Almost everyone will agree that there is a basic formula for wealth management and asset accumulation: make more than you spend, reduce expenses, and invest your savings wisely.

For homeowners, the idea of wealth management, never mind nest egg building, usually takes a backseat to other financial priorities like maintaining your home and paying off the mortgage debt.

It doesn’t have to be this way.

While building wealth may seem impossible — particularly for new homeowners or first-time buyers trying to get into the market — the concepts and steps to wealth building are simple and easy to implement. The great news is you don’t have to earn a six-figure salary to build wealth successfully. No matter what you make or how old you are, you can amass wealth as long as you’re determined.

What Is Wealth Accumulation?

When we talk about wealth, we are usually referring to the pure, finance geek speak definition of wealth:

Wealth = (Total market value of all tangible + Intangible assets) – debts

Put another way, you can calculate your wealth by subtracting your liabilities from your assets.

Your Nest Egg = (All tangible assets + All intangible assets) – (debts + accumulated depreciation)

For many, the goal is to become wealthy enough to live free from obligation or dependence by growing a large enough nest egg to support us. To achieve this goal, most of us focus on wealth accumulation.

Why Is Wealth Accumulation Important?

In my new book, House Poor No More: 9 Steps that Grow the Value of Your Home and Net Worth, I discuss the importance of goal-setting and planning — and show how this translates into a successful wealth accumulation strategy.

But to appreciate the importance of planning, we need to go as far back as the 1960s. This decade saw a wave of studies published on the importance of goal-setting as it relates to successfully meeting a goal. (The first empirical study on goal-setting was published in the UK in 1935 by Cecil Alex Mace.) For example, one article published in the Journal of Applied Psychology in 1967 showed how setting specific goals increases motivation, which increased the achievement of those goals by as much as 30%. While the idea that setting tangible goals improves your chances of reaching them may seem self-evident now, it was ground-breaking at the time, and changed how financial advisors helped their clients reach their goals.

Not surprisingly, many financial planners and money coaches now insist on a financial plan — a tangible goal-setting document that helps you visualize and specify your financial goals.

By identifying your financial goals, you can determine the steps required to meet them. This roadmap will be tailored to your unique goals, and no two roadmaps will be the same. For instance, if your goal is to retire early, your actions may differ from someone who wants to reach a certain professional standard, buy a car, or start a family.

So how does homeownership fall into goal-setting and wealth accumulation?

For starters, owning a home is a goal all by itself. Saving up a down payment, shopping for the right (at least for now) home and maintaining a property once you’ve bought it are all monumental undertakings all on their own. But owning a home isn’t the final destination or the ultimate goal. Financial independence through wealth accumulation is the goal, and reach that goal, you need to use your home as a part of your wealth accumulation strategy.

Today, we’re faced with volatile equity markets and high-priced homes, and building wealth may seem impossible – but it’s not. The truth is there is plenty of evidence that even those earning less than six figures can grow their net worth and achieve financial independence. No matter how old you are, how late (or early) you start, and how much you earn, you can amass wealth as long as you’re determined and set the right goals. Just remember that building wealth is not an overnight process.

Start With a Financial Plan

Your financial plan is your blueprint for your financial goals, whatever they are. If your goals include wealth accumulation, you’ll need your blueprint to include a strategy that minimizes (or eliminates) debt and maximizes your assets over time. The main way to measure the progress of your wealth accumulation plan is by growing your net worth. The bigger your net worth, the more independence you have regarding lifestyle and financial decisions.

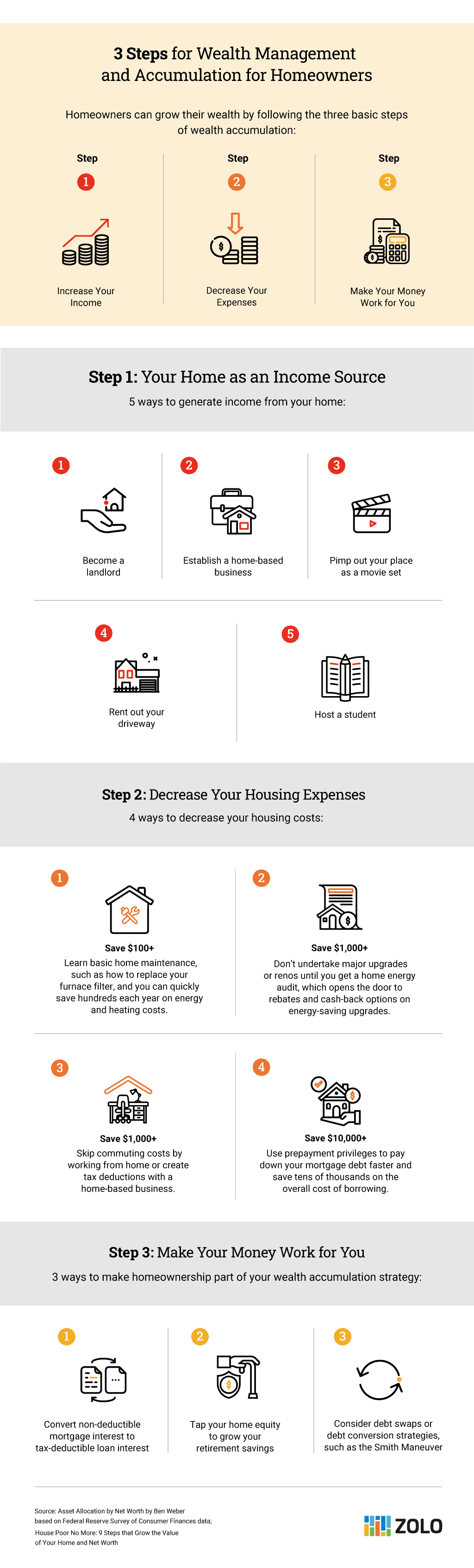

In general, there are three components to any wealth management and accumulation plan:

- Increase your income

- Decrease your expenses

- Make your money work for you

How to Use Your Home in Your Wealth Accumulation Strategy

When you put the three components above into action, you’ll grow your assets and pay off debt. Implementing these three components is particularly important for first-time buyers just starting their wealth-building journey or for homeowners who have never tapped their home as a wealth accumulation tool.

To start, take these three steps:

Step 1: Increase Your Income

Part of your wealth accumulation strategy should be dedicated to increasing your income. While many of us will achieve this through annual salary increases, opening up a business or taking on side-hustles, if you are a homeowner, your home itself could represent an additional income stream.

Here are five ways to generate income from your home:

- Become a landlord: Whether it’s a secondary rental suite with a long-term tenant, a room you rent out or a short-term rental unit, renting out excess space in your home is a smart way to increase your income.

- Establish a home-based business: Not only do you add an income stream, but you also create tax deductions that you can use to reduce your taxes.

- Pimp out your place as a movie set: If you live in a larger city or have a unique home, consider listing your property as a potential movie set. Location scouts are always looking for the ideal spot. You never know, the fame your home garners from starring in a movie could even make it a sought-after getaway spot, like the cottage used for a certain leading man’s send-off in Avengers: Endgame, now renting for a whooping $800 USD per night.

- Rent out your driveway: If you live close to a busy commercial centre, medical or entertainment facility such as a hospital or stadium, consider renting out your parking spots. You can either do this on a part-time/per-event basis or as an ongoing income generator. Nancy Gillis, a retired teacher who lives close to B.C. Children’s Hospital in Vancouver, BC, generated an extra $400 per month by renting out two parking spots on her driveway to medical professionals. To advertise, you can put up notices on free classified ad websites, such as Kijiji or Craigslist, or plaster paper ads near the facility.

- Host a student: This income stream (also known as homestays) can generate $500 to $1,000 per month in extra cash. That said, you are required to spend quality time with the student and provide a separate bedroom along with three meals per day.

Step 2: Decrease Your Expenses

In House Poor No More, there are more than 35 tips that illustrate how homeowners can save more than $6,000 per year through efficient upgrades, new habits and rebates. Many of the suggestions are free and only take time and effort — although some options will cost you.

One of the best ways to decrease your home’s expenses is to decrease your variable costs. Variable costs are costs related to your consumption of resources, for example, water, fuel, and electricity. You have control over these costs, but can’t control or reduce others, for example, property taxes.

Fortunately, there are a ton of ways to reduce your variable costs, with the added benefit that you can usually make your home more eco-friendly in the process. For example, if you want to reduce the amount of money you spend on heating and cooling, a great place to start is replacing your windows and doors and upgrading your insulation.

If you want to upgrade your home’s efficiency, but you aren’t sure where to start, a home energy audit is a good first step. A home energy audit is an assessment done by an independently certified evaluator. The assessment shows how efficiently your home uses energy and, more importantly, where energy is being wasted. Once the energy audit is complete, you’ll receive a detailed report that lists your home’s energy deficiencies as well as tangible recommendations for fixing these issues to make your home more energy-efficient.

Home energy audits cost anywhere from $100 to $800 for a typical home. The range in price depends on your city, the specifics of your home and the firm that completes the audit. The good news is that many provinces now offer financial incentives for these audits, including rebates on the audit cost, provided you finish a portion of the updates suggested in the report.

For example, in Ontario, homeowners pay $0 for their home energy audit after completing all energy upgrade suggestions and filing for a rebate.

There’s another reason why a home energy audit makes sense: It will open the door to even more rebates and savings on efficiency upgrades. In Ontario, homeowners can claim up to $5,000 in green home upgrade rebates. In BC, homeowners get up to $7,000 back in rebates for upgrades ranging from new insulation to air source heat pumps. There are also federal programs for offering rebates on energy-efficient home upgrades.

The process of getting a home energy audit might seem daunting, so we’ve broken down the process for you step-by-step below, so you know what to expect:

- Don’t undertake significant home renos, especially in an older home, without considering or paying for a home energy audit. You could be leaving thousands of dollars in rebates unclaimed.

- When you book your home energy audit, prepare by gathering the last 12 months of utility bills. Your auditor will want to see these.

- After the audit, review the list of suggestions in the audit and determine which ones align with your remodel plans.

- Once you complete the reno, schedule your final audit test, where the company returns and retests your home to gauge the impact of the energy-efficient improvements.

- Receive your final report that shows your home’s energy efficiency improvement.

- Submit receipts and paperwork to various federal, provincial and municipal rebate programs. Although it can take up to a year to get the rebate money, it should still feel pretty good to get money back on renovations you were going to do anyway.

Step 3: Make Your Money Work for You

On the surface, owning a home may seem like a financial liability. It takes money out of your pocket every month, and in almost every situation, you’ll spend more of your after-tax dollars on housing as a homeowner than you do as a renter.

To offset this cost, homeowners need to get smart about spending, especially when it comes to home renovations. This is where the difference between your home being an asset, versus it being an investment, is particularly important. Remember, an investment is a decision to use money to earn more money. An excellent example of a home being an investment is purchasing an income property that will generate positive cash flow each month. In that case, you’re using your money to generate more money.

Most primary residences are not investments. They are assets. That means they have value, but the money you put into maintaining your home doesn’t necessarily translate into an increase in the home’s value. For example, you may spend thousands of dollars maintaining your home each year, but those dollars spent don’t directly translate into an increase in the home’s value.

The same is true for renovations. Although your home certainly has value, that doesn’t mean spending on renovations for your home will increase the value of that investment. If your decision to renovate is predicated on the value it will add to your home, then make sure you can back this assertion up with expert insight and data — and be prepared to be wrong.

Why does this matter? Because buying a home usually means taking on debt – usually the biggest debt you’ve ever had — and you should only take this step if you have a debt management plan as part of your overall financial strategy.

Still, when it comes to making your money work for you it’s critical to consider how best to use all your assets — including your earnings, investments and your home — as part of your debt management and wealth accumulation strategy.

Dealing With Mortgage Debt as Part of Your Debt Management Plan

Canadians pay, on average, 23.2% of their earnings in taxes — slightly less than the 24.8% net average of all OECD countries (member-states with a commitment to democracy and the market economy). Still, when almost a quarter of your income is paid in taxes, it doesn’t hurt to find ways to max out legitimate tax deductions to lower your overall tax bill each year.

While many tax deductions are simple to figure out and apply — from student loan interest to childcare expenses to charitable donations — some opportunities aren’t as straightforward. One, in particular, is how and when you can deduct mortgage interest as a tax-deductible expense in Canada.

Is Mortgage Interest Tax-Deductible in Canada?

In general, if a mortgage is held on a property used primarily to generate income, the mortgage interest is tax-deductible.

Tax-deductible interest means any mortgage interest paid on a property used to generate rental income can be claimed as a tax-deductible expense in Canada. Using the property to generate income could include professional income (such as a dental office) or business income (such as a retail store).

Unfortunately, this straightforward option is not open to homeowners who pay mortgage interest on their principal residence. The good news is some strategies can turn this non-deductible mortgage interest into a tax-deductible expense.

How to Make Your Canadian Mortgage Interest Tax-Deductible

Since Canadians cannot write off the mortgage interest on our personal residences like in America, it’s critical to learn how to create a tax-deductible Canadian mortgage.

The principle behind this strategy was first introduced by Fraser Smith, a well-known B.C.-based (now-retired) financial planner who wrote a book outlining his strategy. Known as the Smith Maneuver, the underlying principle is to pay off all non-deductible debt using current savings, then re-borrow and use this debt to invest.

For example:

- Say you hold $390,000 in invested savings (let’s assume you and your partner hold this sum in a non-registered investment account) and owe $390,000 on a mortgage on your home;

- Cash-out your invested savings and use the money to pay off your mortgage;

- Then re-borrow the $390,000 and re-purchase your investments (be sure not to use the borrowed money to purchase investments inside a registered account as this will negate the tax-deductible status of the borrowed funds);

- What you owe and what you hold as assets have not changed; however, the more than $11,000 you paid in non-deductible mortgage interest is now a tax-deductible expense.

Using Home Equity to Build Wealth

Another way of getting your money work for you, by using your home to build wealth, is to tap your home equity.

Home equity is the difference between your home’s fair market value and the outstanding balance of all debts on the property, such as mortgages or lines of credit.

Just like the debt swap that turns a non-tax deductible mortgage on a principal residence into a tax-deductible loan, you can use the equity in your to boost your retirement funds or jump-start your investment savings.

To use this strategy, you need to set up a debt conversion strategy using a readvanceable mortgage — a mortgage loan that’s attached to a home equity line of credit, also known as a HELOC.

Each time you make a mortgage payment, the portion used to pay off the principal debt frees up the same amount in the line of credit, which is then borrowed and used to purchase income-producing investments.

Here’s how it works:

- Make your regular monthly mortgage payment of $2,500, where $1,250 is used to pay interest, and the other $1,250 is used to pay down the principal loan debt

- Once the transaction is completed you, have $1,250 available to borrow from the readvanceable line of credit.

- Borrow this $1,250 and invest in a portfolio of income-producing assets (or assets you believe will appreciate over time).

Just like the debt-swap that creates a tax-deductible mortgage in Canada, this debt conversion strategy creates a tax-deductible investment loan that you can use to boost your retirement nest egg.

Homeowners late to the retirement savings party can kickstart their savings by maxing out the amount borrowed against their home equity and using the funds as a lump payment towards an investment portfolio. Remember, the interest paid on the HELOC is a tax deduction, as long as the money is only used for investment purposes.

Aside from the gold-standard debt swap, known as the Smith Maneuver, and the simple debt conversion, there are three other methods of swapping non-deductible mortgages for tax-deductible debt, all of which are outlined in House Poor No More.

But remember, you can get into serious trouble with any of these strategies if you skip out on the overall intent, which is to strategically pay off all debt and minimize your overall cost of borrowing.

Final Thoughts

In my book, you’ll find strategies for maintaining, protecting and increasing the value of your home while finding small and big ways to save money. For now, however, every homeowner or potential first-time buyer can use the following steps to create a wealth accumulation strategy using your home.

By using the steps of increasing your income, reducing your expenses, and leveraging your equity, you will develop a smart strategy for buying, maintaining and growing the value of your home – the single largest asset you own.