Buying a home isn’t always easy at the best of times. With high property prices, becoming a homeowner almost feels like a fantasy for most young people. So, as a parent, buying a house for your child in Canada may seem like the only option for them to get into the expensive real estate market these days.

On the flip side, looking at the financial realities of helping your children buy real estate is essential. After all, it’s your money on the line. So, considering your financial situation is step one. But first, consider whether buying a house for your child is a good idea and what scenarios could work for you.

Why You Might Want to Consider Buying a House For Your Child in Canada

Relying on family help to buy a home has become the norm in Canada. According to our 2024 Housing Market Report, 48% of homebuyers used money from their or their partner’s parents or relatives, and another 20% used money from an inheritance.

We discovered that 71% of Canadians worried they could never become homeowners, while 67% felt they couldn’t afford a home in their city based on the average price. Yet, Canadians want to be homeowners so badly that 77% of the people polled admitted that they would put off saving for retirement if it meant they could be a homeowner sooner. We also found that 21.5% of Canadians want to get into the real estate market to start a family.

When you look at these factors, along with the fact that it simply takes a long time to save up for a down payment since home prices are increasing, you may want to consider buying a house for your child or helping out in some way.

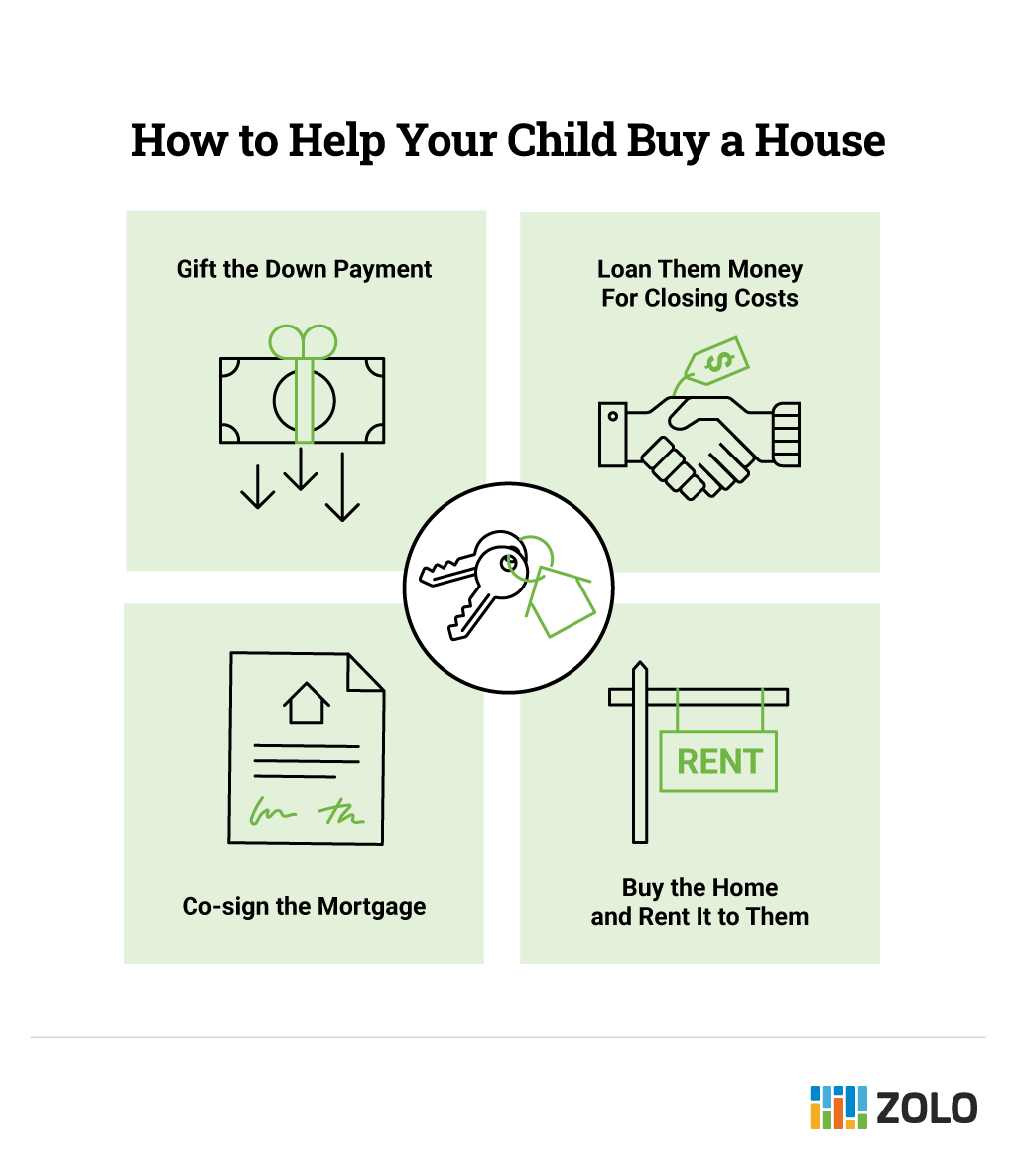

Different Options For Helping Your Children Become Homeowners

There are many unique ways to help your child become a homeowner in a challenging real estate market.

1. Gift the Down Payment

Gifting money for the down payment — or, at the very least — helping them save for this significant chunk of the home price is one option. For many, saving a down payment alongside their other expenses and goals can be a barrier to entering the real estate market. You could cover the entire down payment or develop the missing percentage to help speed up the process.

To help your child save for a down payment, you could help them contribute to a First Home Savings Account (FHSA). This powerful account allows Canadians to save up to $40,000 tax-free towards the cost of their first home. However, only the account holder can deduct any contributions made to a FHSA.

Not only would this relieve the stress of saving for your adult children, but it could also speed up the process and allow them to enter the market at a more optimal time. In addition, your child could also avoid paying the Canada Mortgage and Housing Corporation (CMHC) mortgage insurance if you give them the funds needed for an adequate amount. That way, they don’t fall under the threshold of 20%.

2. Loan Your Child Money for Closing Costs

If you’re not in the financial position to give a full down payment to your child, you could loan them the money to assist in additional closing costs. This money could go towards closing costs or the funds accompanying the increased spending that comes with being a property owner, like moving.

There are many conflicting anecdotes about how to loan money to a family member for a house. It depends on your relationship with your children and what kind of loan agreement you create. A flexible loan could ease the burden on your children as they struggle to become homeowners.

3. Cosign the Mortgage

Suppose you’re not financially comfortable with loaning or giving a down payment. In that case, you can use your solid credit to assist your kid with getting approved for their mortgage, for example, by becoming a guarantor or co-signer on their mortgage loan.

There are differences between co-signing and being a guarantor. For instance, a guarantor is not listed on the property title, and they do not share property rights. If you choose to be a co-signer, you will be listed on the property title as part owner of the property and equally responsible for the repayment of the loan.

While co-signing a mortgage comes with risks, it’s an easy way to assist without spending any of your money. But, of course, your child must be able to afford the mortgage payments to avoid defaulting.

What are the risks of co-signing a loan?

- The entire loan becomes your responsibility

- It will impact your credit rating

- It may affect your ability to borrow money from lenders

- Co-signing can cause distress in a relationship

4. Buy a Home and Rent it to Your Child

Another way you could help your child out that could benefit you is to purchase the home and rent it to them for a discounted price or agreed-upon rate. Doing this could set up an arrangement where you both get ahead financially.

What to Consider Before Buying a House For Your Child In Canada

As you know, buying a home is a serious financial obligation. It can be even heftier to consider funding your child’s home purchase. As much as you want to help your child out, you must be able to do so because you don’t want to compromise your retirement or living situation.

Things to consider before buying a house for your child in Canada:

- Your retirement plans – You want to ensure that you have enough money saved to retire at a reasonable age and then live comfortably.

- Your own mortgage – If you have a mortgage of your own, you want to ensure that you’re contributing to it to cut down on your expenses as you wind down your career.

- Other children – Do you have additional children who might expect the same assistance when buying a home?

- Tax implications – If you donate a property to your child, it will be treated as being sold at its fair market value, even if no money is exchanged. This means you are subject to capital gains tax.

Buying a house for your child in Canada isn’t easy because real estate prices have skyrocketed in the last few years, so there’s a substantial cost involved.

Final Thoughts: Should You Buy Your Child a House in Canada?

As you can see, there’s no easy answer here. When you factor in high property costs with rising interest rates and soaring inflation, it’s no wonder millennials are discouraged about the possibility of becoming homeowners.

Here are a few other points to consider before buying your child a home:

- Could you possibly downsize? I spoke with a friend who got assistance from their parents because they were looking to downsize. So, the parents sold the family home to the kid for a heavily discounted price and moved into a smaller unit.

- Could this gift be their inheritance? This would save them from hefty probate fees after your passing, and the money would be much more beneficial now than when they’re older.

It makes sense to help out in one way or another if you’re in the position to do so since you would greatly help out your children, who are dealing with high real estate prices and higher rates. We urge you to think about your own financial future and retirement situation so that you don’t put yourself in a difficult position as you near your golden years.

Buying Your Child a House in Canada FAQs

Is it better to buy my parents’ house or inherit it?

There are benefits and drawbacks to buying or inheriting the family property. If you buy your parents’ home for less than fair market value, the difference is called a gift of equity. The gift of equity can serve as your down payment.

On the other hand, if you inherit your parents’ home after they pass away, the property will be issued after the probate process. In general, there are no fees for inheriting a property, as the estate typically covers legal and probate fees.

It’s best to consult a lawyer and tax advisor to make the best decision for your situation.

How to hold a mortgage for your child?

If you’d like to help your child qualify for a mortgage, you could become a guarantor or co-signer on the mortgage loan. A guarantor agrees to make payments if the borrower defaults. On the other hand, a co-signer is equally responsible for the repayment of the loan.

Otherwise, you could purchase a home to rent to your child and allow them to inherit the property at a later date.

How to pass property from parent to child?

There are multiple options for passing a property from a parent to a child. For example, property can be transferred through sale, donation, or inheritance. The legal and financial implications for each option differ. It’s essential to consult a lawyer and tax advisor to avoid unforeseen consequences.