born out of frustration, this state of mind is called ‘tilt’ and usually results in big losses (and even bigger regrets).

In the lending market, the same tilt mindset can occur when frustrated (or impatient) borrowers max out their credit lines. Turns out part of the credit score calculation takes into account how much credit you have access to and compares that to how much debt you’ve taken on. The closer you are to the maximum lending amount, the higher your credit utilization and the higher your credit utilization the lower your credit score will be.

The key to avoiding the title factor is to have access to lots of credit, but don’t use it.

It’s also why many financial planners will advise against closing lines of credit or cancelling old credit card accounts. As long as these accounts aren’t costing you out-of-pocket fees, it’s better for your credit score to keep them open.

#4. Your Credit Age Counts

Another reason to avoid closing old (and even unused) credit accounts is that they tend to have a positive impact on your average age of credit accounts.

A longer history of borrowing and paying back debt leads to higher average age of credit accounts and this means a higher credit score.

It’s also why opening up multiple new credit accounts is almost never a good idea unless you are starting to build your credit history (at which point, it’s a great idea to open up multiple accounts, and then slowly use and consistently pay back the credit used).

#5. Avoid Applying for New Credit Before a Big Purchase

New credit, or a number of recent applications reflects poorly and lowers your credit score.

Adding new loans or applying for multiple new credit accounts is known as “credit shopping,” and lenders take it as a sign that you are struggling with finances. Even if this isn’t the case, any new application or approved credit account will lower your credit score, since the lender approving the application will need to check your credit report — verification that’s known as a ‘hard hit.’

For each new account, your credit score will drop between two and 10 points. In most cases, one hard inquiry is unlikely to play a huge role in whether or not you get approved for a new mortgage or loan, but a series of hard checks can hurt your chances. It’s why mortgage brokers strongly advise you not to apply for new credit cards, store accounts or personal loans shortly before shopping for a mortgage.

There is one exception: Mortgage lenders and lenders for car financing know that you will probably shop around to get a good rate.

“If a lender sees six mortgage-related hard-inquiries in a two-week period, they know the person doesn’t intend to buy six houses,” says Kuzmic. “The person is shopping for the best mortgage product.” As a result, these six inquiries will actually get grouped into one ‘hard hit’ against your credit profile.

For that reason, a series of hard checks in a short period of time for the same type of loan will be treated as one application. The key, however, is to make all these loan inquiries within a relatively short period of time.

“Some lenders only group similar credit hits in a 15 day period and others group similar hits within a 45 day period.” To be safe, Kuzmic suggests shopping for mortgages (and car loans) within a two-week period.

#6. Use Different Types of Credit

Always relying on one line of credit or one credit card can simplify your bill payments, but it can hurt your credit score.

Lenders want to see a variety of credit accounts on your file. Not only does this help build your credit history — and improve your credit score — but it proves to lenders that you can handle a variety of loans with a variety of payment requirements.

This factor starts to lose significance the longer you have good credit. However, for those just starting to build their credit history, or those looking to rebuild their credit, varying the type of loans you have, use and payback can really help to increase your credit score.