Coming off some of the most volatile years in Canada’s real estate and housing market, it’s safe to say that buyers and sellers have a hard time imagining what the market could look like in one or two years. Various factors like house prices, interest rates, and new banking regulations competing for these individuals’ attention can create fear or doubt when trying to make a real estate decision.

While the market looks strong this spring against more interest rate hikes, the setup is eerily similar to last year’s spring market. There is a lot of attention on the growth in house prices and interest rates. But what does this mean for buyers and sellers?

Let’s take a look at the full scope of what’s happening right now to impact the real estate market.

What is Happening in Canada’s Spring Real Estate and Housing Market?

With the US Federal Reserve signalling two more hikes after their most recent decision to “skip” their most recent hike, more work seems to be done to control inflation. Further hiking could mean that central banks have departed the “soft landing” ideology and are pushed to the unfortunate reality that a hard landing, and a recession, could be the only way to get inflation back down to the target range.

After all, recessions have a 100% success rate of getting inflation back down to the target range — which takes about 16 months. This is why CIBC’s Chief Economist Benjamin Tal states that the Bank of Canada will always choose recession over inflation.

How Do House Prices Look in Canada’s Real Estate and Housing Market?

To think about the future, we must understand what the Bank of Canada looks at when raising interest rates. If the Bank of Canada feels compelled to continue hiking rates to cool the economy, it’s because it appears strong on paper.

This assumption is based on unemployment at a record low and house prices growing from January until May. House prices grew at the fastest home price appreciation ever for the first five months of the year and the second fastest home price appreciation in a consecutive four-month period.

According to the Canadian Real Estate Association (CREA), prices have grown around 10% to 15% across the country since January, equivalent to the beginning of 2022, before the Bank of Canada’s interest rate increase of 25 basis points. The spring market growth ended the same way this year — with a 25 basis point increase from the Bank of Canada. This “unpausing” hike seems to have shaken consumer sentiment and slowed price growth, as many buyers and professionals were anticipating that rate hikes were over.

Generally, we saw a spring housing market that was chasing affordability. But, for some, buying a home doesn’t even feel possible, with 63% of Canadians who don’t own a home admitting to having “given up” on ever owning one. Because of this, entry-level or starter homes seem to be the most sought-after property type. This is causing a frenzy of buying along the price floor.

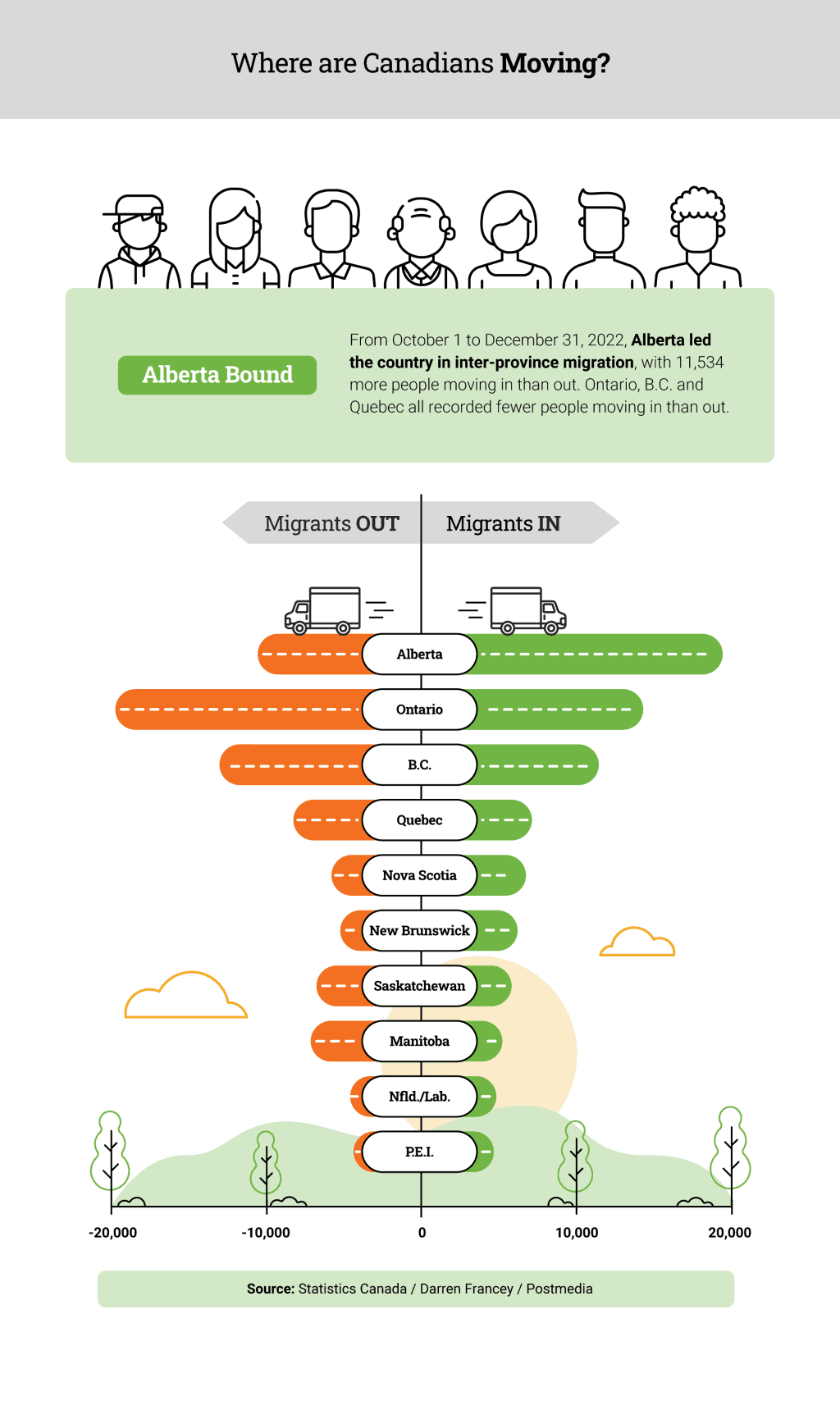

Why are Canadians Moving?

Housing affordability is key for buyers, making cities like Calgary, Edmonton, Moncton and Halifax appealing. The data tells us the same story: in the first few months of the year, Calgary was the most searched city in Canada, and Edmonton was the fourth most searched. Interprovincial migration shows large groups of people leaving Ontario and British Columbia and moving to more affordable areas.

Buyers who felt excluded from the market for the past several years felt opportunistic toward the steep price discounts at the beginning of this year. But we’ve seen those discounts exhausted as buyers aggressively bought property throughout the spring.

What Could Increase Home Prices?

This rollercoaster of volatility in Canadian house prices has left many buyers wondering whether or not prices go up or down from here in Canada. Let’s start by looking at economic factors that could cause house prices to increase in Canada.

- Canada’s population grew by 1 million last year

- Canada was the top global destination for international students in 2022, which supports the demand for rentals

- Rents are rising — and when rent prices rise, investors’ willingness to pay for property increases

What Could Lower Home Prices?

Now that we’ve explored what could cause house prices to increase in Canada let’s look at the alternative scenario and explore what factors could push prices down in Canada.

- OSFI is regulating Canadian banks to hold more cash, meaning interest rates could go up further

- Interest rates are going up (again) after a short “pause”

- The Bank of Canada is suggesting that interest rates will have to be higher for longer

- Many indicators suggest a recession is on the horizon

- Household net worth is in decline

- Household savings are in decline

- Credit card debt is increasing

Either way, it’s important that buyers and sellers keep an eye on both the economy and the real estate market to make good financial choices regarding their desire to own or their decision to sell.

How Can Buyers and Sellers Manage this Market?

If you plan to buy or sell property in the second half of the year, you might be wondering what you can do aside from monitoring the news and staying in the loop with your local market. The key thing to remember is that most of what happens within the economy or real estate market is outside of our control. So, as buyers and sellers of real estate in Canada, we must focus on the things we can control — and here are some of those things:

What Should Buyers Do?

- Understand seasonality: house prices go up and down throughout the year

- Don’t be afraid to negotiate: good deals are made, not found.

- Manage downside risk: look at the fundamentals of the property

1. Seasonality

Look for seasonal cycles in real estate throughout the year. Ask your realtor to show you the average monthly price over the last several years. Every market has clear increases and decreases in market strength and price. It’s easy to get wrapped up in the fear of missing out (FOMO), especially in a hot spring market like the one we just saw in many real estate markets in Canada in 2023, where prices rose substantially year to date.

For example, markets in Greater Toronto and The Lower Mainland were seeing offer dates with 20-30 offers, much like the spring of 2022.

During the spring market, average prices typically rise 5% to 10% in any given year, simply because most people try to buy in the spring so that they can move in the summer. This demand typically peaks in May, and average prices, and the number of home sales, typically trend downward from May until August. You often see more inventory remain throughout the early summer, making it easier to buy when compared to the spring.

2. Be Willing to Negotiate

It’s important to note that a good deal is made, not found. If something is a really good deal, it’s usually already found – especially for Canadian real estate. When a property is underpriced, in most cases, buyers can expect to see a bidding war, which drives the price up. But when a property is overpriced, it’ll often sit in the market for a while before it sells. As buyers, we often feel compelled to only look at properties below our price range, when sometimes, we might find opportunities elsewhere if we’re willing to negotiate favourable terms.

3. Manage Downside Risk

The biggest risk factor for a household is the cost of interest rates. Paying more on a mortgage can make a difference of tens of thousands of dollars in interest paid, which is just as impactful as negotiating a few extra percentage points on a house price.

Similarly, unforeseen problems with a home can cost just as much. So, work hard for a home inspection, or inspect a property thoroughly during the showing periods if you can’t negotiate a condition. Make sure you’re happy with the whole picture of your real estate decision, not just the price.

What Should Sellers Do?

- Exercise patience: the market has less buying power than it did with record-low rates

- Don’t get stuck to your strategy: this market requires flexibility

- Think about your next move: it’s just as important as the move you’re making

1. Patience is a Virtue

This year’s spring market is slower than last year’s. While price growth has been strong, in line with typical seasonal growth, fewer homes are selling and taking longer to sell. Buyers are being more careful after seeing a steep price drop behind them and a shaky economy ahead of them. While we’re statistically in a seller’s market due to low inventory, the number of homes selling is so low that a slight increase in new listings could shift the market in favour of buyers. In combination, buyers possess more power than they do individually.

It’s not uncommon to see financing conditions in today’s market, especially with banks becoming more careful against rising unemployment and a shaky economy ahead. It may be worthwhile to consider offers conditional on financing to eliminate any subsequent financing issues before closing.

2. Recognize Sunk-Cost Fallacy

Switching costs are one of the reasons the real estate market is so slow. Broadly, switching costs are the costs that a consumer incurs due to changing products. Typically, these are financial limitations, but other considerations are being made to account for psychological, effort-based, and time-based switching costs. In many cases, these costs can be sunk costs. A sunk cost is capital (money, time, or effort) that has already been spent and cannot be recovered.

These sunk costs can include things like preparing a home for sale, moving items into storage, or upgrading a home to make it more marketable. Sunk costs can be tricky with a real estate transaction because we become stuck to the strategy once we’ve spent them. This is called a sunk-cost fallacy, or the belief that because you made an investment, you need to stick with it — even at a potential financial loss. Exercise an open mind and a willingness to adapt – the market is constantly changing, and we must change with it.

3. Prepare for What’s Next

As a seller, what you do after you sell can cost you just as much as your sale. If you’re pushed into a fast closing or forced to take less money, this can drastically change the outcome of your entire transaction. It’s important to think about the entire scope of the transaction – or the “net” outcome. Think about how much you’re making from the sale and how much you’re spending on the next move. There are two moving parts to the transaction – consider them both. Will you be able to accomplish your financial goals with both parts?

What is Coming for Canada’s Housing Market?

When it comes to these potential market changes, there are a few factors to consider, including:

1. Household Net Worth: After three record years of household net worth gains, 2022 was the first time it turned negative since 2011.

2. Job Security: Recessions are often preceded by a cyclical low unemployment rate. Because of this, job security can be an important factor when transacting whether we’re heading toward a recession.

3. Household Savings Rate: Consumers are saving less money, and this could create financial stress or increased supply in the Canadian housing market, as people need to sell assets, like investment properties, to improve their financial positions.

4. Consumer Delinquency: According to RBC’s most recent Economics Report, consumer delinquencies are rising, which means more Canadian households are feeling financial stress. Typically, mortgages are the last type of loan to experience delinquency.

Take Note of Economic Factors in Canada’s Real Estate and Housing Market

There’s much to consider in Canada’s housing market right now. But, by considering all economic factors, buyers and sellers can make a more informed real estate decision in 2023.

Look at seasonality, know your local market trends, find trustworthy real estate professionals, and be patient. All of these tools can help you make the best possible decision for your home buying or selling journey.