This column is adapted from House Poor No More: 9 Steps that Grow the Value of Your Home and Net Worth, the new handbook on smart homeownership and available for purchase starting November 16, 2021.

Most people believe the key to wealth is to make more money. There is no denying that earning more makes it easier to accumulate assets, but that doesn’t mean a high-paying job is critical to achieving financial independence. It isn’t.

What is Financial Independence?

Financial independence is the status of having enough income that you can pay your living expenses now and into the future without having to be employed or dependent on others.

Based on this definition, it’s easy to assume that financial independence is synonymous with retirement; earn enough, save enough, invest enough so you can eventually stop working and still pay the bills.

But retirement isn’t the goal. Just as getting a high-paying job or accumulating a large amount of money in a savings account or investment portfolio aren’t goals. Instead, these achievements are milestones and can be used to mark accomplishments and as tools for further success.

Role of a Homeownership in Meeting Our Needs

At this point, we could spiral into an existential discussion about the purpose of life and the definition of a good life. We won’t. But we do need to understand a little about human motivation. An easy way to do this is to use a popular framework developed by humanist psychologist Abraham Maslow.

According to Maslow, human behaviour is motivated by a hierarchy of needs. Each decision or action taken is based on our motivation to satisfy each need. We must meet the most basic needs first before we move up through the hierarchy of human needs.

Using Maslow’s framework, we can examine the decision to buy a home.

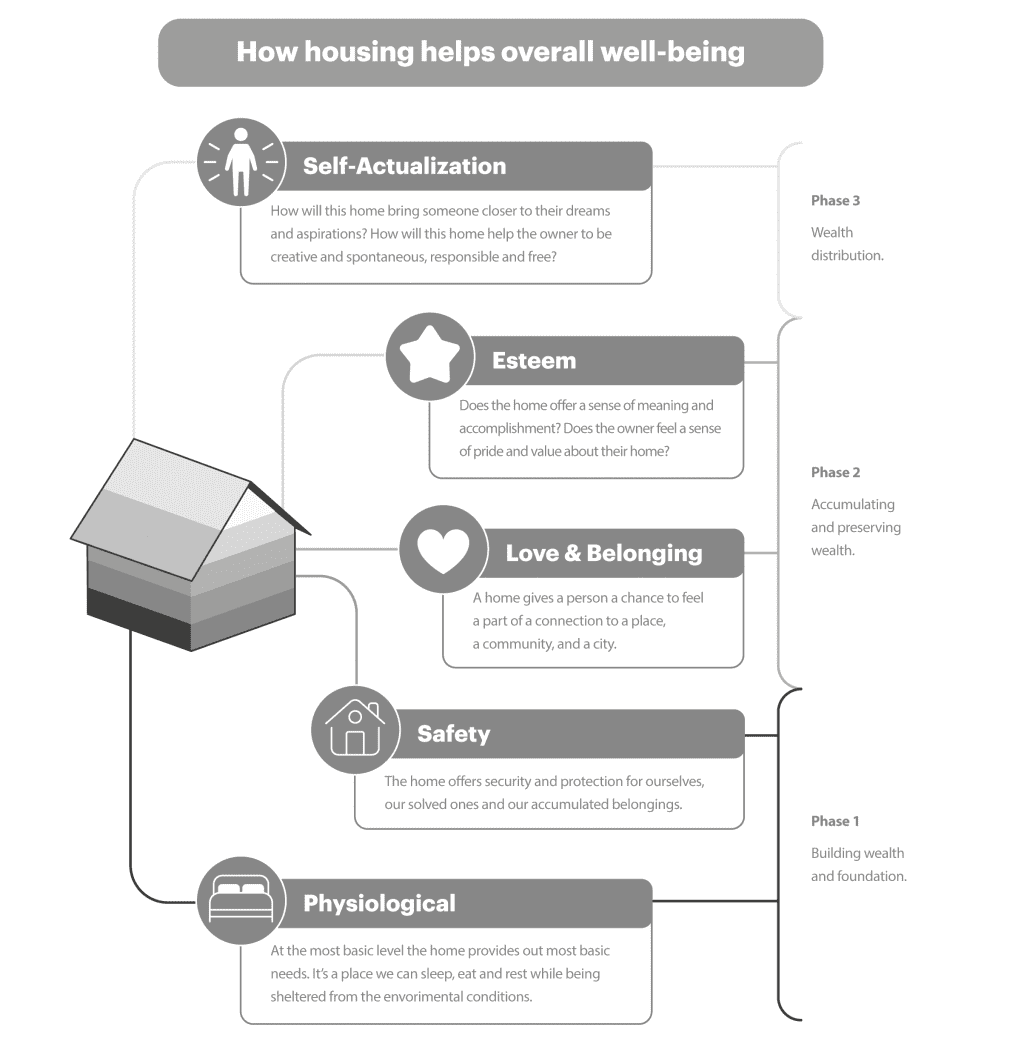

A place to live helps satisfy our physiological needs; it gives us a place to sleep and protects us from the elements. But stable housing meets more than our base needs. It lays the foundation of security and allows us to build community, create a sense of belonging, and give us a solid foundation to grow. Through homeownership, we may also achieve the financial independence (arguably Level 5 in Maslow’s hierarchy of needs).

- Level 1-Physiological: At the most basic level, the home provides our most basic needs. It’s a place we can sleep, eat and rest while being sheltered from the environmental conditions. The home satisfies our physiological needs if we can store, prepare and eat food and keep our belongings and ourselves safe.

- Level 2-Safety: The home offers security and protection for ourselves, our loved ones and our accumulated belongings. Knowing that we can explore and define our lives—through the hobbies, sports and activities we enjoy—and that we have a safe, happy place to return is an integral part of a home.

- Level 3-Love & Belonging: A home gives a person a chance to feel a part of—a connection to a place, a community and a city. This attachment enables homeowners to focus on allowing other relationships with friends, family, neighbours and community to blossom.

- Level 4-Esteem: Does the home offer a sense of meaning and accomplishment? Does the owner feel a sense of pride and value about their home? Whether it’s a first home or part of a retirement plan, the home offers the owner the ability to set and achieve goals and gain respect from success.

- Level 5-Self-actualization: How will this home bring someone closer to their dreams and aspirations? How will this home help the owner be creative and spontaneous, responsible and free, live within their ethics and abide by their principles? How will this home help the owner move towards becoming the most capable, best self?

Since housing plays a critical part in building a solid foundation upon which all needs are met, our home becomes a keystone—a critical or vital component that helps hold the entire system together. That system is all the milestones, decisions and steps towards financial independence.

Stable Housing Isn’t the Same as Owning A Home

The great news is that anyone can build a solid foundation, achieve milestones, learn and master tools and achieve financial independence—and owning a home isn’t a requirement.

The key is stable housing—not homeownership. Stable housing is reliable and safe; it meets current and future needs and allows community building and personal growth.

How Homeownership Factors into Financial Independence

What does all this have to do with financial independence? Or, for that matter, buying a home?

Everything.

Turns out the human race has managed to adapt and evolve because we relied on mental shortcuts. These shortcuts, known as heuristics, allow for efficient cognitive processes. This helps us solve problems, absorb new knowledge and adapt more quickly. (Read more on the three key heuristics we use—representativeness, anchoring and adjustment, and availability).

By and large, we use mental shortcuts when it comes to mapping out our financial independence. Some of the more common milestones—tools that worked well in the past—are now considered sacred cows. Homeownership is one of these sacred cows. Despite attempts to validate or question its role in achieving financial independence, becoming a homeowner remains iconic throughout North American culture.

Truth is, the milestone of buying a home has become so ingrained in our culture of #adulting and #achievement that we forget that buying property isn’t the goal—financial independence is the goal.

Evidence of this misplaced sense of achievement can be seen in how we frame whether or not to buy a home. Rather than assess the decision based on needs, goals and calculations, we’ve created shortcuts.

- Buying a home is smart.

- Buying a home is foolish.

Regardless of which side of the fence you sit on, the ‘smart’ decision is the decision that allows you to buy low and sell high or opt for the fiscally responsible choice and refuse to take on the financial burden of mortgage debt.

Sadly, this is an oversimplification of a critical decision that reduces the choice of becoming a homeowner to a zero-sum decision: Either you’re smart or not.

What’s worse is that all this focus on the milestone of homeownership actually obfuscates the real goal: The ability to live a life that offers choice without relying on others to pay your way. We forget that the milestone is one step towards the goal of financial independence.

Buying a home is like childbirth. It’s a wonderful moment that needs to be celebrated, but we can’t stay stuck in that moment. Celebrate! And then focus on the bigger picture.

(Plus, I’d argue that it denies the lived experience of the vast many who choose to purchase a home as part of a smart financial decision-making process, even in expensive real estate markets.)

Turn a Property Purchase into Smart Homeownership

Wax-on. Wax-off, right, Mr. Miyagi? (For those that don’t know the reference, this is from the original Karate Kid.) All this talk about heuristics and existential choice is all well and good, but what does it mean?

It means that mental shortcuts can help solve problems and speed up our decision-making but relying on shortcuts can also lead to inaccurate judgments and errors in our decision-making. Worse, our repeated reliance on heuristics can cloud our ability to see alternative options and come up with new ideas.

This bias is significant when you consider all the arguments against buying a home. Over the last decade or more, almost every criticism regarding homeownership attempted to establish homeownership as a financial liability.

And, I would agree.

Homes cost homeowners. Sometimes they cost homeowners quite a lot.

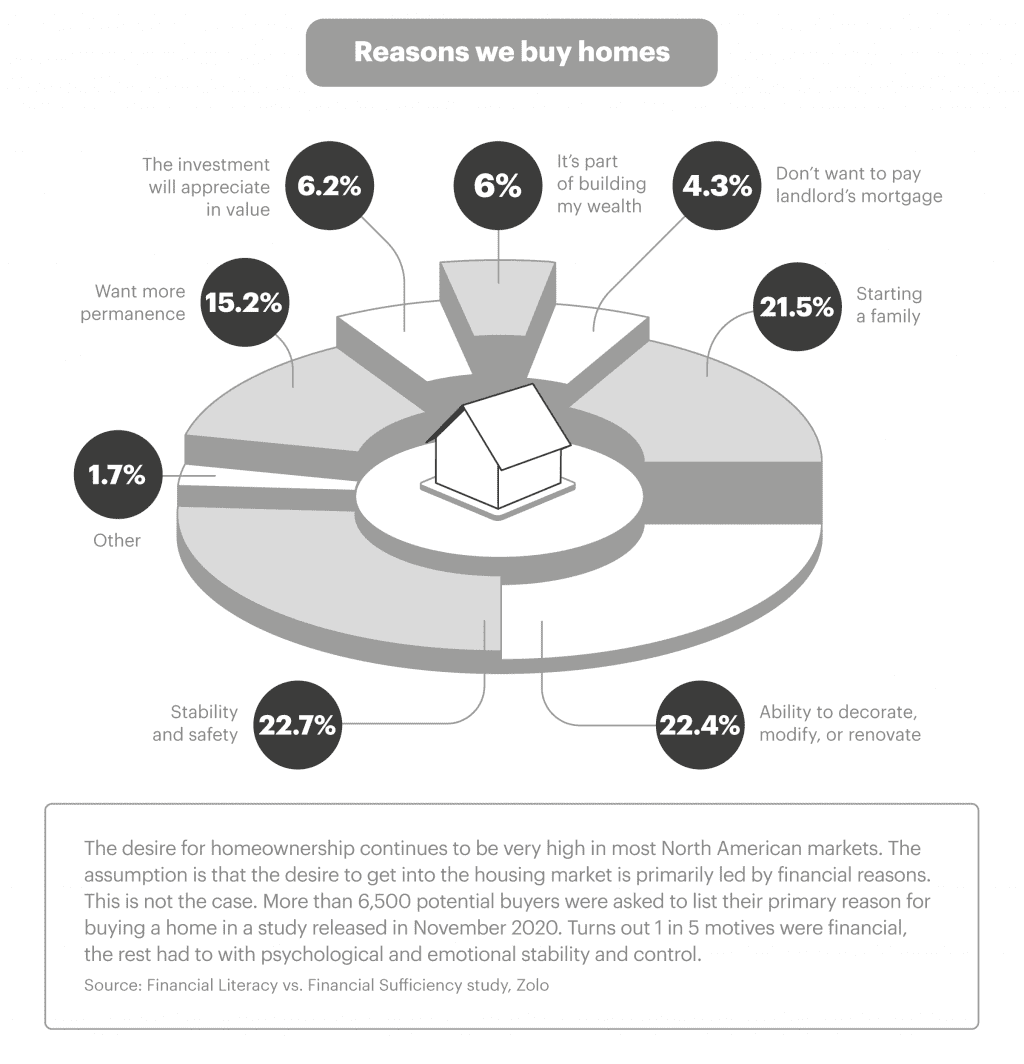

But the biggest reason for buying a home is not for financial security—it’s to establish emotional stability and physical security.

We buy homes when we fall in love; we buy homes when we get married; we buy homes when we grow our family; we buy homes when we move, and we buy homes as a way to earn income. While there are financial consequences to this decision to purchase property, the primary motivation isn’t financial; it’s our emotional need for security and stability.

This perspective helps to explain why buyers rush into the real estate market despite frothy price escalations, predictions of bubbles, threats of market crashes and persistent arguments that homeownership is an unwise financial decision.

To turn a property purchase into smart homeownership, we need to stop justifying our reasons on why we buy homes—and start concentrating on learning how to use this tool to help with wealth accumulation.

Smart homeowners tune out the noise and double down on solid financial decisions. It means knowing how your property is valued and how to maximize and use that value to grow your net worth. It’s about using your home—and your smarts—to make wise decisions when it comes to housing, lifestyle consumption and wealth accumulation. It also means ignoring the zero-sum mentality that you need to choose between homeownership and other, just as important, wealth accumulation goals.

The very act of buying a home requires us to learn and execute money skills that are integral to financial independence. Buying a home requires us to save money, the discipline of using a budget, and the adoption and use of other money management tools that are critical to overall financial independence.

Buying a home is often the first real test of our relationship to money—and the cycle of learning about money management, also known as financial literacy.

What Is Financial Literacy?

Financial literacy is the ability to understand and effectively use various financial skills, including personal financial management, budgeting, and investing.

How It Contributes to Financial Stability and Independence?

Studies show that the earlier you start learning and practising money management, the better off you will be—in earning, saving, spending and investing money.

Unfortunately, there is no national financial literacy program in Canada. While individual school districts started to introduce and incorporate financial literacy into the education curriculum, there remains no universal or unified lesson plan—with goals, milestones and a standardized set of tools.

As a result, many impose their own version of financial literacy bootcamp as soon as important milestones are considered (or arrive). If that’s where you find yourself, not to worry; you are not alone.

Start Using Your Home as a Tool to Achieve Financial Independence

In general, most of us start and stop learning critical money skills once we’ve bought the home and established a debt-repayment schedule (aka: mortgage).

We learn to save; to budget; to comparison shop and we learn the power and impact of compound interest and the joy of amplified gains through leverage (or the magnitude of losses, on the flipside).

Most, however, don’t expand upon this knowledge or explore the options and tools available to them—tools that can help accelerate wealth accumulation and the achievement of financial independence.

To help kickstart the motivation to explore and develop these tools, here are seven takeaway lessons from my new book, House Poor No More: 9 Steps that Grow the Your Home’s Value and Net Worth.

Use each takeaway as a building block—a critical reminder to not stop at a milestone celebration but push on towards your actual goal.

The best part is that there is no one-size-fits-all solution when it comes to effectively integrating your home—and the use of equity, leverage and smart spending decisions—into a wealth accumulation strategy. How you use credit, debt and the value of your asset(s) can shift and change, depending on your strategy, age, risk tolerance and goals. But to be successful, you have to start.

(The selected Takeaways were taken from Chapter 5 and 6 of House Poor No More: 9 Steps that Grow the Value of Your Home and Net Worth.)

Start Small for Big Impact. As author James Clear illustrated

in his book Atomic Habits, small habits build up to big impacts.

Trying to make wholesale changes can be overwhelming. Instead,

start with one change, like unplugging unused electronics. Once

that’s a habit, move on to the next change. Taking small steps to

reduce our energy consumption may feel like baby steps, but over

time, energy goes down and savings add up.

Don’t Lead with Your Emotions. Heed Your Emotions. Buying or selling based on fear—either fear of missing out or fear of worst-case scenario—is never good. You might luck out and have it work out, but it’s a gamble. This doesn’t mean you should dismiss your emotional needs. Even though paying off your mortgage isn’t always the optimal use of your hard-earned money, the peace of mind that comes with eliminating debt is huge. The key is to act objectively according to your plan, which was created based on your personal, emotional needs.

Celebrate Small Wins, but Don’t Get Stuck at the Party. Paying off a mortgage isn’t a goal—it’s a milestone towards wealth-building and financial independence. Growing your investments isn’t a goal—it’s a milestone towards wealth-building and financial independence. Celebrate your small wins, but don’t stop at a milestone. Keep forging ahead towards your ultimate goal (however that may look).

Saving Is Smart. Assuming a Home Is a De Facto Retirement Fund Is Stupid. Buying a home doesn’t exempt you from the need to save for retirement, a child’s education or anything else. But your home can be used as part of a plan to save and invest. Include your home—both the debt you owe and the equity you’ve built up—as part of your saving and spending plans.

Home Equity Is a Tool. Use It. For many homeowners, most of their net worth is in their home. From a diversification point of view, this sucks. Leverage this equity by borrowing and investing in equities and fixed income to help diversify your overall portfolio.

Effective Wealth-Building Uses the Entire Earning-Saving-Spending Life Cycle. To build wealth, you need to maximize the use of each dollar earned and invested. In general, the order of priority means paying off all expensive, non-deductible debt (i.e., credit card balances and personal loans) first, then tackle less-expensive non-deductible debt (such as a mortgage loan). Use investment dollars to start building a portfolio in tax-sheltered accounts with a focus on capital gains for long-term growth and Canadian dividends for income. At all times, try to maximize the tax efficiency of every dollar earned and invested. Do this, and you’ll be maximizing how effective each available dollar is used in your earn, spend and save life cycle.

Earnings + Leverage Helps You Build More Wealth. Most of us won’t get wealthy trading time for money (aka working). Leverage enables you to cut the time, cost and effort necessary to reach your personal and financial milestones. Leverage magnifies your efforts—or your potential losses. Although it’s not difficult to master, the key is learning how to use it based on your needs, goals and risk tolerance.

Homeownership can be an incredibly potent tool. It allows you to start and strengthen your saving skills, flex your money management, and ‘beast up’ your wealth accumulation strategy through the power of leverage. The aim is to create a system where your money works for you. The goal is financial independence.