Saving for the down payment is one of the biggest hurdles most Canadians face when buying a home. If you’ve been contributing diligently to your Registered Retirement Savings Plan (RRSP), it can be tempting to withdraw that money to buy a home.

But, many of us have heard from financial experts that we shouldn’t touch our retirement nest egg. Still, the Home Buyers’ Plan (HBP) offers the option to withdraw from your RRSP for a down payment on your first home. With 41% of Canadians saving their down payment in an RRSP in 2023, the HBP is a popular choice. But is it the right choice for you? Let’s explore the rules for using your RRSP for a down payment.

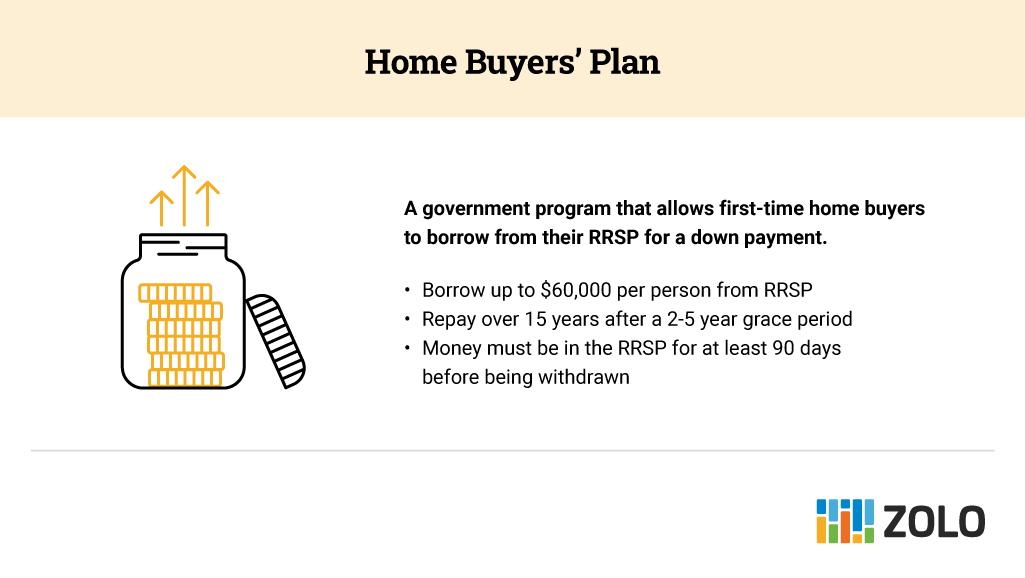

What is the RRSP Home Buyers’ Plan (HBP)?

Currently, the HBP allows first-time homebuyers to withdraw up to $60,000 from their RRSP savings to purchase or build a home without paying tax on that withdrawal. A couple can withdraw up to $60,000 each, for a total of $120,000 to buy a house. So long as they each qualify as a first-time homebuyer, of course.

The loan is considered tax-free, and you have 15 years to pay back the total amount. But now that you’re ready to enter the real estate market, how do you use your RRSP for that down payment? Let’s start with the basics.

Who Qualifies For the Home Buyers’ Plan?

The qualifications to be eligible for the Home Buyers’ Plan are pretty simple:

- You must be a first-time homebuyer who is a resident of Canada

- You must have a document stating that you are buying or building a home for your personal use in the same calendar year that you withdraw your RRSP money (under the HBP)

- Alternatively, you can participate in the HBP if you are buying or building a home for a specified disabled person, even if you or they are not a first-time homebuyer

A first-time homebuyer is someone who has not owned a property in the previous four calendar years and has not occupied a home that their spouse or common-law partner owns in the last four calendar years.

For those who qualify for the HBP, there are a few rules to follow. First, if you plan on building a home, the property must be completed and suitable to be lived in before October 1st, one year after you withdraw your RRSP funds under the HBP. If the property is not ready by that date, you may cancel the HBP or choose to buy or build a different home.

You can participate in the Home Buyers’ Plan more than once, provided your HBP repayment balance is zero, and you meet all other HBP eligibility requirements.

How Do You Withdraw From Your RRSP Under the HBP?

After ensuring you are eligible to participate in the Home Buyers’ Plan, the next step is to withdraw the funds.

First, you must have a written agreement to buy or build a qualifying home at the time of your withdrawal. Any funds you wish to withdraw must have been in your RRSP account for at least 90 days.

Next, you must fill out Form T103, Home Buyers’ Plan (HBP) Request to Withdraw Funds from an RRSP. The best option is to book an appointment with the financial advisor where you hold your RRSP. From there, they should be able to provide you with the form and the next-step instructions on how to complete this process.

After you submit your request, it may take a few days or several weeks to process your application and deposit the money into your account.

On closing day, you’ll use those funds to pay your down payment. Additionally, you can request to withdraw funds under the HBP up to 30 days after your closing date.

Repaying The Withdrawn Funds

Under the Home Buyers’ Plan, you need to repay any amount withdrawn from your RRSP within 15 years. Typically, the repayment starts the second year after your first withdrawal. For example, if you withdrew in 2020, your first year of repayment was 2022.

However, if you participate in the HBP between January 1st, 2022 and December 31st, 2025, the repayment period can be deferred an additional three years. For instance, if you withdraw in 2025, your first repayment will be due in 2030.

To make a repayment, you will need to contribute to your RRSP and designate the repayment on your income tax return. Each year, the Canada Revenue Agency (CRA) will send you a statement of account that includes the amount you have to contribute as repayment and your HBP balance.

You can repay the full amount at any time.

What Are the Advantages and Disadvantages of Using Your RRSP?

Why do so many financial advisors suggest not using your RRSP savings as part of your home’s down payment? Unfortunately, this incredible program has downsides.

We recommend examining the pros and cons to help you determine whether the Home Buyers’ Plan is a good option. The list considers the advantages and disadvantages of using money saved in your RRSP as part of your down payment.

The Advantages:

- You’ve already saved this money, possibly allowing you to buy a home sooner

- The funds can be used stand-alone or added to savings to bump up your down payment

- The withdrawal is tax-free and interest-free as long as you repay according to schedule

- After a grace period, you will have 15 years to repay the loan

The Disadvantages:

- You cannot withdraw any RRSP money until it’s been in your registered account for at least 90 days

- You potentially miss out on 15 years of tax-sheltered growth (think compound interest) on the money you withdraw

- If you neglect to pay the annual repayment, you will get charged income tax (at your current marginal rate)

RRSP vs FHSA

The Federal Government introduced the First Home Savings Account (FHSA) in 2023 as a way for Canadians to save for their first home tax-free. Similar to an RRSP, any contributions made to an FHSA are tax deductible. FHSA account holders can contribute a maximum of $8,000 annually up to a lifetime limit of $40,000.

You can use both an RRSP and an FHSA to save for your first home. For instance, you can save up to $40,000 in your First Home Savings Account and withdraw up to $60,000 from your RRSP for a combined maximum of $100,000 per person toward the purchase of your first home.

Any amount saved in an FHSA that was not used to purchase a new home can be transferred to an RRSP. However, it’s worth noting that you cannot withdraw any amount transferred from a First Home Savings Account to your RRSP under the Home Buyers’ Plan.

Final Thoughts

While using your RRSP savings to purchase a home has pros and cons, it can be a great option for Canadians planning to buy their first home. It’s essential to consider your long-term financial goals before you decide where to save your down payment and closing costs.

RRSP for Down Payment FAQs

What happens if you don’t close on the home you withdrew funds to buy?

If you withdraw funds from your RRSP but the deal falls through and you choose not to buy a different home before October 1st, you can cancel your Home Buyers’ Plan participation. You can return the funds to your RRSP without penalty as long as the funds are returned by December 31st of the year you receive the funds.

Does the HBP work for everyone who buys their first house?

If you meet the eligibility requirements and your RRSP allows withdrawals under the Home Buyers’ Plan, you can use your RRSP funds to buy your first home.

Can I use my group RRSP to buy a house in Canada?

Some locked-in or group RRSPs do not allow you to withdraw from them under the Home Buyers’ Plan. Therefore, if you plan to withdraw funds from your group RRSP to buy a home, check with your plan administrator first.

What percentage do you need for a down payment in Canada?

The minimum down payment depends on the property’s purchase price and the type of home you are buying.

For homes under $500,000 the minimum down payment is 5%. The minimum down payment on homes priced between $500,000 and $1,499,999 is 5% on the first $500,000 of the purchase price and 10% on the portion of the purchase price above $500,000. Finally, the down payment on homes over $1.5 million is 20%.