Buying your first home in Canada is never easy, and many Canadians need help with affordability and saving up a down payment. To alleviate some of the stress that comes with saving for a down payment, the government introduced the Tax-Free First Home Savings Account, which became available in 2023.

As of April 2024, more than 750,000 Canadians have opened a FHSA to help them save for their first homes. However, according to our 2024 Housing Market Report, only 51% of Canadians used the FHSA to save for their downpayment in 2023, suggesting that many Canadians still aren’t aware of the benefits of this powerful account. Before investing, here is what you should know about the Tax-Free First Home Savings Account.

What is the First Home Savings Account (FHSA)?

The First Home Savings Account (FHSA) allows Canadians to save up to $40,000 tax-free towards the cost of their first home. As well, contributions to the account will be able to grow and compound tax-free. In addition, this account can hold the same investments currently allowed with your TFSA, including:

- mutual funds

- publicly traded securities

- bonds

- Guaranteed Investment Certificates (GICs)

Of course, there are several limitations and rules in place. For example, any savings in your FHSA will have to be used by December 31 on the year of the account’s 15th anniversary OR when the account holder turns 71 — whichever comes first. In addition, if you do not use the whole amount, the account must be closed within one year of your first qualifying withdrawal.

If used properly, you will not be taxed on withdrawal. However, any withdrawals that do not meet the criteria of being used to purchase your first home will be taxed as income.

Who is Eligible for the FHSA?

As of right now, eligibility for this tax-free home savings account stands as follows:

- You must be a resident of Canada

- You must be the age of majority within your province or territory

- Aged 71 years or younger as of December 31st of the year you open your account

- You are considered a “first-time home buyer” and haven’t owned a home in the current calendar year or the previous four calendar years

- You did not live in a qualifying home that your spouse or common-law partner owned in the current calendar year or the previous four calendar years, or you did not have a spouse or common-law partner when opening the account

It’s also important to note that since this is a first-time home buyer’s account, the property you purchase must be a primary residence — not an investment property.

How Much Can I Contribute to the FHSA?

Account holders can contribute a maximum of $8,000 annually up to a lifetime limit of $40,000. If you cannot contribute the total $8,000, you can carry your unused contribution room forward to the following year.

You can also have more than one account, so long as the total of these combined accounts does not exceed the yearly or lifetime maximums. Contributions are tax-deductible and can grow and be withdrawn tax-free, assuming you follow the account rules.

Exceeding the Annual Contribution Limit

If you exceed your contribution room in your FHSA, you will be charged 1% per month on the excess amount until the excess amount is withdrawn. For example, if you contribute $10,000 in one year to your FHSA, the excess amount is $2,000. The tax payable is calculated by multiplying the excess amount of $2,000 by 1%, equaling $20. You will have to pay $20 per month until the excess amount is eliminated through any of the following ways:

- Making a designated withdrawal

- Directly transferring funds to a Registered Retirement Savings Plan (RRSP) or a Registered Retirement Income Fund (RRIF)

- Making a taxable withdrawal from the FHSA

Excess contributions can also be eliminated by reducing the amount of contribution room for the next year. For example, if you invest $10,000 in your FHSA in 2024 and do not eliminate the excess amount, your contribution room for 2025 will be $6,000. In addition, you will pay tax on the excess amount each month after you exceed the contribution room.

How Do I Use the First Home Savings Account to Buy a Home?

When you are ready to use your FHSA, you must first ensure that you meet the following conditions:

- You must be a first-time home buyer as per the criteria above

- You must reside in Canada when making the withdrawal

- The qualifying home must be located in Canada

- You must have a written agreement to either buy or build a home in Canada before October 1 of the year following the year of the initial withdrawal

- You must use the home as your primary residence

What if You Decide Not to Buy a Home?

Should you open a first home savings account and choose not to purchase a new home within the allotted timeline, you will have two options.

The first option is to transfer the money from your first home savings account to your Registered Retirement Savings Plan (RRSP) or Registered Retirement Income Fund (RRIF). This would be done tax-free.

The second option is to withdraw the funds. If you choose this route, the funds you withdraw will be taxed.

How to Open a FHSA

If you meet the requirements to open an FHSA, the first step is to find an FHSA issuer. Issuers include banks, credit unions, trusts or insurance companies.

Open your First Home Savings Account with Questrade online and start saving for your first home!

To open the account, you must provide your social insurance number (SIN), date of birth, and supporting documents to certify you qualify to open a first home savings account.

When you are filing your tax return for the year you opened your First Home Savings Account, you must fill out a Schedule 15 form, even if you did not contribute to the account in that year. Your FHSA issuer will provide you with a statement explaining how to report your contributions on your income tax return.

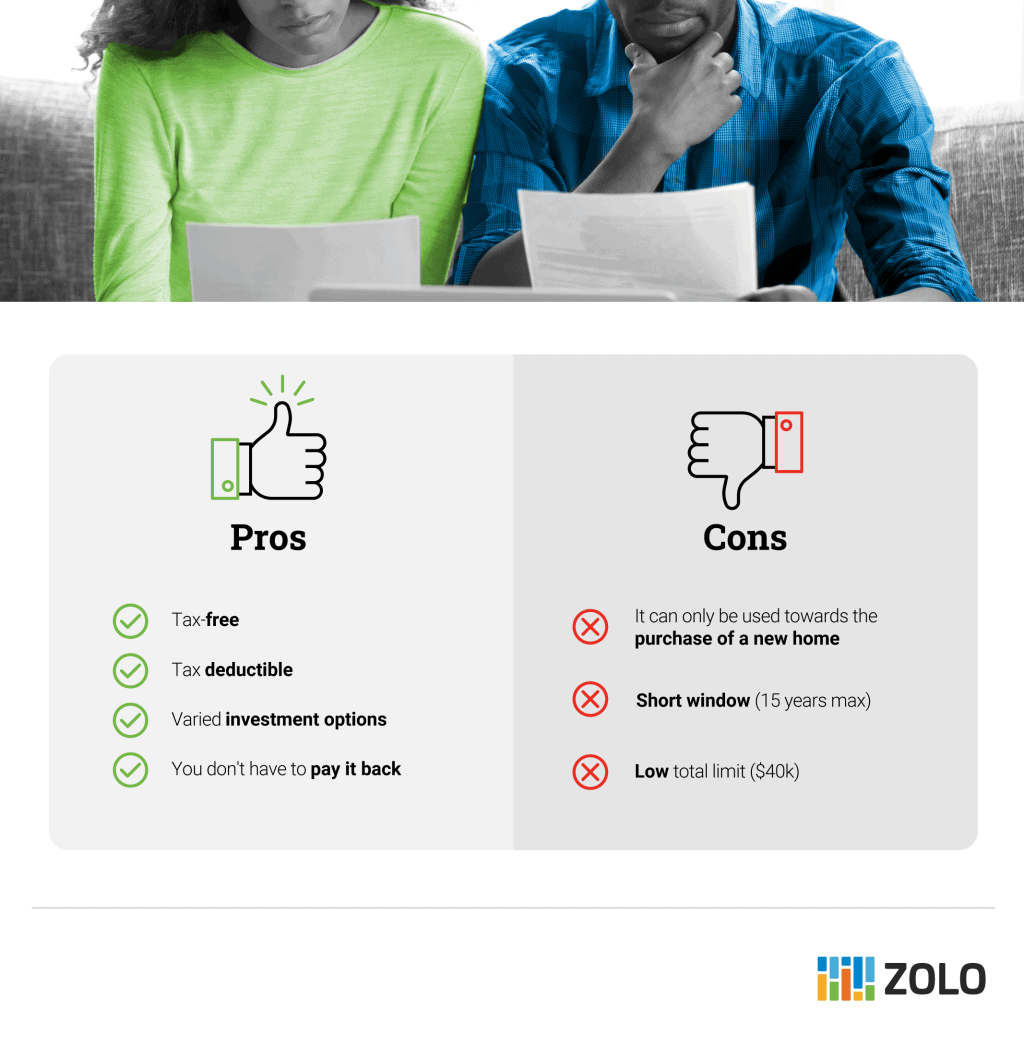

Pros and Cons of the Tax-Free First Home Savings Account

The FHSA is lauded as having the ‘best’ attributes of a Tax-Free Savings Account (TFSA) and RRSP. The main benefit is that the FHSA reduces your taxable income through deductions on your income tax return, and you are not taxed when you make a qualifying withdrawal. However, there are still pros and cons to consider.

Pros

- Tax-free

- Tax deductible

- Varied investment options

- You don’t have to pay it back

Cons

- It can only be used towards the purchase of your first home

- Short window (15 years max)

- Low lifetime contribution limit ($40k)

Is the Tax-Free First Home Savings Account Beneficial?

The tax-free home savings account can be a helpful tool for Canadians looking to save a home. The FHSA allows your money to grow tax-free. Plus, you’ll reduce your taxable income by claiming your contributions on your tax return.

Another great benefit is the money in your First Home Savings Account isn’t limited to a down payment. Your contributions can also be used for closing costs or other new-home expenses. Any unused funds in your FHSA can be transferred to an RRSP or RRIF to save for retirement without any tax implications.

What’s the Difference Between the FHSA and TFSA?

The main difference between the First Home Savings Account and the Tax-Free Savings Account is funds in an FHSA can only be withdrawn for a qualifying home purchase. Money in a TFSA can be withdrawn at any time, for any reason.

Secondly, any contributions to a TFSA are not tax-deductible, and you won’t pay tax on any withdrawals. Conversely, any funds contributed to your FHSA, within the contribution limits, are tax-deductible. Withdrawals are tax-free if you make a qualifying purchase of your first home from your FHSA.

Lastly, the contribution limits differ. The contribution limit for a First Home Savings Account is $8,000 per year, up to a lifetime limit of $40,000. For a Tax-Free Savings Account, the contribution limit is currently $7,000 per year, but your personal contribution limit may be higher, depending on how much you’ve contributed in the past.

Ultimately, if your goal is to buy a home, it’s smart to prioritize your First Home Savings Account. That being said, you should not neglect your RRSP or TFSA while saving to buy a home.

FAQs

Can I contribute to someone else’s FHSA (i.e., child or spouse)?

You can give your child or spouse cash to contribute to their FHSA. However, only the account holder can deduct any contributions made to their FHSA.

Can my spouse/partner and I both have an FHSA?

If you both meet the eligibility criteria, then yes. This will give you a maximum of $80,000 towards purchasing your new home rather than just $40,000.

Can I combine my FHSA with the Home Buyers Plan (HBP)?

Yes, you can use these financial tools in unison to purchase a home. In 2024, the Home Buyers Plan withdrawal limit was increased from $35,000 to $60,000 for withdrawals made after April 16th, 2024. However, if you use the HBP, you must repay the amount withdrawn from your RRSP within 15 years.