There are few things in life more certain than taxes. Therefore, if you are selling a property in Canada, especially as a landlord, house flipper, or someone who has inherited a home, you should be fully aware of how capital gains tax applies to real estate transactions. Understanding this crucial element of Canadian tax law is vital, since it directly impacts the final profit you walk away with.

You may, quite naturally, be wondering how to avoid or minimize capital gains tax legally to ensure you keep a larger portion of that profit in your pocket. This often involves strategic planning and a deep understanding of exemptions, such as the Principal Residence Exemption, as well as the rules governing the sale of investment or secondary properties. While correctly navigating these regulations is key to maximizing your return on investment when selling real estate in Canada, we always recommend consulting a tax advisor for professional advice.

Key Takeaways

- Canadian capital gains tax is paid as part of your income tax return when you sell an investment asset

- Avoiding capital gains tax completely is difficult; however, there are several strategies that can reduce your tax bill

- Selling your principal residence is generally exempt from capital gains tax

What Is Capital Gains Tax in Canada?

A capital gain is the amount that an asset increases in value. An asset could be real estate, a stock, a bond, or a precious metal. Capital gains are often referred to as “realized” or “unrealized”. A realized capital gain is when you have sold the asset for a profit. Whereas an unrealized capital gain is when the asset has increased in value, but has not been sold.

In Canada, only a portion of capital gains is taxable. This taxable portion is included in your total income when you are filing your taxes and is subject to your marginal tax rate.

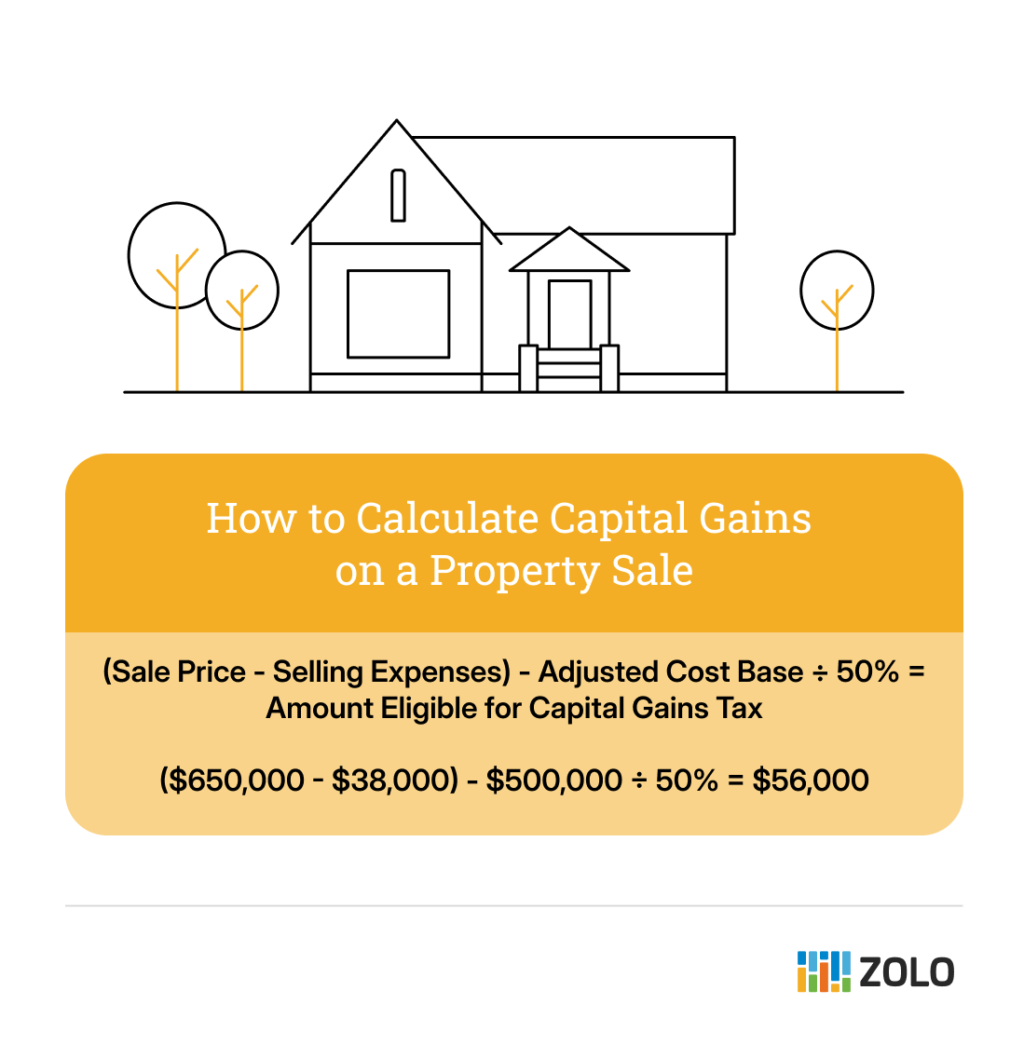

Calculating Capital Gains on a Property Sale

To calculate capital gains, you need to determine:

- The adjusted cost base (ACB) – calculated based on the original purchase price plus eligible expenses such as legal fees, realtor commissions, and capital improvements (like renovations)

- Selling price – the amount you sold the asset for

- Expenses incurred when selling – eligible expenses you paid to sell the property, such as closing costs and real estate commissions

For example, if you bought a cottage for $500,000 including fees (ACB), and later sold it for $650,000 (selling price), after deducting the expenses you incurred when selling, including 5% real estate commission fees plus Ontario sales tax, and $1,275 in legal fees (expenses), your realized capital gain would be $112,000.

However, not all of the capital gains are taxable. The inclusion rate for capital gains is 50%, meaning that you only need to pay capital gains on half of your profit. For instance, if you have a $112,000 profit from selling your cottage, $56,000 is taxable. You will report the capital gains on your income tax return. You will then be taxed at your marginal tax rate according to your income.

When Capital Gains Tax Applies to Property Sales

Whether or not capital gains apply to you when you sell a property depends on how that property was used. If the property was not your primary residence, you will likely need to pay capital gains. Here are common types of property that would be subject to capital gains tax:

- Secondary residence (cottage or second home)

- Investment property

- Land

Understanding the Principal Residence Exemption

Primary residences are exempt from capital gains, meaning that the most common way to avoid paying capital gains tax is to sell your primary residence. A primary residence can be any type of property, like a house, condo, mobile home, float home, or even a cottage, so long as it meets the qualifications set by the Canadian government. To qualify, you must own the property, either alone or jointly with another person, you must live in it at some time during the year, and you must designate it as your principal residence. You can only designate one home as your family’s principal residence for each tax year.

Canada Revenue Agency (CRA) rules state that if you sell any property, you must report the sale on your income tax return. If the home you sold was your principal residence for the entire time you owned it, you will not pay any capital gains tax. However, if it was not your principal residence for any of the years that you owned it, you will pay capital gains tax on part of the sale.

To claim the Principal Residence Exemption, you must report the sale of your principal residence on Schedule 3 and Form T2091 in the tax year you sell it.

Capital Gains vs Business Income: How CRA Determines Tax Treatment

When you sell a property other than your principal residence, the CRA uses several pieces of information to determine whether the profits of the sale are determined to be capital gains or business income. Several factors are assessed during this “intent test,” including:

- Your intent when you bought the property

- How long you’ve owned it

- How often you’ve made other property purchases and sales

- Renovations or improvements you’ve made to the property

- Circumstances of the sale

- The type of property

For instance, if you’ve bought many similar properties, owned them for a short period of time, renovated to improve market value and sold them for a profit, the CRA may determine this is business activity. On the other hand, if you bought a property for personal use as a second home and sold it years later, the profit is likely to be considered capital gains.

How House Flipping Sales Are Taxed

House flipping is buying a property with the intention of selling it quickly for a profit. Flipping usually involves remodelling the home before listing it for a higher price than what you paid. However, before you decide to flip a home, consider house flipping tax implications.

The CRA may view income from home flipping as business income instead of capital gains, especially if you’ve owned the home for less than one year. If determined to be business income, 100% of the profit would be taxable, instead of the 50% inclusion rate for capital gains.

Ways to Reduce or Offset Capital Gains (Within CRA Rules)

While it’s difficult to completely avoid paying capital gains, there are ways you can reduce capital gains tax, within the CRA rules, of course. Before you decide on a method to reduce capital gains tax, you should talk to a tax professional to understand the best options for your personal situation.

Calculate the Adjusted Cost Base Properly

To calculate your adjusted cost base (ACB), you start with the purchase price and add eligible expenses such as closing costs and lawyer fees. In addition, investments in the property, such as renovations (capital improvements), can be added to the adjusted cost base to reduce taxable capital gains.

Tax Shelter Your Earnings

You may consider placing your profit from selling your property into a tax-sheltered investment, like a Registered Retirement Savings Plan (RRSP). Since money placed in an RRSP reduces your taxable income, it lowers the amount of taxes you pay when you file your income tax return. In addition, RRSPs allow you to grow investments on a tax-deferred basis, which means that gains in registered retirement accounts like RRSPs are only taxed upon withdrawal.

Sell When You Have a Lower Income

The government taxes capital gains as part of your income, and your total income and tax bracket determine the final amount you pay. Therefore, selling a property during a year when your income is lower may keep you in a lower tax bracket, potentially lowering the capital gains tax rate you pay.

Use Capital Losses to Offset Gains

Capital losses are essentially the opposite of capital gains and occur when you sell an asset for less than you paid for it. Through a strategy called tax loss harvesting, you can claim capital losses to offset capital gains, which reduces the amount you owe in capital gains tax. If your capital losses exceed your gains, you can also carry forward the unused losses to future tax years.

Incorporate Your Rental Business

If you are selling a rental property, consider incorporating your rental business and transferring ownership to the new entity. When it comes time to sell the property, you will be taxed at a corporate tax rate, which is often lower than a personal tax rate, therefore saving you money.

Capital Gains on Inherited Property in Canada

You may be wondering about the tax implications of inheriting a property in Canada. The good news is that there is no inheritance tax in Canada; therefore, you will not owe anything just for receiving a property. However, the estate of the original owner may face capital gains before you take ownership of the property.

When someone dies, the CRA treats it as if any property they owned was sold at fair market value, a concept known as a deemed disposition. The estate is then responsible for paying any capital gains tax before assets are distributed to heirs. If the inherited property was the deceased’s principal residence for all the years they owned it, the estate can claim the Principal Residence Exemption to eliminate or greatly reduce capital gains tax. But, if the property is an investment property or a second home, such as a cottage, capital gains tax typically applies.

If you decide to sell the property, your adjusted cost base is the fair market value of the property; therefore you only pay capital gains on the difference between the fair market value and the final sale price.

For instance, if your parent owned a cottage that they originally bought for an adjusted cost base of $200,000, and its fair market value at the time of their death was $500,000, the estate would pay capital gains tax on 50% of the $300,000 difference.

Once the property is transferred to you, your adjusted cost base is $500,000. If you later sell the cottage for $525,000, you would pay capital gains tax on 50% of the $25,000 difference.

Proper estate planning is essential to reduce taxes; therefore, you should consult with a tax professional before selling an inherited property.

Common Capital Gains Tax Mistakes to Avoid

Capital gain tax errors could lead to serious tax consequences. Here are some of the most common mistakes people make considering capital gains:

Failing to Track the Adjusted Cost Base (ACB) Correctly

The ACB is the original cost of the property plus any expenses to acquire it, such as commissions and legal fees. Undercalculating the ACB will result in an artificially high capital gain and higher tax liability. On the other hand, overstating the ACB to lower your reported gain is an error that can lead to reassessment and penalties if discovered by the CRA.

Misapplying the Principal Residence Exemption (PRE)

You must formally designate the property as your principal residence on your income tax return for the year you sell it. Failing to do this can result in the CRA denying the PRE, making the entire gain taxable.

Mixing Personal Use and Income-Generating Use

If you convert part of your principal residence into a rental property or business space, the PRE may be partially or entirely forfeited for that period. You must track the percentage of the property used for income generation, as that portion is subject to capital gains tax upon sale. Failing to report this “change in use” in the year it occurs is a significant error.

Ignoring the Tax Implications of “Deemed Dispositions”

The CRA can treat an asset as sold even if no actual sale occurred. Common examples include:

- Change in Use – For example, converting a personal residence to a rental property, or vice-versa.

- Gifting an Asset – Transferring capital property to a non-arm’s-length individual (like a family member) is deemed a sale at fair market value (FMV) by the CRA, potentially resulting in a taxable capital gain for the giver.

- Emigrating from Canada – For individuals who become non-residents of Canada, a deemed disposition of most capital properties (with certain exceptions) is triggered, as if they were sold at FMV upon departure.

Not Utilizing the Capital Loss Carry-Back/Carry-Forward Rules

Capital losses (selling for less than the adjusted cost base) cannot offset regular income. However, they can offset capital gains: used against current year gains, carried back three years, or carried forward indefinitely. Failing to use this mechanism results in overpaying taxes.

Failing to Report the Sale of the Principal Residence (Even if Fully Exempt)

Since 2016, the CRA has required Canadians to report the sale of a principal residence on their tax return, even when the PRE covers the entire gain. If you fail to report the sale during the year it occurs, the CRA may charge late-filing penalties or deny your exemption entirely.

Bottom Line

As the saying goes, there are two things in life that are certain, and taxes are one of them. It’s essential that you understand capital gains taxes in Canada before you sell a property to avoid a surprise bill at tax time. Consider consulting a tax professional before listing your home for sale.

Avoid Capital Gains Tax FAQ

Is capital gains tax different for seniors in Canada?

No, there are no different capital gains tax rules for seniors in Canada.

How long do you need to live in a home to claim the principal residence exemption?

Generally, you must live in the home for at least one year (365 days) and designate the property as your principal residence. If you maintained the home as your principal residence for the entire ownership period, you will not pay capital gains tax when you sell. However, if you did not use the home as your primary residence for any of those years, the principal residence exemption may not cover all or part of your reported capital gain.

Do condos and houses have different capital gains rules?

Any type of property is subject to the same capital gain tax rules. This includes condos, houses, cottages, townhouses, mobile homes, and others.

Can CRA reassess a property sale years later?

The Canada Revenue Agency (CRA) can reassess the sale of a property at any time. As of 2016, if you sell your principal residence and have not reported it, they may reassess you at any time. In addition, late-filing penalties may apply, up to a maximum of $8,000.

When should you consult a tax professional before selling?

You should consider consulting with a tax professional before you sell any property that isn’t your principal residence to ensure you understand the tax implications of the sale.