As soon as you decide you are ready to be a homeowner, you tend to look at how much home you can actually afford and what type of home you dream of buying. Either way, the price will be the primary focus. Price determines how large of a down payment you will need and what your maximum affordability is. Ignore these details and you run the risk of putting yourself into high financial stress and turning your homeownership dream into a nightmare.

Before you buy, your mortgage broker or lender will provide you with maximum affordability. Typically, they determine this number by looking at your total down payment and your debt to income ratio. In other words, how much money do you have upfront, and how much debt do you carry in comparison to your earnings. Of course, there are other factors, but these two points are a good indicator of how much home you can afford.

We asked nearly 300 Canadians about their home buying experience, and many (26%) are pushing themselves to the limit by buying houses at their maximum affordability.

Your Affordability Window

When looking for homes, you may hear people joke that you don’t want to choose something too expensive and wind up house poor. What they’re really saying is that by buying outside of your affordability window, you will end up rich in house and poor in cash.

If you spend a significant amount of money on homeownership, be it through a mortgage, property taxes and maintenance, you may feel a financial burden trying to meet other obligations and essential (or non-essential) purchases.

Although it may seem small, 18% of Canadian homeowners feel house poor. Even if they don’t feel house poor, they are pushing it to the limit by buying homes that they’d be unable to afford should themselves or their partners lose their job.

How Can You Ensure Your Mortgage Is Affordable?

With 49% of homeowners worried about paying their mortgage due to job loss, there are a few things to consider to ensure you don’t end up feeling house poor before you buy a home.

1. Consider Your Worst-Case Scenario

If you’re buying as a dual-income partnership, it’s best to buy a property that you’d be able to afford on one salary should something unexpected happen.

2. Start to Budget Before You Buy

Put together a mock budget with your estimated monthly income, mortgage, housing expenses and non-essential spending to ensure you can afford to live the lifestyle you want.

3. Save Up a Larger Down Payment

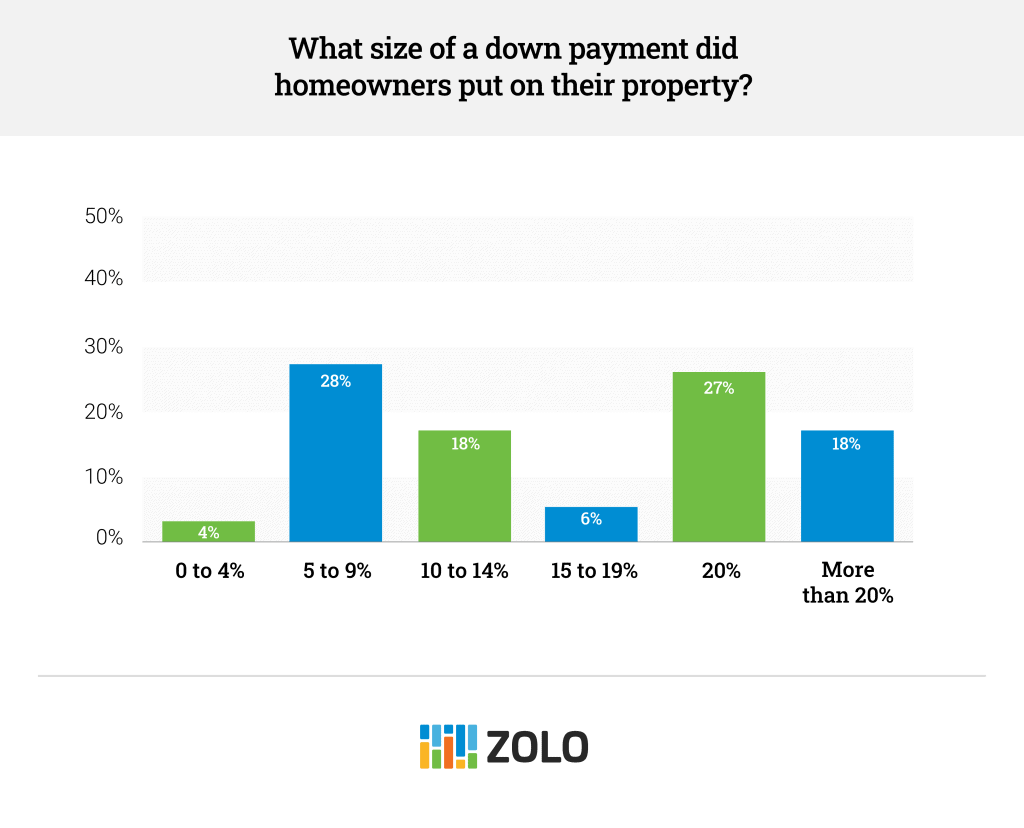

If you put a more significant down payment on the purchase of your home, you can keep monthly mortgage payments low. Of course, if you can afford to put down 20% or more, that’s ideal, and thankfully, nearly 27% of surveyed homeowners did just that.

Results show that 32% of Canadians put less than 10% down on their home — but the sweet spot for a down payment is actually 10-15% — which can typically score you a better interest rate. Putting down less than 10%, although sometimes the only way you can break into the real estate market, is a financial risk in itself. It’s better to be patient and save up as much as you can for your down payment to avoid having to pay a higher monthly mortgage payment.

The Dangers of Buying at Your Maximum Affordability

A common theme in the Canadian real estate market is buyers with financial support. For many, friends or family provides a little more of a cash flow to supplement their down payment and push them to the 20% mark.

Although it doesn’t make sense to turn down financial support if you are privileged enough to access those funds, it doesn’t always set you up for success as a homeowner. A larger down payment provides you more considerable maximum affordability, but as we’ve already noted, that can be when we put ourselves in a danger zone.

To protect yourself, one thing you can do is save up a solid emergency fund before you take possession of your first home. Unfortunately, 37% of Canadian homeowners missed the mark on this essential financial tip that can make you feel more comfortable and avoid feeling house poor.

To save an emergency fund, consider putting enough money away to cover at least three months of mortgage payments or enough to cover the cost of your most significant appliance breaking down unexpectedly. That, and make sure you have enough home insurance coverage to protect yourself from things outside of your control.

What Can You Do if Your Mortgage Is Too Expensive?

Because preparing for homeownership isn’t always something we do when we’re excited, it can feel too late to avoid that feeling of being house poor. To help, we asked Alexandra Boland, Certified Financial Planner, what to do if your mortgage is too expensive, and here are her top tips for creating more room in your budget.

1. Evaluate Your Monthly Expenses

Itemise your monthly expenditures over the last 6 to 12 months. This helps you identify recurrent spending that you can reduce to make room for a full mortgage payment. Once you have reduced discretionary spending to the extent possible, consider the following few options.

2. Find a “Roommate”

Although it might not be your first choice, you won’t be the only one. In a recent Zolo survey, we found that 2% of homeowners live with roommates. So renting out part of the house may generate enough income to solve your cash flow problems — and provide you with the ability to live the lifestyle you genuinely want.

3. Restructure Your Mortgage

Contact your mortgage broker or lender to consider restructuring your mortgage. There may be an opportunity to reduce your mortgage interest rate, reducing your monthly payment and the total interest cost. However, if that is not enough to bridge the gap, consider extending the amortization.

For example, a $500,000 mortgage at 2% interest amortized over 25 years vs 20 years reduces your monthly payment by approximately $400 per month. The downside is that extending your mortgage repayment by five years increases the total interest cost in this example by roughly $29,000 over the life of the mortgage (more if rates rise in the future, which is likely). You can mitigate the higher interest cost by accelerating your mortgage payments in the future when your cash flow improves.

Restructuring our mortgage for the reasons described will trigger a breakage fee unless the changes are made at term renewal. Please ask your mortgage broker or lender to calculate your breakage fee and how long it will take to recoup it through your new lowered mortgage payments (also known as the breakeven point).

Warning: If extending the mortgage helps you balance your budget, you’re not out of the woods. Houses need ongoing maintenance that requires regular capital over and above the cost of the mortgage, property taxes, and utilities. So be realistic about your ability to fund home maintenance, which is an integral homeownership cost.

4. Consider Selling

The home may not be affordable. You either over-committed yourself financially by coming too close to your maximum affordability, or your circumstances have changed significantly since the purchase. Adjusting other areas of spending or refinancing your mortgage may not solve the problem. Selling the property and purchasing a less expensive property (which eliminates some debt) may help you balance your budget. Selling and renting should be evaluated too.

No matter what you decide to do, the best approach to homeownership and dealing with a tight budget is always unique to your financial circumstances.

If you’re unsure, the best course of action is to speak to your mortgage professional and a financial planner to help you gain a clear understanding of what options exist and how best to approach your next steps. At the end of the day, if you feel house poor, you are certainly not the first — or last — homeowner to be in this situation.