If you’ve been looking to purchase your first home, you’ve likely become frustrated with how much housing prices have increased over the last few years. While it’s wise to save up a decent down payment before applying for a mortgage, occasionally, a situation arises where you need to buy a home – but you don’t have a down payment. This leads you to wonder, “can you buy a house with no down payment?”

The answer isn’t straightforward, but we’ll examine your options if you want to enter the real estate market but don’t have the required 5% down payment to apply for a mortgage loan.

Key Takeaways

- The minimum required down payment in Canada is 5% of the home’s purchase price

- When reviewing your loan applications, your mortgage lender will consider your down payment size, credit score, credit history, debt levels, and employment to determine your trustworthiness

- Cash-back mortgages can sometimes help you buy a house, even if you don’t have a down payment

- Buying a home is expensive, and you’ll want to consider waiting if you don’t have enough money saved up for a minimum down payment

What is a Down Payment?

Your down payment is money you directly put toward the purchase of your home. It’s usually a percentage of the purchase price, with the remainder financed through a mortgage lender.

It’s crucial to note that your home down payment is just a percentage of the purchase price and doesn’t cover the other costs associated with buying a home. You must set aside extra money to pay the closing costs, such as legal fees, land transfer tax, and administrative fees.

What are the Minimum Down Payment Requirements in Canada?

The minimum down payment depends on the cost of your home. You need a 5% down payment for the first $500,000 of the home’s price. Then, you need 10% for the portion of the home’s price over $500,000 until $1,499,999. Any property over $1.5 million requires a 20% down payment.

Here’s a quick example of a home with a purchase price of $700,000. You combine two amounts to determine your minimum down payment:

First $500,000 x 5% = $25,000

Next $200,000 x 10% = $20,000

Total minimum down payment = $45,000

If your down payment is less than 20% of the purchase price, you’ll also need to buy mortgage default insurance. Your mortgage insurance premium is usually added to your mortgage balance, and you’ll pay it off over time.

Unfortunately, saving even the smallest allowable down payment for a home purchase can be challenging, so you may wish to explore buying a home without a down payment.

How to Buy a House With No Down Payment

How can you buy a house without a traditional down payment? In the past, “flex lender mortgages” were a common way to borrow money for your down payment. However, the CMHC tightened its rules surrounding borrowing money for a down payment in July 2020, eliminating the flex down benefit. That said, you still have some options.

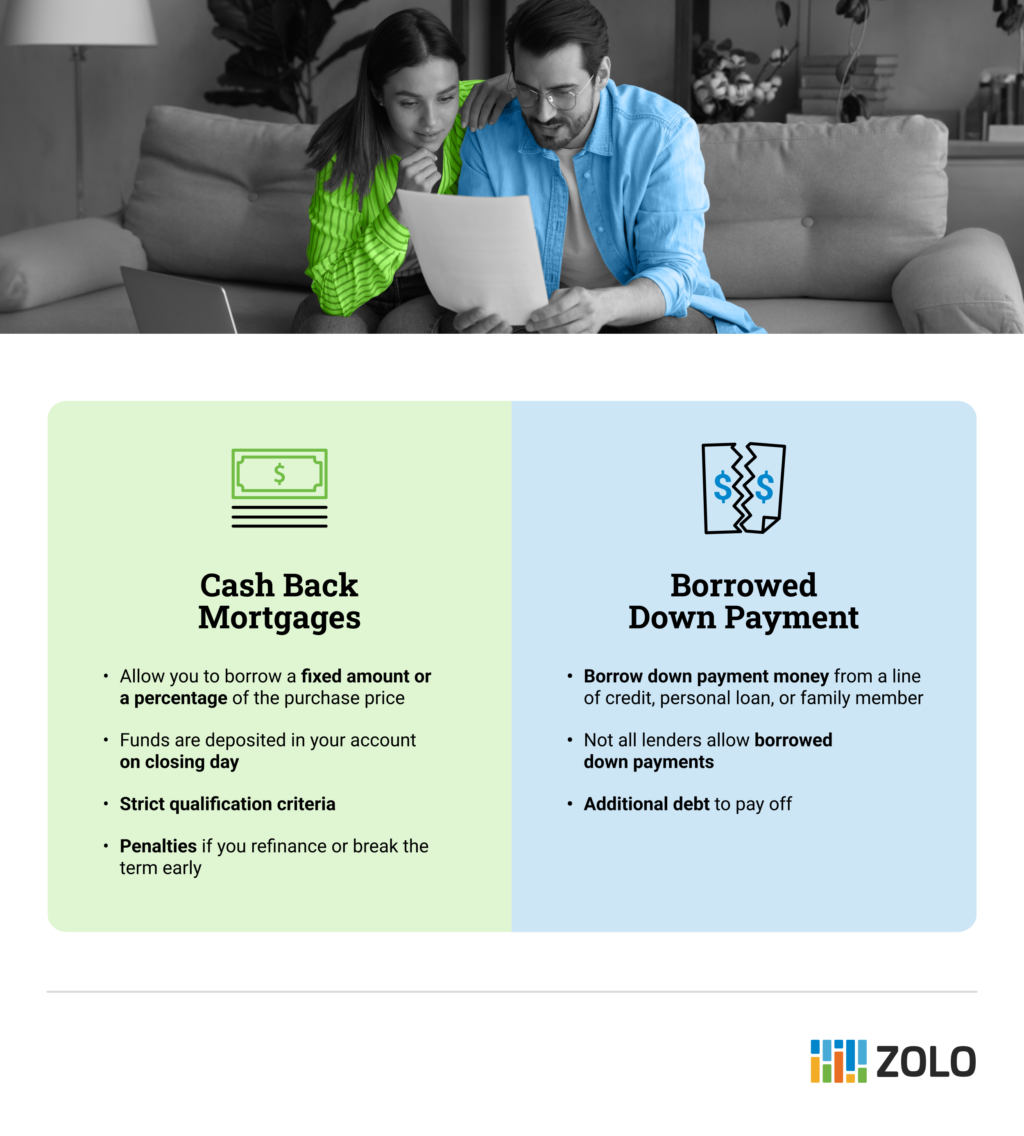

Cash Back Mortgages

A cash back mortgage will technically allow you to get a mortgage without a down payment in Canada. A cash back mortgage will enable you to borrow more money than needed to purchase your home. The additional funds you borrow can be a fixed amount or a percentage up to 7% of the purchase price, to a maximum of $20,000. The money is deposited in your account as a lump sum on the closing date. You can then use these funds as you wish.

For example, if you get approved for a $500,000 mortgage and set up a 4% cash back mortgage, you’ll receive the $20,000 when your home closes. You’ll then owe $500,000 for your mortgage and an additional $20,000 for the cash back portion of the loan.

What are the Requirements for a Cash Back Mortgage?

Since the lender has to take on further risks with a cash back mortgage because the loan amount exceeds the home’s value, strict qualification criteria exist, including:

- You must have stable income and employment, with no exceptions for self-employed individuals

- Your credit score must be at least 650

- Have a low debt-to-income ratio

- You have to be the occupant of this home, and you can’t rent it out

It’s essential that you understand the true cost of a cash back mortgage because there are penalties if you want to refinance or break the term early. The penalties can be as steep as being asked to repay all the borrowed funds on top of a prepayment penalty.

Borrowed Down Payment

If you want to put down 5% to make the minimum down payment on a home and you don’t have the money saved, here are some alternative loan options:

- Line of credit – While you can’t get a line of credit for your down payment from the same lender as your mortgage, you can apply at another bank

- Borrow the money from family – You can contact a relative to see if they would loan you the money to enter the real estate market

- Personal loan – These are generally easy to find if you have a decent credit score

Not all lenders will allow alternative sources of funding for your down payment. For example, some lenders only allow funds from family members if it’s a gift, not a loan. Confirm with your mortgage lender before purchasing the home to avoid costly penalties.If you require mortgage default insurance, it’s important to note that only Sagen and Canada Guaranty allow borrowed funds for a down payment.

How Do No Down Payment Mortgages Work?

With a traditional mortgage, you borrow the money you need to make the home purchase, which, when added to your down payment, equals the home’s purchase price. No down payment mortgages differ since you’re not putting your own money toward the home’s purchase price. While you always have to make a down payment to apply for a mortgage, it may be possible to use borrowed funds.

For example, let’s say that you borrow 5% to make the down payment for your $500,000 mortgage. This would mean you have an additional debt of $25,000 to apply to borrow for a home loan. Using this strategy is generally not advisable, as you’ll have a higher debt load, which could land you in financial trouble if you can’t keep up with your payments.

With a cash-back mortgage, you would get up to $20,000 back on the date your mortgage is advanced. These funds could be used to handle the urgent expenses associated with home ownership, like closing costs or purchasing new furniture.

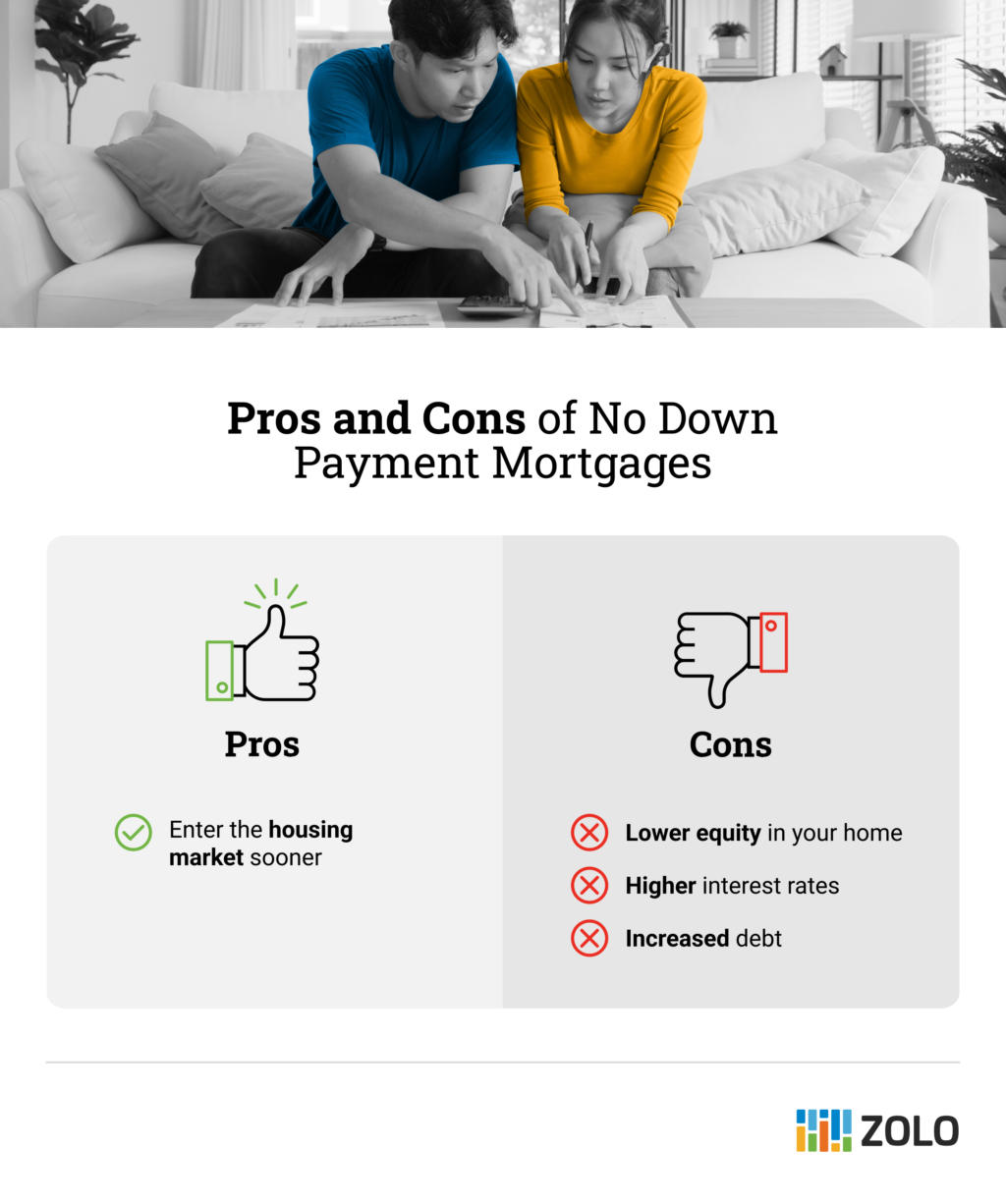

Are No Down Payment Mortgages a Good Idea?

You may still wonder about the merits of a no down payment mortgage as you enter the real estate market. It’s smart to make the biggest down payment possible. While this may be frustrating to hear, if you begin saving now, you can focus on saving up.

Here are the biggest drawbacks of a zero down payment mortgage. First, by borrowing your down payment, you’ll have limited or no equity, which means you’ll owe more than or equal to the home’s value. This will leave you vulnerable to any real estate market fluctuations.

For example, if you only have 3% equity and the market drops 5%, you would have an underwater mortgage, meaning you would owe more than your home is worth. You may make no profit or even owe money if you need to sell your home.

Second, a cash-back mortgage can have much higher interest rates than a typical mortgage, which may make it harder to make your monthly mortgage payments, especially if you experience financial hardship like job loss or illness.

As a result, we don’t recommend getting a mortgage with no down payment. Your ability to save a down payment is often a good indicator of whether you’re ready for the financial stress of homeownership. There are numerous costs associated with buying and owning a home, and a down payment is just the beginning.

Down Payment Assistance Programs in Canada

Instead of a down payment loan, you can take advantage of down payment assistance programs. These programs are designed to help first-time homebuyers get into the housing market faster. Here are some of the most popular programs:

- Home Buyers’ Plan (HBP) – A government program that allows first-time homebuyers to borrow from their RRSP for a down payment

- First-Time Home Buyers’ Tax Credit (HBTC) – Federally administered and non-refundable tax credit for first-time homebuyers valued at up to $1,500

- Land transfer tax rebate – Rebates to offset the cost of land transfer tax, which ranges from 0.5% to 3% of the purchase price

- Municipal or Provincial down payment assistance programs – Certain provinces or municipalities offer interest-free loans, forgivable loans or grants for down payments

Conclusion

If you’re struggling to save for a down payment to buy a house, you may be tempted to look into no down payment mortgages. It’s essential to remember that buying a home is a serious financial decision. Purchasing a home without sufficient funds for a down payment could put you in a vulnerable financial position. It’s worth reviewing your options, looking into down payment assistance programs, and waiting to save for a larger down payment if possible.

No Down Payment Home Purchase FAQs

What credit score do you need to buy a house?

Generally, the minimum credit score to be approved for a traditional mortgage is 680. However, some lenders’ requirements may be lower. If your credit score is lower than 660, consider contacting a mortgage broker or applying for a mortgage through a credit union or alternative lender. On the other hand, you can improve your credit score, save for a larger down payment, or consider adding a co-signer or guarantor.

Can I borrow money for a down payment on a house?

In some cases, you can borrow money for a down payment as long as you pass their minimum requirements. Sagen and Canada Guaranty allow borrowed funds for down payments on insured mortgages from sources such as personal loans, lines of credit, and gifts.