Canadian first-time homebuyers are often instructed to budget for closing costs when buying a home, but what are closing costs, and how do you know how much cash you’ll need to close?

While there are general rules of thumb for how much to save for closing fees, ultimately, the cost depends on the particular house you are purchasing, the location of your future home, and even who you choose as your real estate lawyer.

Once you understand the different types of closing costs, you’ll be well on your way to getting the keys to your new home.

Key Takeaways

- Closing costs are upfront fees paid on the closing date

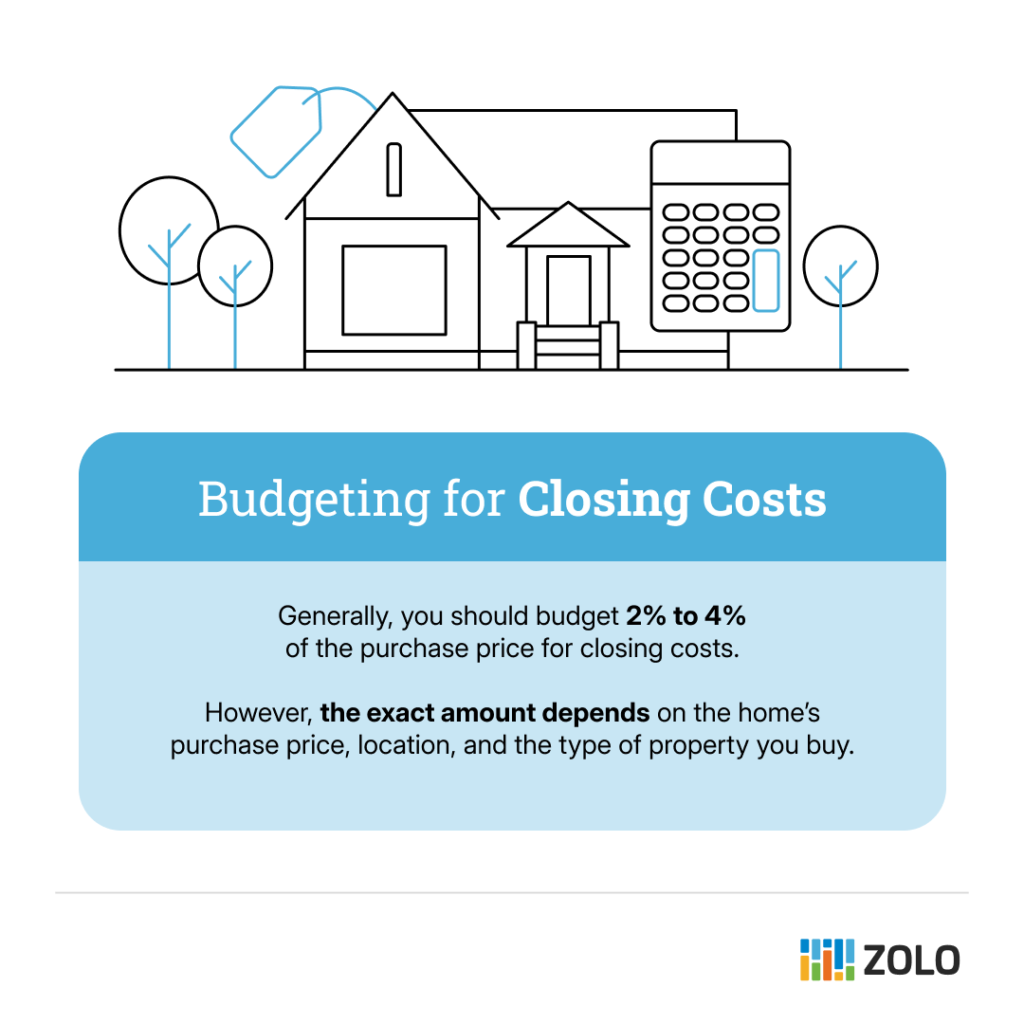

- It’s smart to budget 2% to 4% of the purchase price for closing costs

- The buyer pays the majority of closing costs, which may include legal fees, land transfer taxes, title insurance, and other administrative fees

What are Closing Costs?

Closing costs are upfront legal, administrative fees, and taxes associated with a real estate transaction. Closing costs are a separate expense that is not included in your down payment. Additionally, closing costs cannot be rolled into your mortgage payments and must be paid upfront on the closing date.

How Much Are Closing Costs?

The exact amount you’ll pay in closing costs varies significantly, depending on the home’s purchase price, where you live, the real estate lawyer you choose, and the type of property you buy.

The general rule of thumb is to budget 2% to 4% of the purchase price for closing costs. For example, if you plan to buy a home for $600,000, you should budget $12,000 to $24,000 for closing costs.

Breakdown of Common Closing Costs in Canada

To better budget for closing costs, here are some common types of closing fees and their associated costs. Some types of closing costs are mandatory, but others may not apply to you, depending on the type of property you are buying.

Legal Fees

A real estate lawyer completes the paperwork associated with buying and selling a home. For example, your lawyer will review the purchase agreement, perform a title search, calculate the land transfer tax, arrange for title insurance, and oversee the financial transaction to ensure all funds are properly distributed between the parties involved.

In addition, you will incur administrative costs associated with courier services, scanning, and printing documents. These legal and administrative fees can range from $900 to $2,000, depending on where you live.

Registration Fees

Your real estate lawyer pays title and mortgage registration fees on your behalf. The specific fees vary by province.

For example, in Ontario, you may have to pay:

- Registration of Deed Transfer: $82.00

- Registration of Mortgage: $82.00

- Municipal Land Transfer Tax Processing Fee: $89.84

Land Transfer Tax

Land transfer tax (also known as property transfer tax in some regions) or an equivalent is applied when you buy a home in most Canadian provinces. The amount of land transfer tax is typically calculated as a percentage of the property’s selling price.

Each province sets its own marginal land transfer tax rates, and some municipalities set separate land transfer fees. However, you may be eligible for a land transfer tax rebate if you are a first-time homebuyer. For example, in Ontario, the marginal land transfer tax rate is:

Moreover, Toronto charges an additional municipal land transfer tax, which doubles the amount you pay.

Home Appraisal

A home appraisal is an unbiased assessment of a property’s fair market value. Your mortgage lender may require an appraisal before approving your mortgage application to ensure the home is worth the offer you made. A property appraisal fee typically ranges between $300 and $500.

Property Survey

In addition to the home appraisal, your mortgage lender may require a property survey if the seller’s survey is outdated. Depending on the size and complexity of the property, the survey fee could range from $1,500 to $6,000.

Home Inspection

While not mandatory, it’s a smart decision to hire a professional home inspector. A home inspector can help identify hidden problems or systems that require repair or replacement. If significant issues are found, you may be able to negotiate a price reduction to cover the repair costs or have the seller complete the repairs prior to closing.

Unlike other closing costs, the home inspection fee is paid directly to the home inspector and could range between $500 and $600.

Title Insurance

Title insurance protects your lender against title fraud or outstanding claims on the property. The fee for title insurance could range between $250 and $500 depending on where you live, the value of the home, and the insurance provider.

Property Tax Adjustments

If the sellers have prepaid property taxes for the year, you will pay a pro-rated portion of the property taxes at closing. The property tax you will pay depends on the date you purchase the home, the property’s value, and the municipal tax rates.

Mortgage Interest Adjustment

You may need to pay a mortgage interest adjustment if there is a gap between your mortgage closing date and your first mortgage payment date. For example, if you close on a home on April 15th and your first mortgage payment is due on May 1st, you will accrue interest for 16 days. Most commonly, your lender will add the interest adjustment to your first mortgage payment. However, you may pay it as part of your closing costs.

CMHC Mortgage Insurance

CMHC mortgage insurance, also known as mortgage loan insurance or mortgage default insurance, is mandatory for buyers with a down payment of less than 20% of the home’s purchase price. This insurance protects your mortgage lender in the event that you default on your payments.

CMHC premiums are calculated depending on the size of your down payment. The larger your down payment, the less mortgage insurance you will need to pay.

You can pay for mortgage default insurance upfront. However, many add it to their mortgage, resulting in a higher mortgage cost over time.

In addition, Saskatchewan, Manitoba, Ontario, and Quebec add Provincial Sales Tax (PST) on the mortgage insurance premium, which is paid as a lump sum upon closing.

GST/HST on New Homes

Federal sales tax may be applied if you buy or build a new construction home or condo. The rate you pay depends on which province you live in. For example, in Ontario, the HST rate is 13%, whereas in British Columbia, the GST rate is 5%. Your builder may include sales tax in the total purchase price, which is rolled into your mortgage. On the other hand, if sales tax is not included, it becomes part of your closing costs.

However, you may be able to claim the GST/HST new housing rebate on your personal income tax return if the property is your primary residence.

Condo Estoppel Certificate Fee

You are required to pay for an estoppel certificate when buying a condo in Canada. This certificate is a contract between the condo owner and the condo corporation, which includes the details on how and when to pay condo fees, any unpaid fees by the seller, and any litigation between the seller and the condo association.

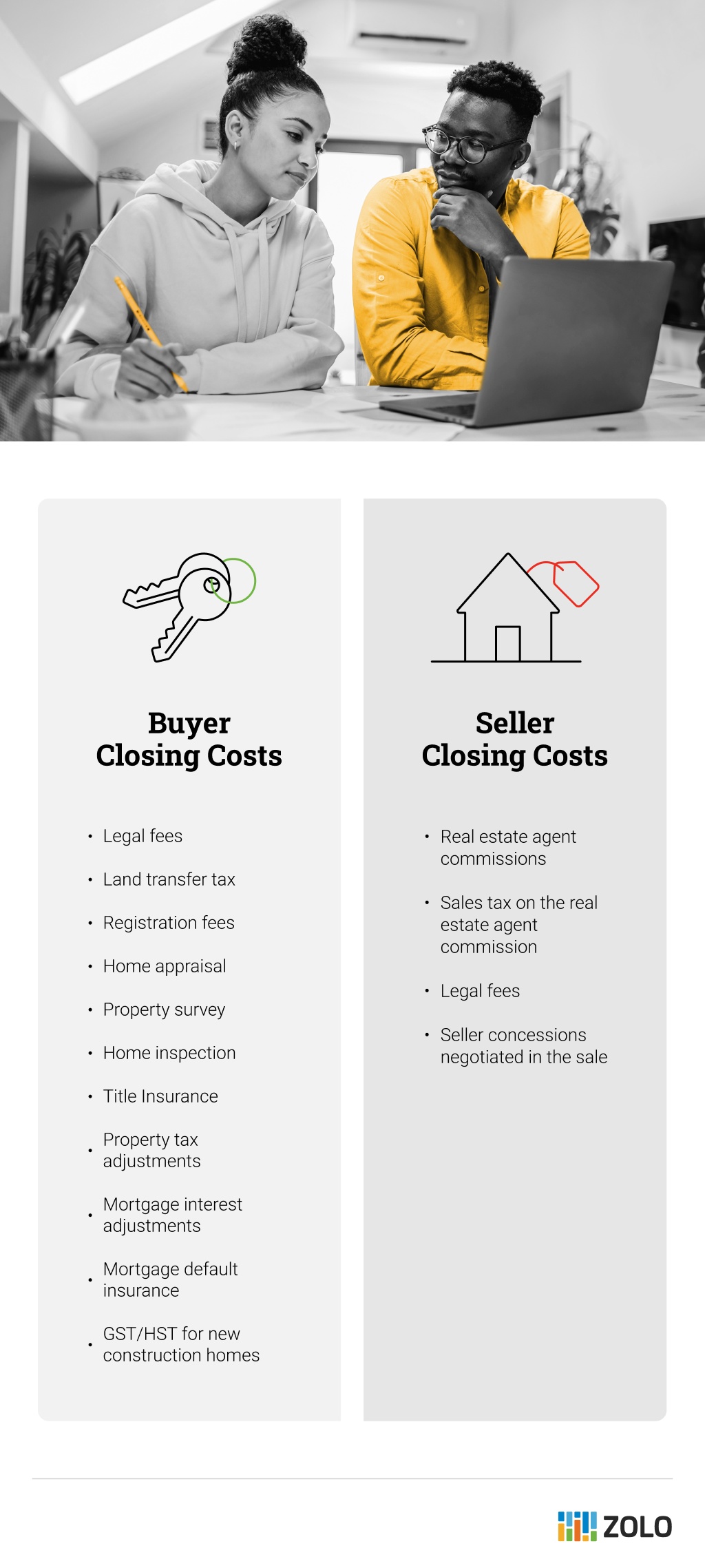

Who Pays Closing Costs?

In Canada, the buyer pays for the majority of closing costs. However, the seller will also incur some closing costs related to the real estate transaction.

Closing Costs for Buyer

The majority of the closing costs outlined above are paid by the homebuyer. Closing costs and down payment will be paid to your lawyer as part of the closing process. Additionally, you will need to consider moving costs when buying a home.

Closing Costs for Seller

Selling a home involves several fees, which vary depending on where you live and your agent’s commission structure.

Real estate agent commissions

The commission is the fee you pay your agent for their services. In Canada, the seller typically pays the commission for both the buyer and seller’s agents. The commission is deducted from your proceeds from the sale.

There is no set rate for real estate commissions. However, it typically ranges from 3% to 7% of the purchase price. Moreover, the amount you pay is up for negotiation with your agent.

Sales tax

In addition to the real estate commission, the seller is responsible for paying sales tax on the commission. The GST/HST tax rate depends on your province or territory.

Legal fees

Lawyers facilitate the real estate transaction from the seller to the buyer. Legal fees generally range between $1,000 and $1,600. As the seller, your lawyer will:

- Review the sale agreement and assist with negotiations of the terms and conditions

- Perform a title search to ensure that any outstanding permits have been closed

- Ensure all legal and financial requirements have been met

- Facilitate closing by confirming receipt of funds from the buyer, paying off the existing mortgage, advancing the final balance to you as the seller, and releasing the keys to the buyer’s lawyer

How to Save on Closing Costs as a Buyer

There are several ways for you to save on closing costs. Including:

- Shop around – Compare legal fee rates before choosing a real estate lawyer

- Rebates – You may be eligible for first-time homebuyer rebates or forgivable loans

- Seller concessions – You can negotiate with the seller to have them partly cover closing costs

- Reduce your down payment – If you’ve saved more than the minimum down payment amount, you can use extra funds to pay for your closing costs

Bottom Line

Managing closing costs is a crucial part of the homebuying process, and being prepared can make a huge difference in your overall experience. Consider using a closing costs calculator to help you budget for closing.

Search for your next home on Zolo.ca, or use our free home valuation calculator to see how much your home could sell for.

Closing Costs FAQs

What is the formula for calculating closing costs?

Generally, you can expect to pay 2% to 4% of the purchase price in closing costs. To calculate your closing cost estimate, multiply the purchase price by 0.02 and 0.04.

For example:

$600,000 x 0.02 = $12,000

$600,000 x 0.04 = $24,000

For a $600,000 home, you should budget between $12,000 and $24,000 for closing costs.

Can you negotiate closing costs?

Yes, you can request that the seller pay all or a percentage of the closing costs. These seller concessions are negotiated as part of the purchase agreement. The concession can be arranged as a percentage of the purchase price or a fixed dollar amount. Seller concessions are more common in a buyer’s market.

What if I can’t afford closing costs?

If you can’t afford closing costs, you have a few options to reduce them. Before choosing a real estate attorney, compare legal fee rates. Additionally, search for first-time homebuyer rebates or forgivable loans to help cover closing costs. Lastly, you can also negotiate with the seller to have them cover part of the closing costs.