Payday is one day of the week that typically brings forth some excitement. But, before you start spending all your money in one place, knowing how much to allocate to each of your financial goals is critical. In other words, you need to know how to budget.

What Is a Budget?

A budget is a plan for your money. It helps you understand where each dollar you earn should go, how much you have leftover to spend on fun stuff, and whether or not you’re living within your means.

It’s an effective tool for managing your money, ensuring all of your necessary expenses are taken care of so that you can focus on planning for the future and achieving your financial goals.

How Much Should You Budget for Each Expense?

A budget can help you map out how much you can afford to spend on each monthly expense. But, it can be hard to know whether your spending habits are in line with the ‘norm’ or whether or not there are some ways you can improve your financial situation.

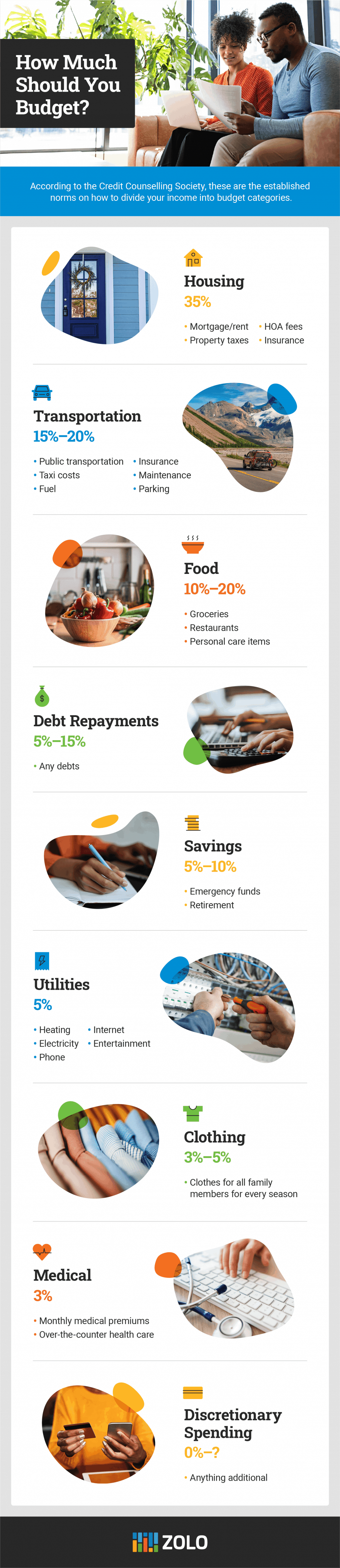

To help, here are some general guidelines from the Credit Counselling Society on what percentage of your income that experts recommend you spend on various sub-categories.

- Housing: 35%

This includes expenses like your mortgage or rent, property taxes, strata or condo fees, as well as insurance (home or tenant insurance). In more expensive cities, like Toronto and Vancouver, you can increase this budget item to a maximum of 42%.

- Transportation: 15% to 20%

Under this umbrella, you can include all transportation costs, such as public transit passes or tickets, taxi costs, fuel, insurance, maintenance, and parking.

- Food: 10% to 20%

This includes both groceries and personal care items.

- Debt Repayments: 5% to 15%

The more you owe, the tighter your budget will be. If you’re working towards getting out of debt, consider allocating a higher percentage of your monthly budget to paying it off.

- Savings: 5% to 10%

This should include emergency or contingency funds (for things like your furnace breaking down in winter) and savings for large future purchases and retirement. Some experts advise you to save closer to 20% if possible.

- Utilities: 5%

This includes heating, electricity, phone, internet, and entertainment expenses like cable, satellite, or streaming services.

- Clothing: 3% to 5%

This should include clothing for all members of the family for every season.

- Medical: 3%

This includes provincial or territorial monthly medical premiums (if applicable) and over-the-counter first aid or health care items and specialist fees.

- Discretionary Spending: 0% to ?

This is the money you have leftover after paying all of your additional expenses. You can spend this on whatever you like or add it to your savings.

Keeping these guidelines in mind, start listing your earnings and categorizing your expenses.

Determine Your Total Income

Before you spend a dime, it’s critical to confirm that you can afford to take on this expense. To do this, you need to subtract all your budget costs from your income and earnings. This may seem like a fundamental step, but you’d be surprised at how many people don’t even know how much they make or spend in a given month.

In a recent financial literacy study, 88% of Canadians said they understood the importance of a budget, yet less than a third (only 30%) actually stuck to their budget.

If your income fluctuates from month to month, it can help determine your average monthly income. This works best if you’ve got a few years of earnings to work with and if you’re not expecting any significant changes in the next three years or so. To calculate what you earn each month, total up the last three years of earnings, divide by three and then divide by 12 to get your monthly average. You can then use this number in your budget calculations.

Track and Categorize Your Expenses

See What You Spend

Tracking where your money goes gives you an accurate picture of your current spending habits.

Several helpful apps can help you track your expenses, like Mint and YNAB. Of course, if you prefer a more tangible method, a spreadsheet, taking photos of what you buy/spend on with your phone, or using an ordinary pencil and paper are excellent options to help you track your spending.

Categorize Every Expense

Take a close look at every credit card statement and bank account, and start grouping expenses into two broad categories: needs and wants. Needs are essential expenses like housing and food, and wants are discretionary costs like entertainment, meals, or hobbies. From there, you can determine where you can make any adjustments to cut back if needed.

Now that you know how much you’re spending on needs and wants, you’ll want to start drilling down in each category.

Tools to Help You Track and Categorize Your Expenses

To help budget your expenses, try out different tools to track your expenses and understand how much money is going towards each category. There are excellent apps and spreadsheets available depending on what style works best for you.

Phone Notes Expense Tracking Template

It can be helpful to track all your expenses in one easily accessible place. To help, we created a phone notes expense tracker. Simply download the PDF onto your phone. Then add the image to your notes app. As you make purchases throughout the month, track them in this template.

In this video, we walk you through the steps you can take to download the PDF and add the image to your notes for tracking. Tracking expenses can help you understand the emotional side of your spending habits and stay accountable for your finances.

To use your phone as a budget tool, download the Zolo Phone Expense Tracker template.

Compare, Cut, and Adjust

The next step is to compare what you earn to what you’re spending. Hopefully, you’re making more than you’re spending, but if not, you’ll need to take a close look at your expenses and decide where you can reduce spending.

You should also make sure your expenditures aren’t straying too far from the guidelines listed above. Everyone’s financial situation is slightly different, so don’t worry if your budget doesn’t align right down to the percent. Still, you should be aware of any expenses that stretch your budget beyond expert recommendations.

Like any healthy habit, sticking to a balanced budget takes a little practice and dedication. But this effort can, quite literally, pay off when it comes to better financial health.

Shift Your Mindset

While expense tracking can lead to a deeper understanding of where your money is going, it can also be stressful. To get you in the right mindset, we have money mantras to try using. Mantras are phrases that you can repeat to help you focus on a goal.

Take a moment to pinpoint what your money goal is. Write it down on a piece of paper and put it in a place where you frequent. You can tape your money mantra to the fridge or hang it on your desk. This will become a positive reminder of what you’re working towards.

Not sure what your money mantra should be? We have some printable money mantra cards for you to try. Download the cards and choose one that resonates with you and your goals.

Download your own version of Zolo’s money mantra printables

Leave Time for Reflection

As Albert Einstein allegedly said, “The definition of insanity is doing the same thing over and over again and expecting a different result.” Budgeting can help you track down areas of your financial spending that need improvement, but you’ll be left in the same spending cycle unless you make a change.

To help you reflect on the outcome of your expense tracking, we have a spending reflection worksheet. Take the time each month to analyze where your money is going and readjust your goals based on the trends you’re seeing.

Download spending reflection worksheet

With these resources, you’ll be well on your way to financial stability. For more information on how to prepare your finances for the future, check out the Zolo Blog.