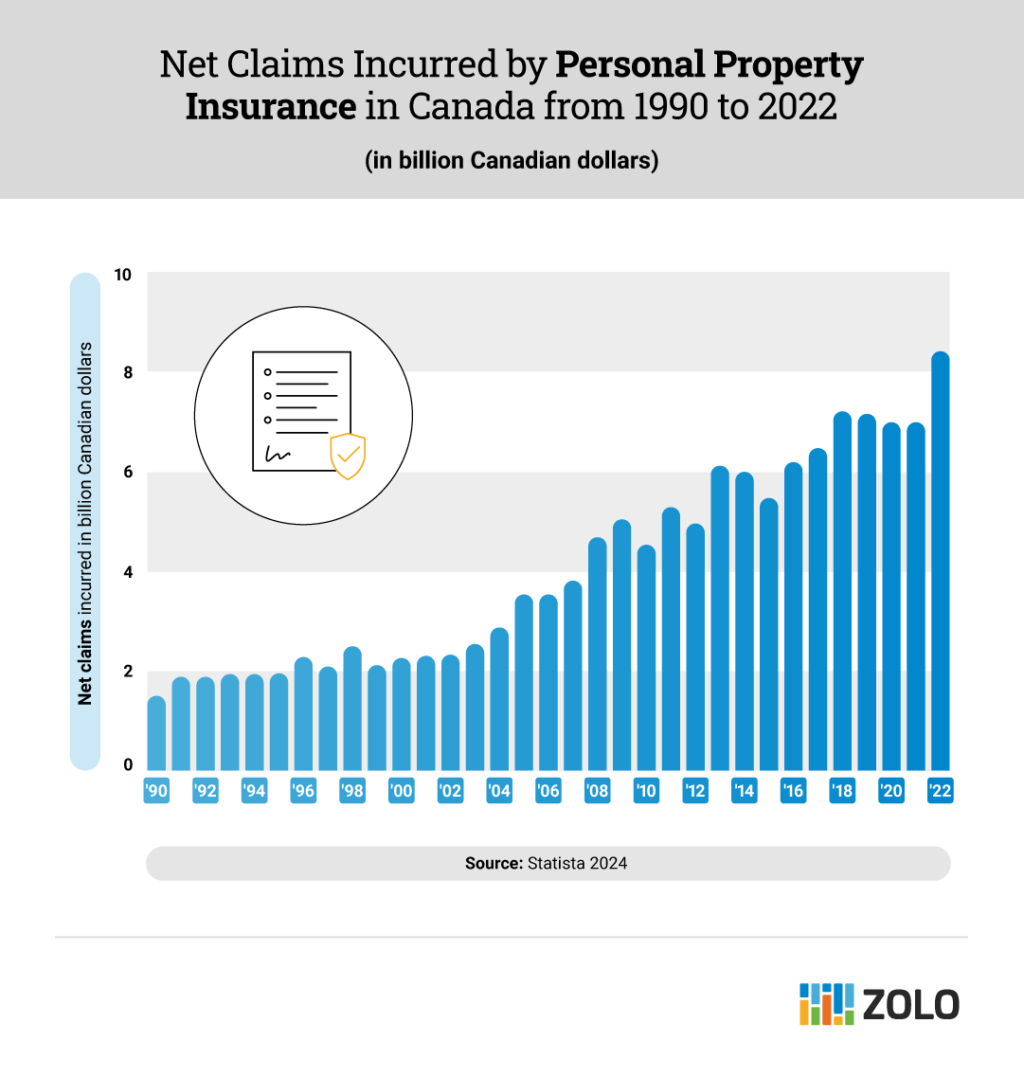

Having home insurance is a must to protect your most valuable asset, but few of us consider what happens when it comes time to use our coverage. Unfortunately, home insurance claims are on the rise. In 2022, net home insurance claims amounted to $8.5 billion in Canada, about $1.4 billion more than in 1990. A big cause of this increase is climate change and extreme weather events.

Whether you live in an area prone to the effects of climate change or not, it’s smart to understand the process of filing a home insurance claim. Missing steps can prolong the time it takes to process your claim, which could impact your ability to move forward with rebuilding or repairing your home. Here’s everything you need to know.

Key Takeaways

- Home insurance claims can be large, like a hail storm or minor, like your child accidentally throwing a baseball through the front window.

- In emergencies, call your provider after calling the appropriate authorities. Keep your policy information, including the emergency number, on hand to streamline this process.

- Collect all relevant information and document everything related to any damages or losses to your home or your personal property.

- In non-emergencies, review your deductible and policy coverage limits before initiating a claim to ensure it’s sensible to proceed.

Common Home Insurance Claims

You may file a home insurance claim for many different reasons. For example, home insurance would be needed to rebuild or repair your home after winter storm damage and also when your upstairs neighbour accidentally lets water leak into your unit, causing a flood.

Some common home insurance claims include:

Extreme Weather Conditions

Insurance claims caused by extreme weather have increased in Canada. According to a recent report from Statistics Canada, home insurance claims due to extreme weather reached $3.1 billion in 2023 and $3.4 billion in 2022. The report also stated that “once in 100 years” events occur more frequently, costing insurance companies billions. Some extreme weather events include extreme cold weather, hot temperatures, forest fires, flooding from heavy rainfall, hail, and hurricanes.

The report also cited research showing that approximately 10% of all Canadian homes, or 1.5 million, are highly exposed to flooding, Canada’s most extreme weather event.

Other Damages

There’s a variety of ways that your place can get damaged, with some of the most common home insurance claims being related to:

- Flooding

- Strong winds or hail

- Fire or smoke

- Burst pipes

- Plumbing issues

- Falling trees

- Damage to windows from flying objects (balls, etc.)

Loss Due to Your Home Being Burglarized

If your home or vehicle is burglarized, your first step is to document any damages and losses caused by the stolen items.

Your home insurance policy will also determine how you’re compensated for personal property losses. Some insurance policies will pay you the actual cash value, which is the depreciated amount of any damaged or stolen property due to a covered loss, while others will pay the replacement cost.

When to File a Home Insurance Claim

Knowing when to file a home insurance claim can be tricky because you don’t want to contact your insurer for every minor issue. Frequent claims can raise your insurance premium, so there is a balance between making claims and choosing to perform the repairs out of pocket.

You’ll want to file a home insurance claim in case of the following:

- The damages are much higher than your deductible. Since your premium will likely increase after filing a claim, you’ll want to ensure that the damages or losses are higher than your deductible, which is the amount you must pay out of pocket before your coverage kicks in. For example, if the damages are $1,200 to repair and your home insurance deductible is $1,000, perhaps you’ll pay for the repairs yourself to avoid an insurance premium increase.

- There’s an emergency. You’ll want to take immediate action if your home gets flooded or damaged due to a covered loss. Since you may have to evacuate your home, you’ll want to open up a home insurance claim so that you can have the cost of additional living expenses covered.

How to File a Home Insurance Claim Step-By-Step

Here are the steps to follow when filing a home insurance claim.

Step 1: Call Emergency Services and Document Everything

First, contact emergency services if there is an emergency, theft, or loss. If you live in a condo, contact your property’s management. Safety is the first priority, and you must ensure the property is safe for you and others.

Next, document the damages or losses to determine the extent of your claim. Here are some other tips for documenting everything for your home insurance claim:

- Take photos of any of the damaged or destroyed items in your home

- Keep all of the receipts from any cleanup

- Keep all damaged items unless they pose a health hazard

- Review your home inventory list

Step 2: Contact Your Insurance Company

Once you’ve gathered all of the information related to your claim and your insurance policy, you’ll want to start a home insurance claim by contacting your insurer. The home insurance claim process will depend on your specific insurer, but this usually leads to the next step.

Step 3: Begin the Home Insurance Claim Process

Once you contact your insurer, you’ll start working with your insurance adjuster or claims advisor, who will help you figure out how to proceed. This person will notify you within 48 hours of filing a claim to confirm the details of your loss. They may also arrange for any necessary emergency repairs and temporary living accommodations.

Your adjuster may ask for your condo management’s contact information and legal documents. If you had extensive damage to your personal property, you may be asked to fill out forms related to your losses. The home insurance claim process will depend on the circumstances.

Your adjuster will work with an approved contractor to gather details about an estimate of the damages and the required repairs. Many insurance companies have preferred vendors with whom they work. Finally, the repairs will begin, and once they’re completed, your home insurance claim will be closed.

What to Do After You File Your Claim

Once your claim has been filed, you’ll want to wait until you hear from a claims advisor or adjuster from the insurance provider. If you file a home insurance claim involving significant repairs to your property that make it inhabitable, the next step might be finding a safe place to stay as soon as possible.

The additional living expenses (ALE) aspect of your home insurance policy would pay for the expenses that you incur when you can’t stay in your place. ALE may include covering the stay at a hotel or Airbnb. Additional living expenses would also cover costs above everyday expenses caused by living outside of your residence due to an insured loss. Your coverage will depend on your policy limit, so you’ll want to keep this number in mind as you pick up expenses.

Once you have secured a safe place to stay, you can arrange repairs to your home. Insurance providers usually have agreements with specific contractors, but you can also hire your own. Research and get at least three quotes to find a reasonable price and a trustworthy company. Your insurance provider will verify the qualifications of your hired contractor and ask for proof of repairs through photos or an invoice.

The home insurance claim process can be time-consuming, so you’ll want to do your best to remain patient. If you live in a home and the damages are straightforward, you may simply wait for the contractor to begin the work. On the other hand, if you live in a condo, you may have to wait longer as you’ll need to deal with your insurer, the condo’s insurance company, and anyone else’s insurance.

Reasons Your Insurance Claim Could Be Denied

There are a few reasons that your insurance claim could be denied, and they typically include the following:

- You don’t have the correct coverage for the damage caused

- The person involved wasn’t covered

- Policy coverage limits

- The adjuster can’t assess the validity of the claim

- You’re deemed to be negligent for not keeping your home safe

The key takeaway is to stay informed of your policy and coverage limits to ensure enough protection for your situation.

FAQs About Home Insurance Claims

Is it worth claiming on home insurance?

It’s worth noting that, as of January, home insurance premiums increased by 7.66% annually, according to data from My Choice Financial. You’ll want to think twice about filing a home insurance claim that could raise your premium.

How to make a claim on house insurance?

The easiest way to file an insurance claim is to gather as much information as possible before making the report. You should always get an estimate of the damage before you call your insurance provider. Based on the likely cost, you can choose to use your home emergency fund, if you have one, or to file a home insurance claim. Be sure to also check your home policy for the deductible amount since there may be a different deductible for water damage than wind or hail damage.

What is the time limit for home insurance claims in Ontario?

You generally have anywhere from 90 days to 12 months from the date of the loss to file a claim.